$150 Oil or Operation Epic Fizzle

Larry Fink's End Game and the dividend strategy that wins either way.

Editor’s note: Happy Easter Weekend and Happy Passover. May we all prosper in these interesting times!--RC

“Do I believe the war is going to be lasting a long time? No. Do I believe oil is going to be reverting back to where it was? Maybe even lower.”

That a quote by Blackrock CEO Larry Fink during a Fox interview last month. And it’s arguably been the consensus view since.

Sure, Iran will wreak havoc on the global economy near-term by shutting off the estimated 20% of global oil and LNG trade passing through the Strait of Hormuz. But ultimately, the crisis will be resolved. Oil prices will plunge. Prosperity will return. And investors fleeing the stock market now will regret it.

That would be the best outcome for Fink and Blackrock. The world’s largest asset manager needs Americans to passively invest in its giant algorithm-controlled index funds to keep growing its $14 trillion asset base. But neither is Fink a one-armed economist. So, he laid out an “on the other hand” scenario during that interview as well: $150 plus oil and a “stark and steep global recession.”

That’s a less favorable outcome for investors. And as Operation Epic Fury fallout has increased, the doomsday argument has gained adherents, who are betting the situation will escalate.

There’s reason for pessimism. 17% of Qatari LNG production infrastructure has been destroyed and could take up to five years to rebuild. The same attack also eliminated 14% of global helium supply, a lesser known but still vital commodity for semiconductor manufacturing, as well as cryogenic cooling, shielding gas, pressurizing rockets and cooling superconducting magnets.

Subsequent attacks throughout the region show Iran can still hit back hard. That includes destruction of Gulf States and Israeli infrastructure, the downing of an American warplane and a drone hit on a Kuwaiti supertanker. And despite the Trump Administration’s alternating string of assurances and ultimatums, there’s no sign yet Iran will stop striking, let alone allow shipping traffic to resume through the Strait of Hormuz.

Limited Damage to Investors So Far

The longer and further Operation Epic Fury fallout spreads, the higher the stakes become for investors. But so far, there really hasn’t been that much damage to most stocks.

The S&P 500 hit an all-time high of 7,000 plus in late January. After bouncing last week, it’s still only 6-7% below that level. Even the Nasdaq is off just 8-9% from the high it reached around that time. That’s despite a -22% decline in major component Microsoft (NSDQ: MSFT).

Neither has the bond market reacted as though one of Fink’s two extreme scenarios is inevitable. The 10-year Treasury note yield is still elevated at 4.3% plus. But it’s backed off from the 4.5% of a week earlier. And the Federal Reserve is standing pat. That’s despite Chairman Powell’s response to employment data last week that “effectively, there’s zero job creation in the private sector.”

As for dividend paying stocks, the iShares Select Dividend ETF (DVY) is up more than 8% year-to-date, after bouncing back from a late March low point. The Utilities SPDR ETF (XLU) is ahead 9.3%, also following a late month recovery. And even real estate investment trusts are showing signs of life, with the Real Estate SPDR ETF (XLRE) advancing about 4% for the year.

The Dividends Premium Portfolio has given back some of its earlier gains. But we’re still comfortably ahead 13.16% for 2026 so far. That’s one of the best performances for the first three months of the year since the portfolio’s inception back in 2018.

Dodging Fallout to Keep the Good Times Rolling

Bottom line: A lot has happened in the world over the past month plus. And the risk of global entropy getting further out of control is elevated. But it’s been a good year to be an income investor so far, especially if you’ve been willing to own a broad mix of high-quality stocks drawn across sectors.

The question now is what we can do to stay on top at a time when many investors are increasingly ready to bet on extreme scenarios. So here’s what may seem a novel approach:

Don’t try to guess how the macro picture may change in the next few months as the result of Operation Epic Fury fallout. Focus instead on what’s likely to keep making money, no matter how this comes out.

One place to look: Selected renewable energy stocks.

When the Trump Administration was first getting organized, I responded to a highly negative post on wind and solar power prospects by Doomberg, a leading Substack publication that focuses on energy issues. As it turned out, my contention that the incoming government would be relatively benign for the sector was dead wrong. But from an investment perspective, it didn’t matter.

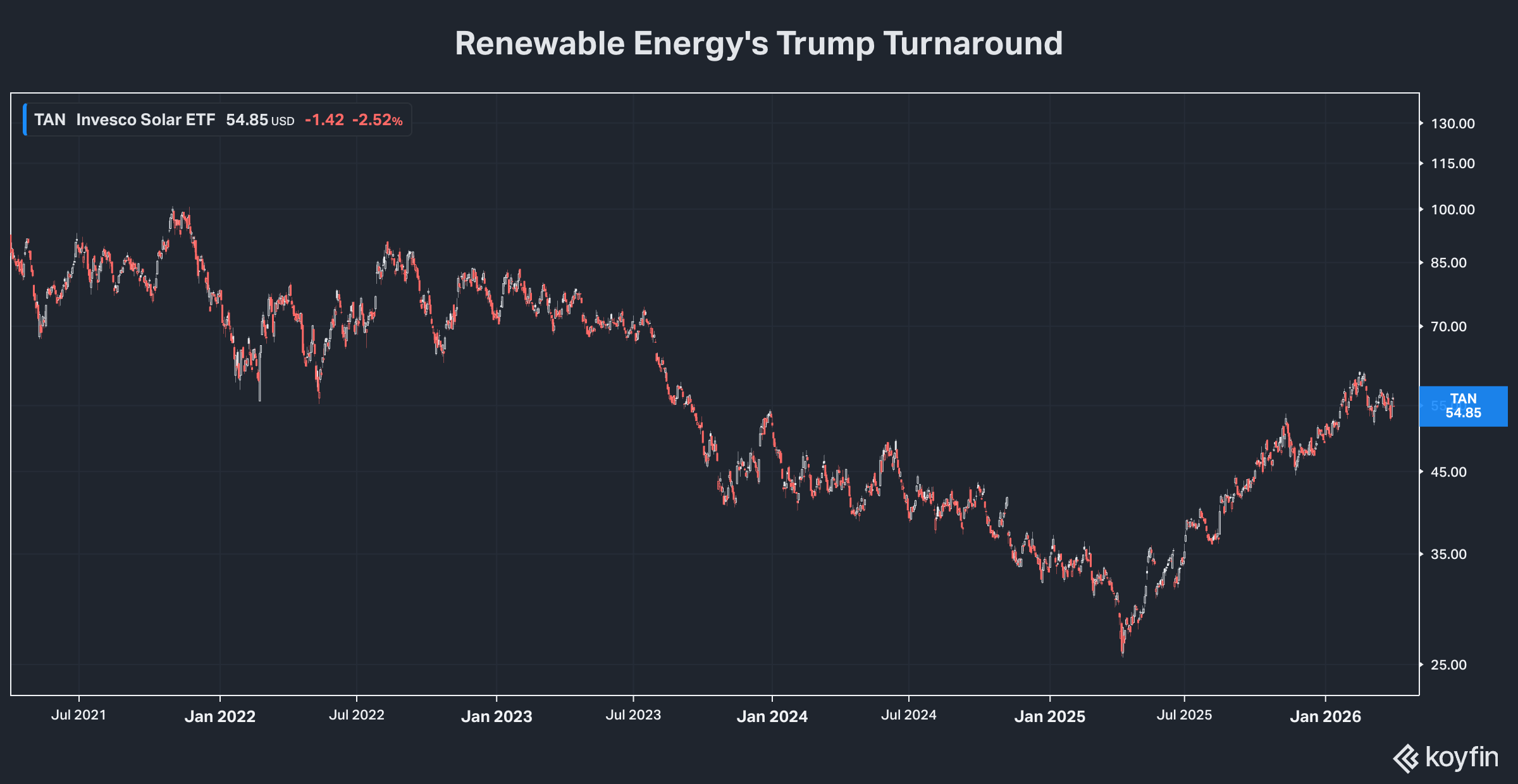

Mainly, since Inauguation Day 2025, renewable energy stocks have been among the stock market’s best performers, reversing a crushing four-year bear market under the previous president.

The Invesco Solar ETF (TAN) dropped roughly -75% from January 2021 through January 2025. But since then, it’s up over 80%, including 11.7% year-to-date. That’s despite a -25% decline this year in First Solar (NSDQ: FSLR), the largest holding and ironically a continuing beneficiary of Trump’s tariffs and trade barriers.

Why the Trump Turnaround for renewable energy? It certainly had nothing whatsoever to do with policy.

From the start, this administration has done whatever it could to impede development and deployment of wind and solar power. Popular tax credits were reversed and phased out, despite the objections of prominent Republicans. Trump’s Interior Secretary has halted new project permitting on federal lands, just as Biden’s did for oil and gas drilling.

Last year, Interior took the unprecedented step of trying to stop six fully permitted and nearly completed offshore wind projects from entering service. The orders were later rejected by the courts. And three of the facilities are now generating electricity for the grid. But the administration’s actions nonetheless drove up project costs.

Dominion Energy (NYSE: D), for example, increased the projected cost of its now operating Coastal Virginia Offshore Wind facility to $11.5 billion from the previous estimate of $10.8 billion—citing a combination of construction delays and eleventh-hour tariffs on key components.

The Trump Administration even agreed to pay Total Energies (Paris: TTE, NYSE: TTE) nearly $1 billion, just to abandon an offshore wind lease it had shown no sign whatsoever of building on!

Tariff policy and local content rules remain key weapons in the Administration’s war on wind and solar. So are IRS rules regarding what wind and solar projects now in development will qualify for tax credits as they’re phased out.

In my view, the Trump Administration has inadvertently but effectively demolished any guardrails for a new government that’s determined to accelerate a phaseout of fossil fuels. And that may not be long in coming, with Democrats increasingly favored to capture both houses of Congress in November.

But just like oil and gas’ surge during the Biden years, renewable energy’s favorable reversal of fortune is fueled by powerful economic factors. And these far outweigh any negative impact from government policy.

According to the US Energy Information Administration, wind and solar together generated a record 17% of America’s electricity in 2025. Output was 34% higher than in 2024. And it’s set to take a huge leap ahead this year as well, with 43 gigawatts of new name plate capacity entering service last year.

Name plate capacity is not the same thing as actual generation. The sun does not shine at night. And wind conditions are notoriously variable even in the most blustery areas, just as hydro flows vary depending on rain and snowfall even in the wetter spaces of the Pacific Northwest.

But solar has now led all energy sources for new capacity additions for 27 consecutive months. That period includes the startup of two new AP 1000 nuclear reactors in Georgia by Southern Company (NYSE: SO). And combined with rapidly expanding battery storage, wind and solar generated 19% of total US electricity in 2025.

That’s a staggering rate of growth, particularly when you consider how large the US power system already is. And it’s also taking place in the context of the fastest growth in US electricity demand since at least the 1960s, as the artificial intelligence race had triggered record building of data centers—especially at the Virginia hub and in Texas.

Wind and solar energy’s detractors—including the Trump Administration—deride them as “intermittent” and therefore fundamentally unreliable sources of electricity. Advocates, meanwhile, assert that disadvantage is being rapidly overcome by paring renewables with battery storage and more effective grid management, utilizing advanced data science and artificial intelligence.

The truth is both “sides” are both right to some extent. Renewable energy is hardly unreliable. But neither is it in any position to fully replace baseload sources of energy like natural gas and nuclear. In fact, states that have moved in that direction like California have eventually had to allow gas plants like Clearway Energy’s (NYSE: CWEN) to re-open to keep the lights on.

But lost in the increasingly shrill rhetoric is the most important point about renewable energy’s US expansion: It’s being “layered on” to systems. And so doing, utilities are both increasing grid reliability and reducing costs, as wind and solar have zero fuel needs and relatively little maintenance expense.

Natural Gas for Coal

Yes, this nation’s rapidly aging fleet of coal power plants is shutting down. And with apologies to coal miners and all due respect to Department of Energy luminaries: Good riddance.

For over a decade, utilities and other power producers have been replacing old coal with new natural gas. And so doing, they’ve eliminated hazardous particulate matter in the air, as well as acid rain gasses that erode monuments and automobiles, mercury in the water and tons of future coal ash that must be hauled off and stored in giant pits. And as Duke Energy (NYSE: DUK) learned in the previous decade with the Dan River leak, those pits are a multi billion-dollar lawsuit waiting to happen.

If you visit a part of the world that still relies heavily on coal-fired power, you’ll notice right away the unwelcome contrast with the relatively clean air in US cities. And that’s thanks to America’s switching out coal for gas.

Replacing old coal with new natural gas also reduces costs. That’s why utilities and power producers are suing the US government for damages resulting from an order to keep coal plants running this year that had been slated for closure—many for gas switching.

Layering on renewables reduces the long-term risk for utilities that swap historically stable priced coal for more volatile natural gas. US natural gas prices have been well behaved since Operation Epic Fury began, with the benchmark price of North American gas slipping under $3 per million BTU last week.

The market for oil is global. West Texas Intermediate crude oil, for example, sold for $111 plus last week. That was more than Brent’s $108 at the time.

Growing LNG exports including from Canada could eventually erase some of the local natural gas discount Americans now enjoy. But if and when we get there, it’s still unlikely we’d see anything close to the price spikes in WTI oil. That’s because there’s a bonanza of shale gas in North America that would be extremely profitable to drill at a $5 per million BTU price.

On the other hand, there’s a good deal less that’s profitable at sub- $3 prices. And while we’re there, gas producers and energy midstream companies are going to tailor investment to long-term deals with LNG exporter and data center supply.

That’s still a very good business. And shale discipline means companies are going to reward shareholders with dividends and stock buybacks even at these prices, The days of producing for its own sake are long gone.

Investment Discipline Comes to Renewables

The same is happening with the renewable energy companies that survived the 2021-24 bear market.