3 Deadly Myths About Utility Stocks

They’re costing you money

Welcome to Dividends with Roger Conrad! I hope everyone is having a great summer, whether you’re vacationing, stay-cationing or just hanging out.

If you haven’t yet, I invite you to check out my Dividends Premium service. This week, I’ll be posting Dividends Premium, featuring the best buys for growth and income in the high yield universe. The following week is Dividends Premium REITs, with my top picks in the real estate sector. The roughly 70 real estate investment trusts I track have underperformed this year. But many of the best in class are primed for big gains the next few years.

I also host Dividends Roundtable on Discord 24-7 to field all your comments and questions. As always, here’s to your wealth!—RC

Not many predicted it, especially with stubborn inflation holding their borrowing costs higher for longer than most expected. And abrupt policy shifts between the Biden and Trump Administration have arguably added other hurdles to performance, especially for leading US solar and wind power producer NextEra Energy (NYSE: NEE).

But utility stock ETFs have nonetheless outperformed the Big Tech-laden S&P 500 by almost a 2-to-1 margin so far in 2025. And performance is even more impressive in the wider sector.

I currently provide buy/hold/sell advice on 167 utilities and essential services companies from around the world in my monthly advisory, Conrad’s Utility Investor. Their ranks include several companies negatively affected by soft oil and gas prices, as well as a handful of small telecoms headed for bankruptcy and utility technology providers battered by the rapid phaseout of rooftop solar tax credits.

Nonetheless, so far in 2025, an astounding 80% of the stocks I track in CUI are beating the S&P 500. More than half have doubled the S&P’s gains or better. A couple dozen have gains well north of 40 percent, including an 80 percent return for a renewable energy producer that fetched a high premium takeover offer.

None of this is headline news in the mainstream media. The reason is simply utility stocks labor under several myths that prevent many investors from taking them seriously when it comes to building real wealth.

You can take that from me. I’ve spent the last 40 years as an advisor and investor trying to convince people otherwise. Those I have are the richer for it. But I can count the number of times I’ve succeeded with big marketing campaigns on one hand.

And they’ve usually been just after the sector had made a big run. In fact, I’ve added the most new readers when my thoughts were inevitably turning to harvesting gains—a cash reserve for buying on the next dip down,

That’s the nature of the stock market. Whether we’re making our own investment decisions or relying on a Wall Street product governed by an algorithm, we all tend to emotionally gravitate to rising stocks and to shun what’s been going down.

Don’t get me wrong. There are usually very good reasons for why a stock is rising or falling. And before we buy low—or sell high—we need to understand them. But the stock market is fundamentally about human behavior. And that means we must always be willing to call out the myths influencing others and to bet against them.

So here are a trio of myths affecting utility stocks that I’ve profitably bet against for four decades. And I expect them to work every bit as well the next 40.

Myth #1: Utilities are bond substitutes.

Fact: Utility stocks are always building infrastructure, now more than ever with US electricity demand rising at the fastest pace since the 1950s. They borrow about half the money needed to build power plants, power lines, pipelines etc. So the cost of money—interest rates—does affect the profit on these projects. And some investors will shift money out of dividend paying stocks when money market rates are attractive, as they are now at over 4%.

But for all that, utility stocks’ best performances over the past 50 years have actually been in years when the economy has boomed and benchmark interest rates like the 10-year Treasury bond yield have been rising! And the worst years have been when rates have dropped, such as 2008.

Utility stock returns follow the fortunes of the companies they represent. In the past few weeks, 42 companies I track in CUI raised their earnings guidance for either 2025, subsequent years or both. Interest rates are still elevated. But the utility business is booming. And that’s driving superior stock performance this year.

Myth #2: Utilities offer investors few (if any) prospects for capital growth.

Fact: Slow and steady always wins the race. A fair percentage of utility stock returns over the past 40 years have come from reinvested dividends. And several of the dividend reinvestment plans I’ve owned the past few decades now actually pay me more in dividends annually than my initial investment! Rather than distribute cash dividends, DRIPs instead buy you more shares of stock.

But utilities today also offer an historic growth opportunity as providers of the “picks and shovels” of the artificial intelligence gold rush—electricity, natural gas, water and broadband infrastructure including AI-enabled date centers. And it doesn’t take many years of even 6 to 7 percent compound annual earnings and dividend growth to really add up—both for your yearly income and portfolio value, as stock prices invariably follow that growth higher.

Myth 3: The Trump Admiistration is putting up insurmountable barriers to utilities’ growth.

Fact: Trump policies overall are already accelerating utilities’ growth.

Too much ink has already been spilled trying to explain why the Trump Administration is so hostile to low cost, easy and fast to build wind and solar energy. But it is a fact they’re doing all they can to throw up roadblocks to what remains a massive development wave. And they’re not finished yet: The US Treasury Department seems likely to tighten the rules to qualify for the wind and solar tax credits that are in OB3, the so-called “One Big Beautiful Bill: A group of Republican senators are now blocking administration appointees to ensure it doesn’t go “too far.”

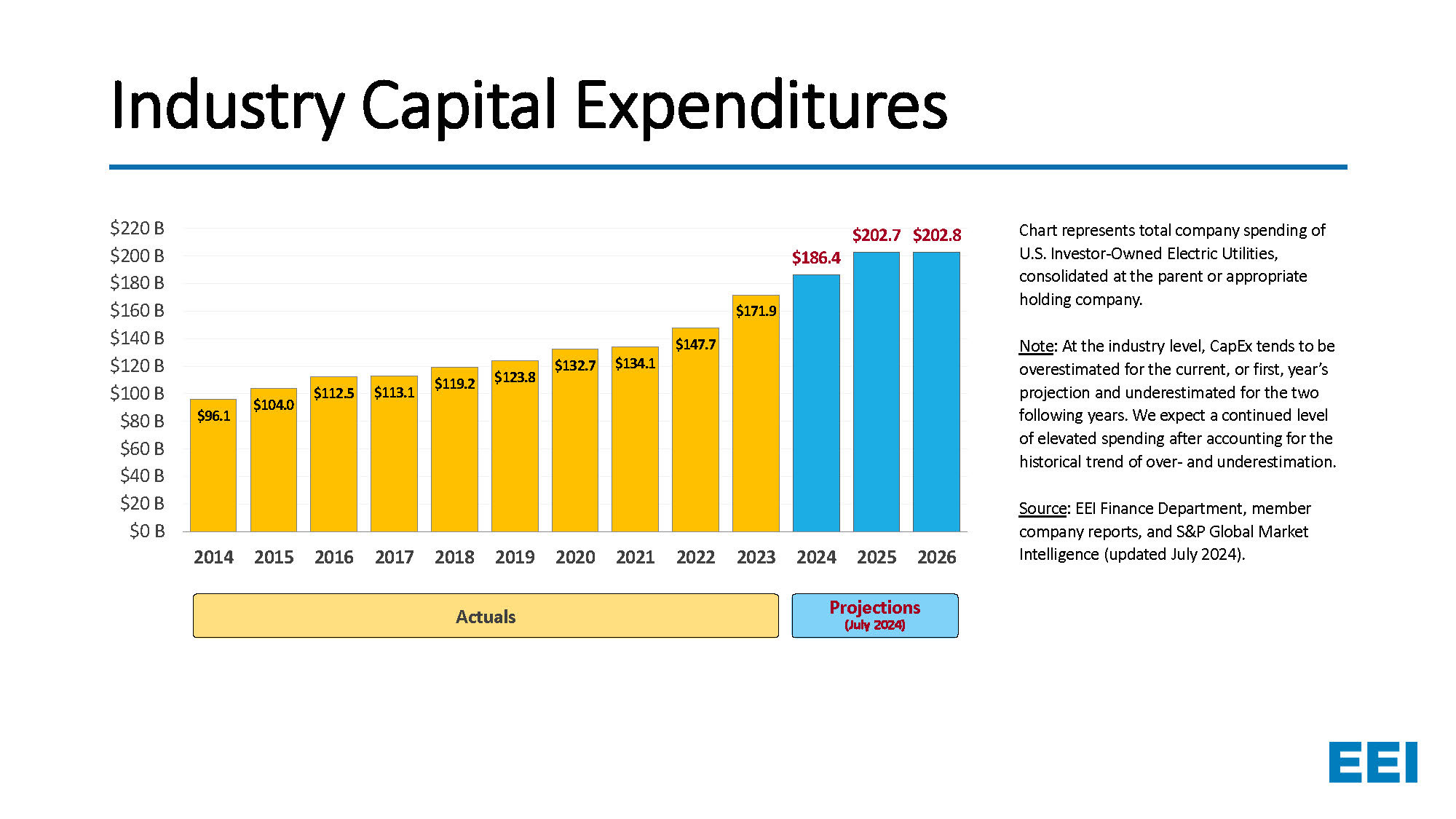

But even renewables-heavy companies are increasing investment needed to drive earnings and dividend growth. And it’s a sure bet Edison Electric Institute projections for 2025-26 CAPEX will fall short of actual spending, just as they have for past decade plus.

How can this be? First, the 900 or so pages of OB3 also include quite a few goodies for utilities. Duke Energy (NYSE: DUK), for example, booked $500 million in tax credits last year just for continuing to operate its nuclear power plants, now extended and enhanced. Utilities are also set up for an investment boom in energy storage, another big OB3 winner.

I highlight these and other benefits for utilities from OB3 in my August issue of CUI. But the biggest will be the hastened demise of remaining competitors for revenue from the accelerating boom in AI demand for energy.

OB3 ends tax advantages for distributed energy/rooftop solar two years ahead of utility scale projects. Industry leaders like NextEra have the resources and ability to dramatically accelerate projects to qualify for tax credits that smaller developers do not.

The leaders can push ahead even without tax credits. And they have the pricing power to push the added costs onto end users. That includes Big Tech—which in a supply constrained world has no choice but to pay up for the power.