7% Yields Wall Street Ignores

My top inflation hedges for the coming shock.

Editor’s Note: Thank you for reading Dividends Roundtable!

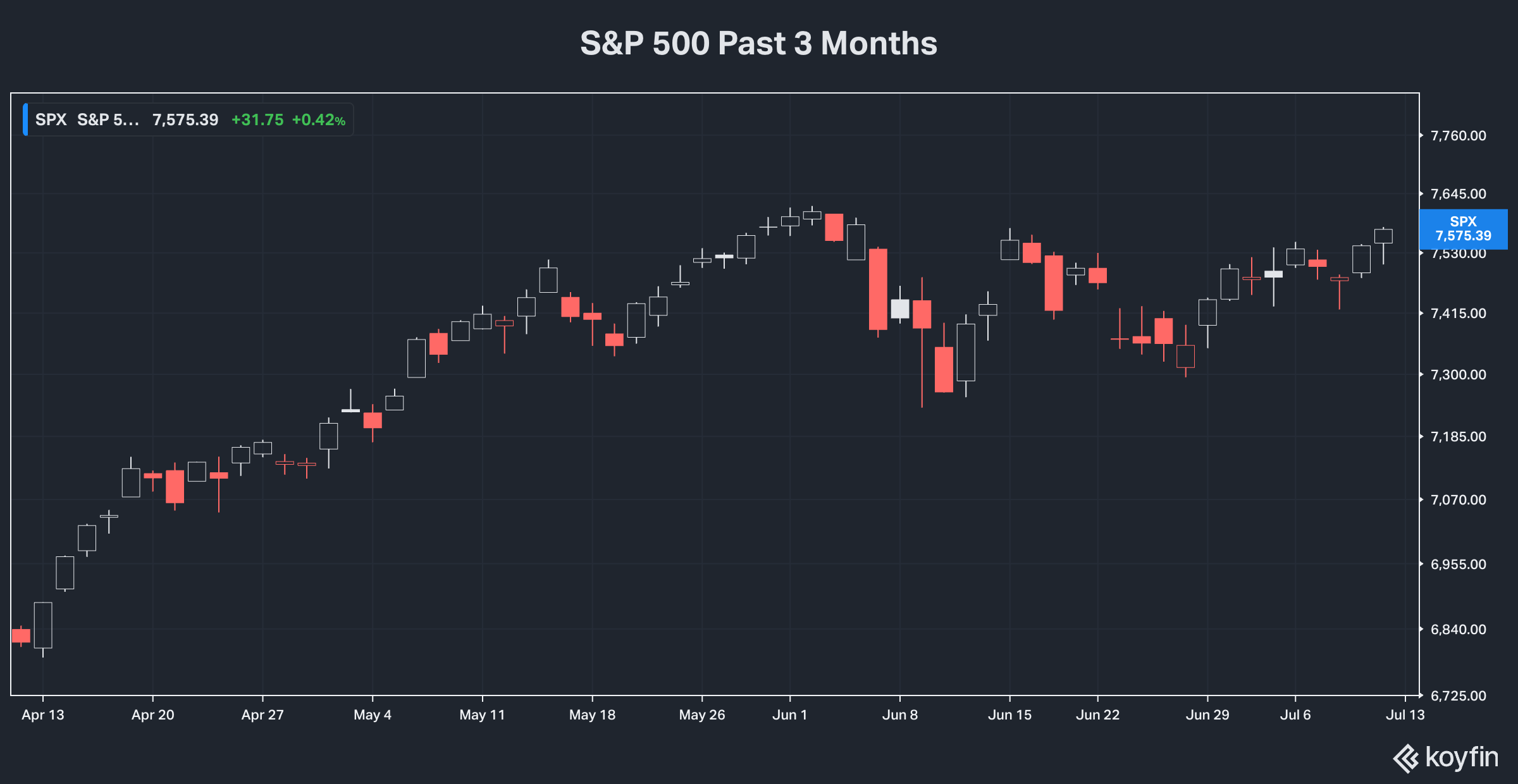

Call it lack of conviction. For the past two months and counting, leading and lagging stock sectors have been changing places regularly, sometimes intraday. And the S&P 500 has made no real headway.

That’s what happens when inflation is on the move. But it’s an ideal opportunity to buy top quality dividend stocks that are still historically under owned, even though they’ve outperformed for the past year and a half.

Over the next 4 to 6 weeks, corporate America will release calendar Q2 results and update guidance. And this report highlights what to expect from every stock in the Dividends Premium Portfolio.

That includes my two best fresh money buys, featuring yields as high as 7%. Both companies are set to get a big boost from their Q2 results, which should be significantly better than what discounted share prices currently suggest.

Have a question? Challenge me by joining the investor forums I host 24-7 on the Substack and Discord apps. Here’s to your wealth!--RC

As of Friday’s close, the iShares Select Dividend ETF (DVY)—a performance benchmark for dividend stock portfolios—has a year-to-date total return of 14.75%. The average for our Dividends Premium Portfolio stocks is 17.22%.

Can we possibly expect a similarly strong performance in second half 2026?

I think so. For one thing, our companies are all healthy and growing. They all have pricing power and balance sheet strength to thrive in an inflationary environment, even if means higher for longer interest rates.

These companies don’t command the smoke and thunder of Big Tech IPOs. But contrary to popular wisdom, best in class dividend stocks have also been market leaders the past couple years.

Our stocks should get another boost over the next 4 to 6 weeks from reporting solid Q2 results, including more than a few guidance increases. And in the meantime, they’re paying us high, reliable and growing dividends to own them.

But even high-quality dividend stocks’ returns are going to depend in part on what happens to the broad stock market. And here the picture is a bit cloudier.

Mainly, if the big market averages that dominate passive investors’ portfolios can avoid a meaningful correction, the best-in-class dividend stocks should head higher in second half 2026, and in a leadership position. But if they can’t, most stocks are likely to head lower, whether they pay dividends or not.

In my view, inflation poses the greatest risk to stocks now—with the exception of sectors that directly benefit like energy and mining. That’s not because the rate of increase has reached some tipping point, though a three-year high is worth notice.

Rather, there’s an apparent consensus that what we’re seeing now is transitory. You can definitely see it in gold prices, which have steadily crept down towards $4,000 since March, when they were pushing $5,500. You see it in mining stocks that surge, only to sell off again. And you see it in bond yields that are little changed from the beginning of the year, despite some jagged volatility along the way.

So far, nothing has been able to puncture that confidence that inflation is under control. That now includes pretty convincing evidence that nothing has been settled in the Persian Gulf, and that the Strait of Hormuz is still a hostile place.

In addition, last week the Bank of Japan announced producer price inflation reached 7.1% in June, up from a revised 6.6% year-over-year rate in May. The BOJ has already raised its policy interest rate to the highest level since 1995. And speculation is growing the rate may double in coming months.

Like the rest of Asia ex-China, Japan relies heavily on imported energy, particularly with its nuclear power plants largely shuttered. And much of Japanese inflation is from rising materials prices. But US producer prices rose almost as much in May (6.5%). And odds are June numbers announced July 15 will be in that neighborhood.

One reason investors appear to ignoring the evidence is that global oil prices have not spiked toward $100 a barrel again. In fact, there’s renewed talk of an impending glut that will send prices plunging toward $50 if not lower.

My long-time friend and colleague Elliott Gue points out that China’s effective management of its massive strategic reserve is one reason for oil remaining relatively well behaved despite the violence now affecting both Persian Gulf and Russian supplies. And readers of our Energy and Income Advisor will see more about that later this month.

China’s ability to effectively manage imported energy risk bodes well for its stocks. And that’s a big reason we’re staying with our Hong Kong position in the Dividends Premium portfolio.

But the other side of this is we can forget about a meaningful supply response to $70 to $80 oil prices, other than from producers and importers trying to wean off Middle East output. And that’s very bullish for our energy stocks long-term.

Bottom line: There’s meaningful risk the consensus is underestimating potential inflation. And that makes the stock market at risk to anything that punctures confidence, if for no other reason than a growing belief interest rates will stay higher for longer.

Still Strung Out on Big Tech

This is also a time when Wall Street is severely testing investors’ appetite for artificial intelligence-related companies.

Last month’s IPO of Space Exploration (NSDQ: SPCX) met 80% plus owner/CEO Elon Musk’s target of $75 billion. But despite being force-fed to passive investors’ portfolios, the stock’s performance has been up and down since. And as of Friday’s close, the price is about one-third lower than the peak less than a month ago.

With that example, will investors absorb the supply of AI stocks lined up for IPOs this year? Probably.

But a less than successful launch or two would not just negatively impact the specific issuers. It would also undermine the case for the seven Big Tech companies that still hold a roughly one-third weighing in the S&P 500—and are more expensive than ever relative to their sales, earnings and underlying business value.

I’m not strung out on bloated Big Tech. And as I note in my company-by-company review later in this report, each of the Dividends Premium stocks appear set to report strong calendar Q2 earnings and updated guidance in the next few weeks.

Consistent, powerful growth combined with strong balance sheets is what will ultimately propel our stocks to superior long-term returns—building our capital while they pay us richly in dividends. And it’s what will limit our downside risk if the stock market’s leaders eventually roll over, while ensuring our holdings are among the first to recover.

Bull markets always end with a whimper, not a bang. In fact, big declines in a short period of time have historically been great times to buy, the Pandemic selloff of February/March 2020 the last great example.

So long as I’m confident in the underlying strengths of our Dividends Premium holdings, I’ll be using meaningful stock market selloffs as a time to add to positions. That’s one reason this portfolio always maintains a solid cash reserve.

The S&P 500 has made little headway since mid-May. And neither has the Nasdaq 100. That may or may not mean the robust move of the past several years is fading to a whimper. But it’s more important than ever to stick to our four basic strategy rules:

· Build and hold onto positions in companies with underlying businesses set for long-term growth that have healthy balance sheets. I sell when the business numbers tell me a company no longer offers that, even if it means taking a big loss.

· Maintain a cash reserve against the possibility of a broad correction. My favorite parking place for cash is still the Vanguard Federal Money Market (VMFXX), which currently has a 7-day SEC yield of 3.58%. It’s not the only suitable money market investment. But anything you choose should be sponsored by an organization that can protect $1 net asset value. And you should be able to access funds in a timely manner.

· Never overload on any one stock. That’s no matter how attractive a particular company looks. Spreading your bets is the surest way to limit risk you’ll be taken down by an unexpected setback with a single company. Diversification rather than doubling down also takes the emotion out of decision making.

· Make fresh investments in increments of two to three, rather than all in one purchase. And I will pare back positions when a stock rises far enough to be out of balance with the rest of the portfolio.

Since inception, the portfolio has a solid total return of 103.27% following this strategy. Certainly not every pick has been a winner. And sometimes I’ve held on too long to a position I later sold. But over the past 8 years we’ve been able to control risk and steadily build wealth while harvesting a rising stream of dividends.

That’s exactly what I expect the rest of 2026 and going forward. Q2 results and guidance updates have the potential to deliver solid boosts for all of the positions. M&A will lift other stocks, possibly including high premium offers for companies not currently involved in deals. And others should get a boost from firming commodity prices, as any supply response to higher levels this year fizzles out.

Action Plan

So what’s our action plan for this month? I generally like to make my strongest recommendations shortly after companies announce their results and update guidance.

Occasionally, the news will be so surprisingly good that a stock’s price will get away from me. But that happens a lot less often with substantial companies, such as those I recommend here. And waiting gives me an opportunity to verify my stocks are still performing where it counts—that is their underlying businesses are moving in the right direction.

I am comfortable enough with two names ahead of results to put them front and center as this month’s top fresh money buys. They are: