3 Great Buys for Second Half 2026

Some leaders and laggards are trading places.

Editor’s note: Thank you for reading Dividends Roundtable! With July 4 celebrations in the rear-view mirror, it’s time to focus on what’s likely to make us money in the second half, of what’s already been a tumultuous year.

Here are three ideas for income-oriented investors. Remember, these stocks will be most effective integrated with the rest of what you own. Next week, I’ll be highlighting current holdings in the Dividends Premium Portfolio.

Have a question? Dividends Roundtable members can ask anything 24-7 on the live chats I host on the Discord and Substack apps. Here’s to building wealth the rest of the year!—RC

First half 2026 was a good time to own dividend stocks.

As of the last close prior to the July 4 weekend, the iShares Dividend ETF (DVY) was ahead by 12.7%, and 14.5% including dividends. The SPDR Utilities ETF (XLU) had advanced 7.2%, 8.6% with dividends.

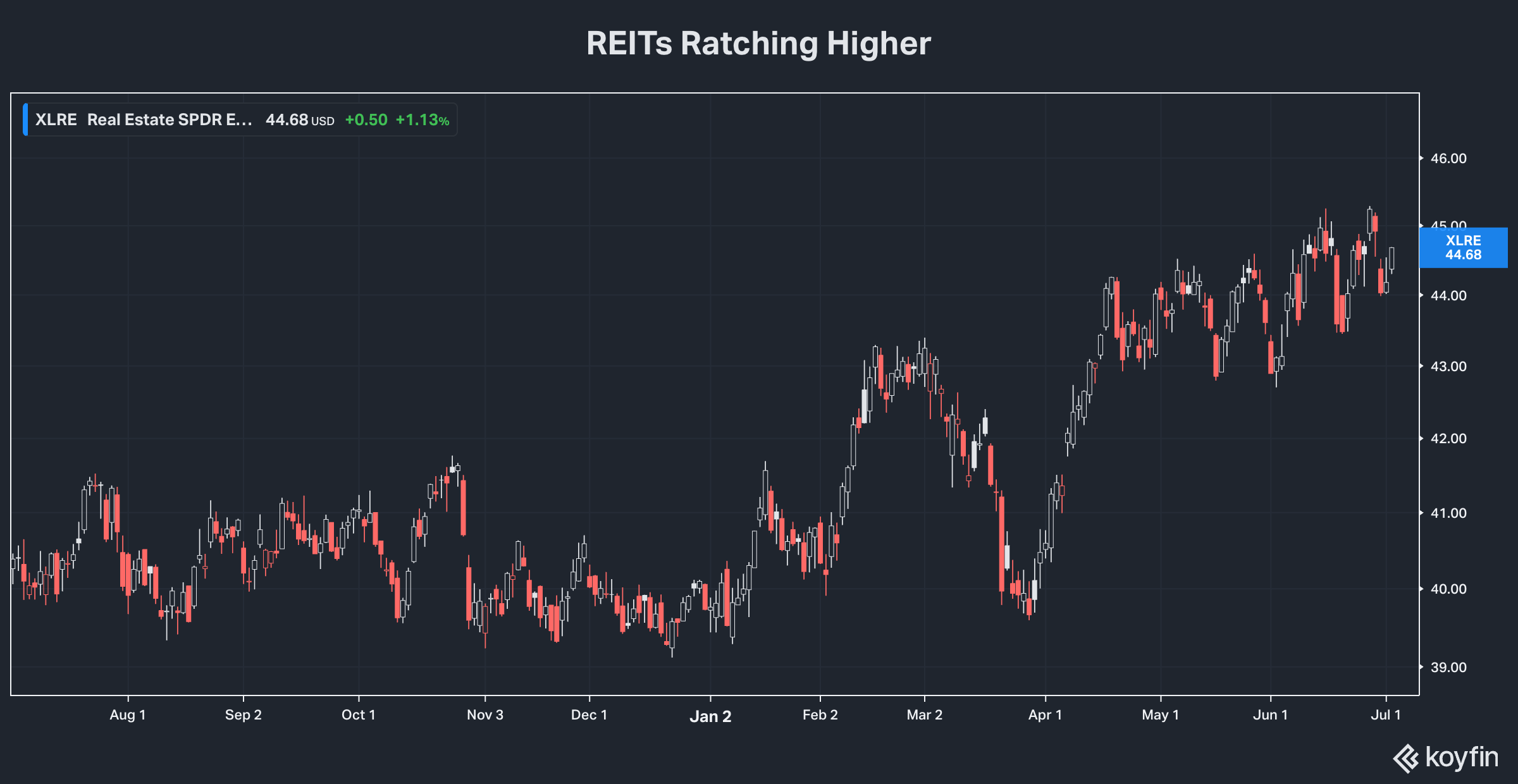

The same numbers for the Alerian MLP ETF (AMLP) were 10.7% and 15.2%, respectively. And even long-lagging real estate investment trusts were firmly in the black, with the SPDR REIT ETF (XLRE) ahead 10.7% and 12.5% with dividends.

Dividends Premium Portfolio stocks have returned an average of 17.35%. Conrad’s Utility Investor companies are ahead 11.2%. And the First Rate REITs finished the first half in the black by 11.8%.

Big Tech and artificial intelligence was once again been the dominant market theme in the first half of 2026. The IPO of Space Exploration Technologies (NSDQ: SPCX) was the largest and arguably most expensive in history. And at this point, it looks set to be followed by a raft of massive AI-related launches, Wall Street as always testing the limits of investor demand.

Yet investors expecting another leg higher for the priciest stocks in history are likely disappointed at this point. The S&P 500’s year-to-date is ahead less than 10%. The Nasdaq 100 has made surprisingly little headway since early May. And though still above the official initial offer price of $135, SpaceX is down by nearly one-third from its peak, reached less than a week after the launch.

The Dividend Stock Solution

It’s three years and counting since the last meaningful decline in the S&P 500. And it’s nearly two decades since the end of the most recent bear market. I define that as a drop of 20% or more lasting more than a few weeks, or long enough to convince a majority of investors to question simply buying the dips.

That’s a long time without a real re-set. Even war in the Middle East, rising inflation and growing US political uncertainty haven’t triggered a real pullback so far in 2026. And they may not be enough to topple the stock market in the second half of the year either.

There are, however, signs that this very long-lived bull market may be running out of steam. That includes what in the past has been unsustainable concentration of wealth in a handful of stocks. Just four technology sectors comprise 42.3% of the SPDR S&P 500 ETF, which is still 33% in just seven stocks—all Big Tech, all heavily leveraged to the single investment theme of artificial intelligence.

Obviously, this has been the state of affairs for some time. It could well be for a good while longer. And similarly, there’s no immutable time limit on Nvidia (NSDQ: NVDA) holding a 7.5% S&P 500 weighting or selling for 104X earnings for the trailing 12-months. Or even SpaceX selling for 810X expected 2027 earnings per share, which would prove wildly optimistic should that company decide to offer satellite-based retail wireless service at scale.

Extreme valuations alone do not bring down stock markets. Neither does extreme FOMO—fear of missing out—as the predominant investor emotion, though it’s reached a new level with the SpaceX IPO.

Equally though these have been warning signs in the past that big changes are afoot. The fireworks are still exploding overhead, just as they were at 1am July 5 in our nation’s capital. But the party is winding down. And it won’t be pretty for those who stick around too long and/or haven’t planned their escape route.

Dividend stocks have been a great solution for investors to stay at the party in first half 2026. They’ve offered a far lower risk alternative to the still headline grabbing Big Tech that dominate S&P 500 ETFs and close cousins, which in turn dominate passively invested accounts comprising a majority of US stock investment.

The best-in-class companies I focus on have also paid us to own them with a steady and rising stream of dividends. And they’ve benefitted from the beginnings of a very discernable rotation out of Big Tech and into other sectors.

Dividend stocks’ outperformance has likely surprised a lot of people because it’s occurred at the same time inflation has been on the rise, causing interest rates to stay higher for longer. The myth persists that companies paying dividends are basically “bond alternatives”—and so like bonds they gain when interest rates drop and lose ground when they rise.

In reality, dividend stocks perform no differently than dividend-less stocks. The key driver of returns is always earnings. When companies are healthy and growing, their share prices rise. When they’re weakening inside, they lose ground.

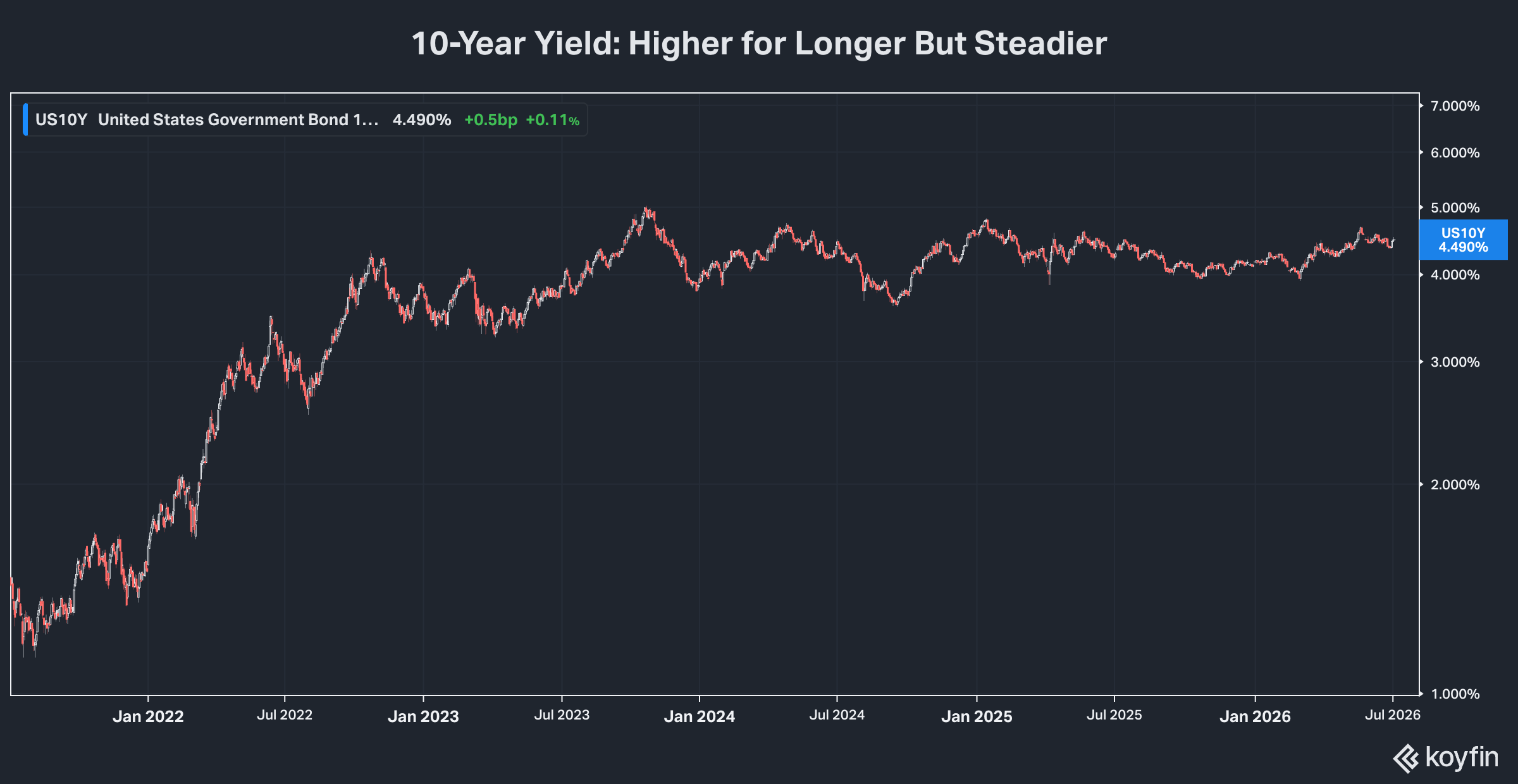

That means dividend stocks like the rest of the market do best when the economy is healthy and growing. And they’re prone to losses when there’s a serious contraction, regardless of what’s happening with interest rates. In 2008, for example, the benchmark 10-year Treasury note yield nosedived by about 50%. But it was the worst year on record for supposedly interest rate-sensitive utility stocks, which had one of their best years in 2009 when rates rose again.

Learning to Live with Higher Rates

Interest rates are important only insofar as they affect earnings. And they’re an important cost for companies to manage, particularly if they rely on investment to grow.

The important thing is that investment returns at least keep pace with the higher for longer borrowing costs. And here analysis of individual companies you own is particularly important.

Some businesses like regulated utilities pass on the added expense automatically in rates and enjoy full tax deductibility. Other companies have pricing power by virtue of occupying a unique niche or providing a service/product that’s currently in shortage.

Not every dividend paying company can pass on higher borrowing costs. And for them, the second half of 2026 could bring higher risk to their payouts.

President Trump finally got his new Federal Reserve Chairman in Kevin Warsh. But with inflation recently reaching a three-year high and global supply chains still disrupted by trade barriers and war, the US central bank has stripped language from its policy statement indicating a “bias” toward cutting rates. And that suggests the Fed is likely to keep the rates it controls higher for longer.

But the Fed’s apparent tightening has apparently calmed the bond market. The 10-year Treasury yield, for example, has been mostly trending lower recently. And there are increasing signs that corporate America is learning to live with higher for longer borrowing costs, with a number of companies in my various coverage universes issuing new bonds at reasonable interest rates.

I define that as a funding cost low enough to ensure a strong return on investment.

HA Sustainable (NYSE: HASI), for example, is a business development company (BDC) focused on providing debt and equity investment to low and no-carbon energy ventures. Management last month issued $1 billion of low investment grade “green” notes maturing in 2033 at a rate of 5.95 percent. That will help fund investments with an average return of 10 to 11 percent.

Bottom line: HA has a healthy profit margin at its current funding cost. And that makes it the kind of dividend paying stock we want to own going into second half 2026.

Q2 earnings and guidance updates will provide us our next great opportunity to assess health and growth of the companies we own. And how management is dealing with interest rates that are still well above their levels earlier in the decade will be especially critical.

For some very high yielders like Canadian telecom Telus Inc (TSX: T, NYSE: TU), it’s going to be very important for us to see meaningful progress on debt reduction. This is what management has been guiding to over the past year. It was the reason given for not raising the dividend this year. And I would view any retreat from projections as a major negative, even with shares pricing in a dividend cut already.

It’s a lot of work for us to put companies through the wringer like this. But that’s how we’ll save a great deal of pain down the road.

On Strategy: Stick with Stocks (Carefully)

You won’t build real wealth investing without owning stocks. And with ETFs overloaded on the same flagging leaders, you’re not going to do well in this market without focusing on individual stocks, rather than sectors or averages.

But making our own decisions means controlling risk. And that means ensuring what we own can back up its dividend with a strong business that will be resilient no matter what lies ahead.

I follow a four-point investment plan to control near-term risk with Conrad’s Utility Investor portfolio positions:

· Sell stocks of any companies that are weakening as businesses, even if it means taking a loss.

· Take at least partial profits on favorites that have run to unsustainable valuations. Deploy proceeds into a reliable cash reserve, such as Vanguard Federal Money Market Fund (VMFXX), which currently yields 3.59 percent.

· Keep your portfolio diversified and balanced. Never double down in falling stocks. Always spread your bets.

· Make fresh money investments incrementally. Decide how much you want to invest. Then cut the purchase into three parts at roughly six-week intervals.

Careful analysis of Q2 results and guidance is the key to avoiding weakness at a time when overall conditions are increasingly uncertain. And we’ll get a pretty good idea of where we stand heading into second half 2026 over the next 4 to 6 weeks.

At this time—based on what we saw in Q1 and developments since—I don’t anticipate any of my recommended Dividends Premium, First Rate REITs and Conrad’s Utility Investor portfolio stocks weakening. But I always let the facts change my mind. And if that happens, we’ll cut the strings to the offending company and move onto something else.

Here are three opportunities I see for income investors in advance of Q2 results:

· Selected water utility stocks—Just a couple years ago, the best in class of this sector were priced at extremes and thoroughly unattractive yielding 2% or less. And I advised taking profits. Then they went through a period where no one wanted to own them, despite strong execution and a healthy boost in M&A. And now they’re again bouncing back to reflect that value. You won’t find a sector that’s more resilient in recessions and bear markets.

· Selected North American energy midstream companies--Operation Epic Fury forever shattered the long-standing illusion that oil and natural gas shipping in the Persian Gulf was without risk. Now global producers and major importers are scrambling to secure alternative sources, with North America the biggest beneficiary. Midstream companies enjoy a massive opportunity to bring energy to market for export as well as to generate electricity for data centers.

· The US Big Three Telecommunications stocks—America’s communications leaders have been locking down market share with expanding fiber broadband and 5G wireless networks at an accelerating rate. All three posted strong Q1 results and will report a big Q2 in the next few weeks. And they’re suddenly cheap, following a selloff triggered by the SpaceX rumor mill.

If you buy any of the stocks I feature in this report, remember to diversify and balance. The Dividends Premium portfolio offers a weighted model, featuring high quality stocks across industries with pricing power and strong balance sheets. Look for holding-by-holding analysis in the next Dividends Roundtable post, along recommended moves for the start of the second half.