3 High Yield Mergers to Bet On Now

A good deal will build real wealth no matter what the S&P 500 does.

Editor’s note: Thank you for reading Dividends Roundtable! Want to join the discussion with other informed income investors? Check out the live chats I host 24-7 on the Substack and Discord applications. Here’s to a great summer and to your wealth!—RC

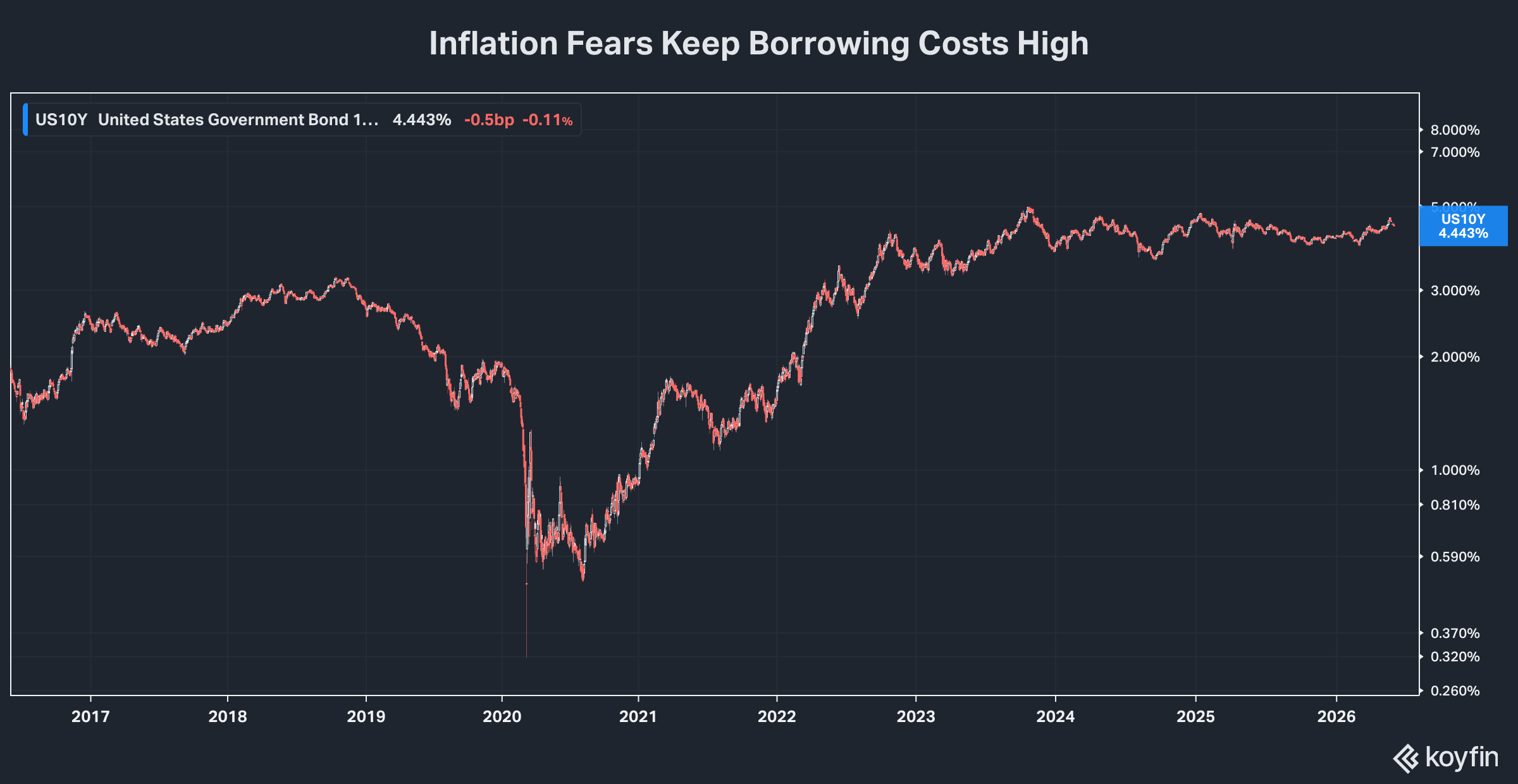

What will the much-hyped SpaceX IPO fetch? Will a real truce at last open the Strait of Hormuz? Will oil prices crash in response? Will the surge to 3.8% last month on the Federal Reserve’s key inflation metric force incoming Chairman Kevin Warsh to raise interest rates, rather than cut as President Trump demands?

Will current political polls hold up and a Blue Tsunami reshape power in Washington following November mid-term elections? Have recent global supply chain shocks ensured an economic slowdown? And how high can the stock market climb, led by a handful of historically expensive names all tied to the same investment theme—artificial intelligence?

Those questions are dominating the headlines. And algorithms that control a growing share of Americans’ stock portfolios are trained to respond to them. So they’ll greatly affect where the S&P 500 closes out 2026.

But they’re all really just bets on momentum. And that means none are really investable.

Building real wealth and durable income means taking positions from good entry points in high quality companies that will grow over time. I recommend following my four-part Dividends Roundtable strategy:

· Build positions in dividend paying companies that stack up well on payout sustainability, revenue reliability, regulatory/legal risk, balance sheet strength and operating efficiency. Sell any company you own when it falters on these criteria.

· Always diversify and balance. Own stocks in multiple sectors, rather than load up on just one or two. The greater a stock’s weighting, the more damage even a mild pullback will do to portfolio value. And even the strongest company can stumble unexpectedly. I also never average down a falling stock just to reduce cost basis.

· Take partial profits when share prices reach momentum-led extremes. Sock away the proceeds into a cash reserve, which can be reinvested in lower priced quality stocks or harvested for a rainy day.

· Invest incrementally to put the power of dollar cost averaging to work. For example, plan to take one-third of your position now, one third in six weeks and another third six weeks later.

The so-called “Magnificent 7” Big Tech stocks have gotten a second wind this spring. And they’re again commanding the headlines, with the S&P 500 ETFs they dominate now up 11.2% year to date. But the Dividends Roundtable strategy also continues to work, with the 19 positions up an average of 18.3% so far in 2026.

To be sure, not all of my stocks are ahead this year. Residential real estate investment trusts, for example, continue to lag in an environment of higher for longer borrowing costs and previous years’ overbuilding in many markets.

Energy stocks have been on a roller coaster ride all year. And investors continue to go back and forth on what my friend and colleague Elliott Gue has written in our Substack advisory the Energy Bulletin as “escalation” and “deescalation” assumptions for oil and natural gas prices. Other companies across a spectrum of industries continue to be negatively affected by global supply chain disruption that shows little sign of settling.

But the point is if you spread your bets on high quality stocks across multiple sectors, your winners will more than offset losers, in all but the worst market meltdowns. That will also minimize overall portfolio volatility, even as both the winners and losers in the current environment become more valuable as businesses.

A Current Trend Long-Term Investors CAN Bet On

There is one investment theme now grabbing headlines that’s also worthy of long-term bets from wealth building income seekers like ourselves. That’s M&A, short for “mergers and acquisitions.”

M&A activity has picked up steam over the past year for several reasons:

· Cost of capital. A couple of years ago, it looked like long-term borrowing costs were on the way down, with the Federal Reserve easing up on its rapid tightening of 2022-23. Now with inflation running at 3.8% on the central bank’s preferred gauge, Fed cuts to short-term rates could actually fuel inflation fears, pushing cost of capital higher still. Merging is a proven way to strengthen balance sheets and so doing gain access to lower cost debt and even equity capital.

· Scale advantages. Inflation is rising. And joining forces provides opportunities for companies to meaningfully cut costs by eliminating duplicative operations. Getting larger also increases leverage in procurement negotiations to offset higher prices. And pooling resources means better access to technology, as well as opportunities to tap top talent, further boosting efficiency so companies can do more with less.

· Trump Administration regulators have made it clear they look favorably on M&A in general. Officials have occasionally used the approval process to push unrelated policy objectives, such as eliminating DEI (diversity, equity and inclusion) programs. But most deals have been able to close with few if any real conditions.; And companies across multiple industries are now stepping up to take their shot.

Certainly, not every merger has been a home run historically. Remember AOL and Time Warner in the previous century? That deal was supposed to unite the future of the Internet with the premier media company of the present. And no one was more excited at the time than the late, great Ted Turner, the billionaire who had built a massive media empire including turning MLB’s Atlanta Braves from laughingstock to powerhouse.

Nonetheless 30 years or so later, AOL/Time Warner is considered a classic case of M&A failure taught in business school. And AT&T Inc’s (NYSE: T) deeply discounted acquisition of the combined company some years later ended with a massive writeoff and dividend cut.

The list of reasons deals fail is just as long as the number of companies failing. Those range from too much debt leverage to unforeseen circumstances and management fundamentally misunderstanding their nature of what they were joining together.

There are, however, three industries where M&A has almost always succeeded in creating stronger and more vibrant companies.

One is regulated utilities. Samuel Insull—popularly known as the “Monopoly Man”—was the first to apply Henry Ford’s principles of mass production to the electricity business. Before that, power was a luxury item only the wealthy could afford.

Insull’s focus was building scale to drive down costs and prices. And the key element of his strategy was M&A. His Chicago-based Commonwealth Edison empire consolidated hundreds of small systems to create one large one capable of mass-producing electricity. And since his time, there have been literally thousands of mergers between operating, regulated utilities—not one failing to create a more powerful power provider.

Early in my career as an analyst, I called the proposed merger of two Ohio utilities—the former Centerior Energy and Ohio Edison—a “mindless merger.” And I can admit I’ve since eaten my words. They’re at the core of FirstEnergy Corp (NYSE: FE), a very successful recommendation in my Conrad’s Utility Investor.

Utility mergers have always been successful because they basically join identical businesses. Sometimes there are management egos to contend with. Occasionally too much leverage is used. But at the core, the partners have the same assets, the same employee skillsets and the same regulatory and customer challenges. And by joining forces, they have more resources to deal with the challenges.

Scale in the oil and gas business has similar advantages up and down the value chain. The nuances of drilling, gathering, processing, compression and so on vary by location and the nature of the reserve. But wherever companies operate, they need a roughly similar mix of assets. And large, diversified players can more effectively deploy resources.

Two of the most effective mergers in history were between major oil companies: Chevron and Texaco and Exxon and Mobil. And arguably, BP’s earlier consolidation of the former Amoco and ARCO is the main reason it was able to survive the devastating Macondo oil spill in the Gulf of Mexico.

As with utilities, M&A had picked up for energy companies up and down the value chain the past few years. And the reasons for this urge to merge are roughly similar: To boost efficiency, diversify geographically and by customer and enhance access to capital at a time of higher for longer interest rates.

And that combination of incentives is now starting to drive consolidation in a third sector that’s consistently produced high, safe and growing dividends: Real estate investment trusts.

No one should ever assume REIT dividends are quite as secure a regulated utility’s payout. That much was proven again in 2020, when the pandemic forced dividend cuts at all but a handful of REITs including strongly investment grade indoor mall operator Simon Properties (NYSE: SPG). But the sector’s strongest do have a solid track record sharing profits with investors as lofty dividends.

Like utilities and midstream energy companies, REITs depend on access to low-cost capital to grow. And that’s become a challenge for many the past several years, particularly as lower rate mortgages and bonds have needed to be refinanced.

As I pointed out last week in Dividends Roundtable REITs coverage, multiple property sectors are also dealing with at least temporary oversupply issues in key markets that have depressed occupancy and especially rents on new leases. That’s now extended to the residential REIT sector, which historically has been resilient in even the weakest of economic environments including the pandemic year.

As a result, REITs are turning to boosting scale to keep margins steady by boosting purchasing power and access to capital. And though every property has its unique characteristics, there are also broad similarities in real estate that create opportunities for improved efficiencies.

I expect to see more M&A in these three sectors over the next year. One way to bet is to buy companies that are most likely to attract a high premium takeover offer in the next 12 months. That’s basically speculative. But you can reduce your risk considerably by sticking to companies you’d want to own even if no offer was ever made.

The higher percentage way is to bet on deals already announced, by owning the stock of the target or the acquirer. You obviously won’t realize the initial gains that typically follow the announcement of a generous offer. But in the utility sector especially, regulatory approvals can take time. And stocks of acquired companies can trade at sizeable discounts to offer prices right up to the close, which investors will then pocket as well as any dividends paid during the process.

The real wealth building appeal of a strong merger is long-term. Investors tend to take a “show me” approach. So rarely if ever will the full potential of a deal get priced in right away. Rather, it unfolds over time as strong annual capital appreciation and dividend growth—the surest way to build real wealth and powerful income streams.

Below I highlight an opportunity in each of these three industries that will lock in that kind of growth long-term for investors, whether the stock market booms or busts the rest of this year. And these stocks trade at great entry points.