The S&P 500 is Un-Investable

Why gold stocks > Big Tech stocks.

Editor’s Note: Thank you for subscribing to Dividends Roundtable!

Will Operation Epic Fury fallout bring doom or boom for stocks? Or will it ultimately be revealed as just a headline grabber that distracted investors from where they should have been paying attention?

I’m inclined to believe the latter. It’s patently absurd to buy or sell an S&P 500 ETF—with an historically high 35% weighting in just 7 super-expensive Big Tech stocks—based on whether the Strait of Hormuz is really open for business. But that’s exactly what trillions of dollars in algorithmic trades have done over the past month, with the ironic result of little real change in actual stock prices.

Don’t get me wrong. Odds are OEF fallout will be with us for months and potentially years—with favorable and unfavorable impacts for investors. But rather than make big market bets, it’s far better to target specific investments that will fare well regardless of how OEF comes out.

That’s what this month’s two top fresh money buys are all about. We’ll build wealth from their powerful value propositions regardless of how ongoing events in the Middle East are or aren’t resolved.

Have a question? Then join my Dividends Roundtable forum, which I host 24-7 on the Substack application. Join an existing thread or start a new one!

Here’s to your wealth!--RC

Algorithmic trading churning trillions of dollars in and out of stocks, based on headlines that are changing intra-day. That about sums up the recent action in the S&P 500 index, related ETFs and close cousins.

Last week closed out on a rally ignited by a statement from Iran’s Foreign Minister that the Strait of Hormuz is open for business again. And there was knee-jerk selling of oil and energy stocks.

The Saturday news, however, was the Strait is closed again—if it was ever truly open. And that means the headline-following algorithms have already lined up the opposite trade for Monday morning, though they could well reverse again depending on the “news.”

The S&P 500 is supposed to represent a broad swath of the US economy. And ETFs based on it dominate Americans’ portfolios, especially those who’ve abdicated their decision making to some form of “passive” investing.

But the sad fact is the US stock market’s premier index is no longer investable, at least for anyone who’s not an inveterate day trader.

S&P 500 performance now is basically tied to just seven Big Tech stocks, all connected to artificial intelligence. Listed in order by percentage of the index:

NVIDA Corp (NSDQ: NVDA)—7.99% of index ETF, 8.15% 2026 return.

Apple Inc (NSDQ: AAPL)—6.41% index, -0.51% return.

Alphabet (NSDQ: GOOG/GOOGL)—5.82% index, 8.74% return.

Microsoft (NSDQ: MSFT)—5.17% index, -12.38% return.

Amazon (NSDQ: AMZN)—4.04% index, 8.55% return.

Broadcom (NSDQ: AVGO)—3.13% index, 17.71% return.

Meta Platforms (NSDQ: META)—2.45% index, 4.40% return.

These have been the market leaders since 2022. And they’re as a direct result historically expensive. So, it’s no wonder the S&P 500 is also historically pricey at 30X times earnings with a yield of less than 1%.

These seven companies are the leaders of an industry still in its nascent stages of changing the world. But that has little or nothing to do with what’s moving around their stock prices now. In fact, they’re unmoored from any recognizable metric of underlying business value.

Rather, its algorithmic trading triggered by news flow from Operation Epic Fury fallout.

There’s some logic to this trade. Mainly, the faster the conflict in the Middle East winds up, the less chance ongoing disruption to supply chains—especially commodities and energy—will plunge the global economy into a real recession. And that in turn reduces risk to investment markets.

But as wealth building investments, these stocks have run out of steam. After this week’s rally, the S&P 500 SPDR ETF (SPY) is in the black 4.4% year-to-date. But what the headlines gave last week, they could easily take away this week.

It could be years before the stock market’s new leaders achieve enough balance to make S&P 500 index related ETFs a viable wealth building bet again.

By contrast, investors who pick their own stocks can build positions in the new leaders now, free of the baggage of bloated Big Tech. And that’s what we’ve been doing in this income and growth focused portfolio.

Objectives and Strategy

Our three core objectives never change, no matter what the market season.

That’s number one to build a reliable and rising stream of income. I rarely if ever will chase the highest current yields available, unless there’s an extremely compelling argument to do so. Instead, I draw from companies paying competitive dividends that the underlying business can support and grow year after year, regardless of the economic environment.

Second, I want to grow principal over time by building positions in high quality companies that are set to become more valuable as businesses over time. And third, I want to minimize overall portfolio volatility, so no one following this strategy ever has to “eat their seed corn”—sell good stocks at bad prices because they need to harvest cash.

To accomplish these goals, I follow four basic strategy rules:

· I build and hold onto positions in companies with underlying businesses that are positioned for long-term growth and have healthy balance sheets. I sell when the business numbers tell me a company no longer offers that, even if it means taking a big loss.

· I maintain a cash reserve against the possibility of a broad correction. My favorite parking place for cash is still the Vanguard Federal Money Market (VMFXX), which currently has a 7-day SEC yield of 3.56%. It’s not the only suitable money market investment. But anything you choose should be sponsored by an organization that can protect $1 net asset value. And you should be able to access funds in a timely manner.

· I never overload on any one stock. That’s no matter how attractive a particular company looks or even if it trades below its “Dream Buy” price (see attached table), which are entry points that in the past have ensured windfall gains. Spreading your bets is the surest way to limit risk you’ll be taken down by an unexpected setback with a single company. I can guarantee if you invest for long enough, this will happen to at least one of your stocks. Diversification rather than doubling down also takes the emotion out of decision making.

· I always make fresh investments in increments of two to three, rather than all in one purchase. And I will pare back positions when a stock rises far and fast enough to be out of balance with the rest of the portfolio.

It’s not a perfect strategy. There isn’t one in investing. And in my view, there never will be. Stock market action is essentially the result of hundreds of millions of decisions by human beings with different objectives and preferences.

Every successful system works until it doesn’t. And the same rule applies to the increasingly sophisticated algorithms developed over the past few decades, including when they’re run with artificial intelligence that’s capable of making and executing decisions on its own.

But my strategy is getting the job done so far this year. Portfolio holdings are up 13.55% on average year to date. And since inception, we’re ahead by 97.47%, assuming harvesting cash dividends rather than reinvesting. Our weighted yield is 4.5%.

One reason we’ve outperformed this year is we’re relatively decoupled from the S&P 500. My largest holding in the index has a weighting of just 0.26%. The other stocks I hold don’t even register, including my largest financial stock—a regional bank which despite a 63.6% return over the last 12 months still has a market capitalization of just over $600 million.

Shunning exposure to the S&P 500’s biggest names has been a big plus for portfolio performance this year, as it was in 2025. And it figures to be a winning strategy for the next 3 to 5 years, as the market’s premier index rebalances toward the emerging leaders and away from the old and increasingly weary.

The Bullish Side of OEF Fallout

How likely is a major correction this year that would take down everything? The investment media and therefore probably most investors expect the outcome of Operation Epic Fury to determine that. And despite Friday’s relief rally, it’s a fair bet that if the situation eventually spins out of control, a major selloff will follow.

We’re Americans. We don’t expect to lose. And for 250 years, we never have when it’s really counted in geopolitics—though few would count the military actions this century in Afghanistan and Iraq as real victories, or what happened in Southeast Asia in the previous century.

Could something truly catastrophic come out of the current conflict in the Middle East? It doesn’t seem likely to me, though the fog of war is still hanging over everything.

There’s even a good case that Operation Epic Fury fallout is hyper-bullish for the US longer-term, particularly concerning energy.

US oil and natural gas exports now command a safety premium. So does the output of our Australian and Canadian allies. And that’s likely to be the case for years. Even if there’s no further damage to Gulf states’ energy infrastructure—and what is out of commission is repaired quickly—the force majeure on contracts declared by regional producers lives on as reputational damage.

Second, there’s the cost of generating electricity as AI competition heats up. Power is increasingly the critical factor for supporting artificial intelligence’s potential to revolutionize efficiency and capability throughout the global economy.

The US and Canada have cheap natural gas that’s critical to meet incremental electricity demand for AI at a low enough price. The rest of the world does not, including Europe where AI “tokens” needed to run high level solutions are widely unaffordable.

Much about AI’s real potential is still unknown. And it’s a safe bet many of the benefits currently trumpeted by proponents are overblown. But it’s also fair to say the world is only now scratching the surface on what is possible, what’s worthwhile and what could really provide breakthroughs.

Now the pace of development is speeding up. And the countries able to afford the energy to get at these solutions—especially the US—have the potential to vault years ahead of the rest of the world in a relatively short period of time.

That’s bullish for the US. And a real AI revolution represents a great deal of business for the 7 Big Tech companies that dominate the S&P 500. But at these prices, their stocks are wholly unmoored from any reasonable measure of business value. And that makes them and the S&P 500 they dominate uninvestable.

Like the Big Tech companies in 2000 that drove the information technology revolution, today’s leaders trade on price momentum alone. And the primary reason for buying these stocks is not undiscovered value but the firm belief someone else will come along to pay more later.

That’s not a way to make money investing, at least with any consistency. But there are still very real ways to bet profitably on America’s growing energy advantage developing AI. That includes utilities, renewable energy power producers, pipeline companies and oil gas producers, all of which are well represented in this portfolio.

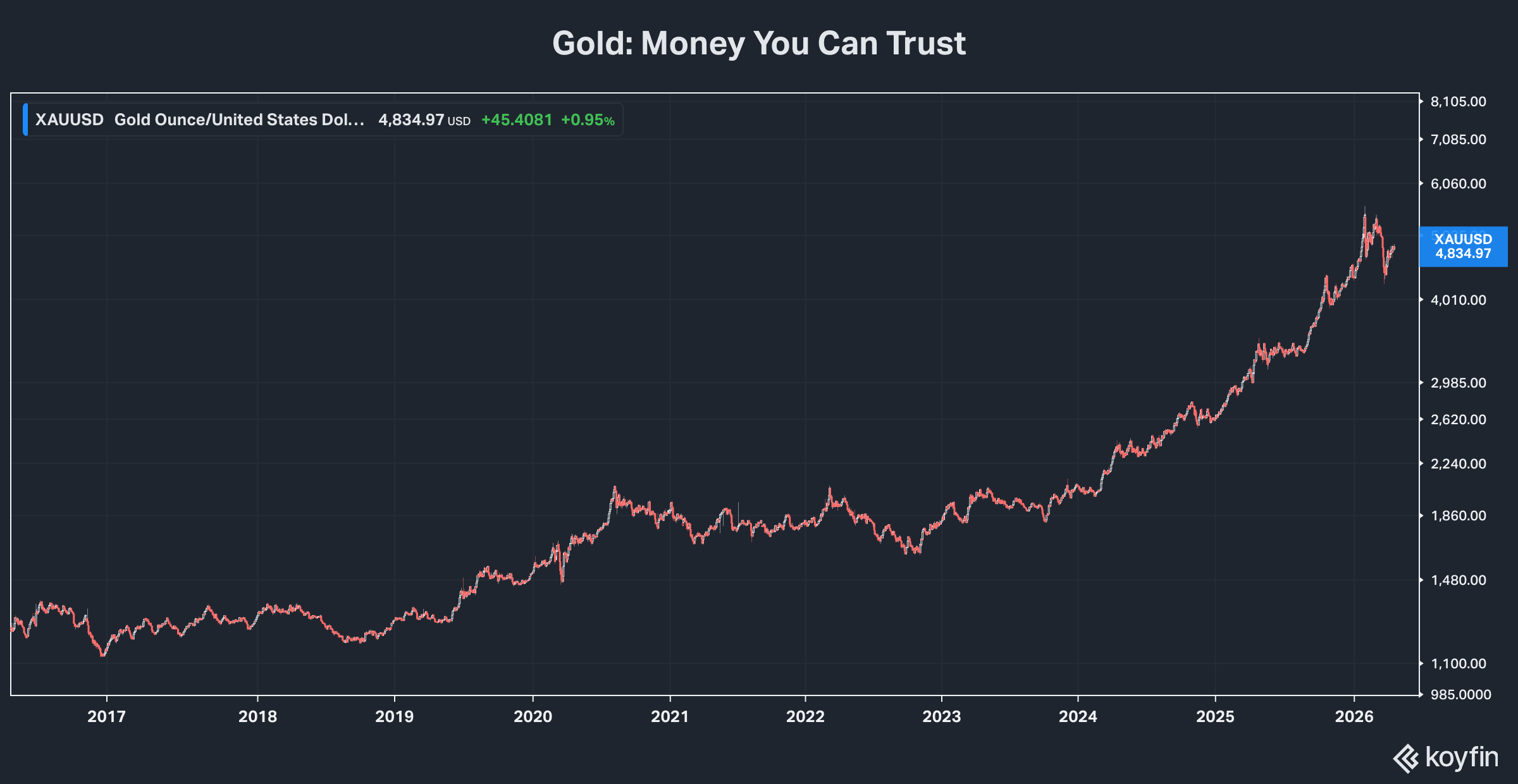

Gold is Flashing Green Again

Ironically, these are the stocks many investors sold on Friday, as the countertrade to the rest of the stock market. And as a result, there’s another opportunity to build positions in the companies highlighted later in this report.

Even top-quality energy-related stocks would be vulnerable to a real 2007-09 style bear market. So, if Big Tech does wind up giving up the ghost here—on an ultimately less than savory outcome for OEF or some other reason—it’s likely they’ll see some selling. But these stocks are nonetheless worth building positions in when they trade at good entry points.

So are best in class gold stocks.

There are many reasons to own gold in spring 2026. Geopolitical turmoil has been and remains one of them. OEF fallout has been at the top of the list. But there are other potential hot spots as well.

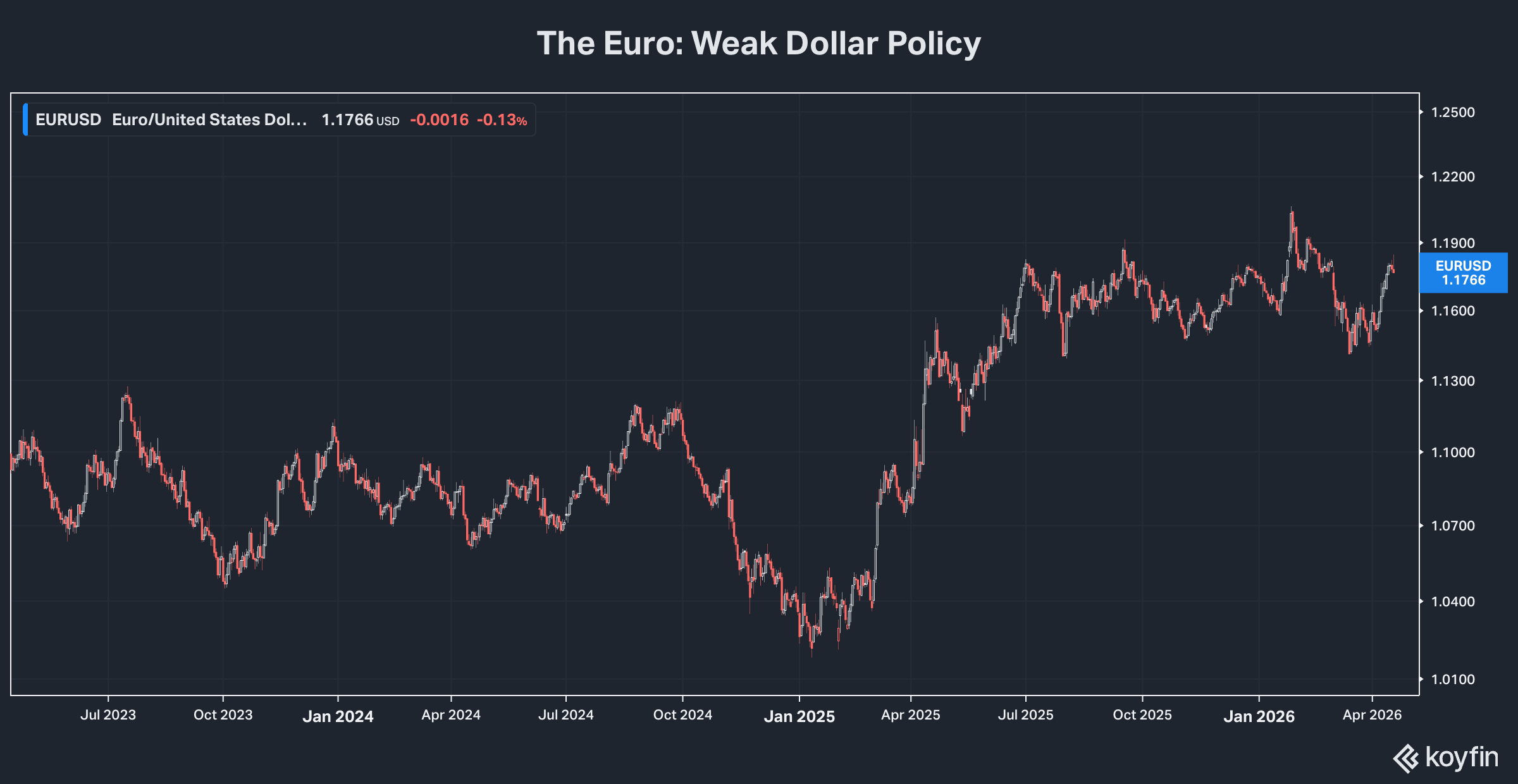

The Trump Administration’s never openly acknowledged weak dollar policy is another reason. Since the president took office, the US Dollar Index (DXY)—a basket of currencies—has slumped from over 110 to 98. Meanwhile, the Euro has risen from around parity over $1.18. And the British pound has moved from $1.20 to $1.40.

It’s hard to argue that a sharp rise in the pound and Euro has anything to do with economic strength in the home countries. And in fact, it’s arguably hurting foreign tourism there, always a key driver of growth.

But the impact has made US products and services cheaper in Europe than they were during the Biden Administration. That appears to be a key Trump Administration goal, fixated as it is on the trade deficit as a barometer of US economic strength. And so long as that’s the policy, it’s a plus for gold.

Then there’s inflation and the Federal Reserve. OEF has chased the Trump Administration’s pressure campaign on the central bank out of the headlines. But it hasn’t let up by any means.

Last week, the president threatened to fire Chairman Jerome Powell if he stays on when his term running the central bank officially ends in May. That’s a reasonable possibility, as Senator Tillis (R-NC) has blocked consideration of Kevin Warsh as Powell’s replacement until the White House ends its investigation of alleged mismanagement of Fed building renovations.

The president’s beef with Powell has of course been the chairman’s refusal to cut the Fed Funds rate as much as he’d like. The target rate remains between 3.5% and 3.75%, following the resumption of incremental decreases last year. But the central bank has put future cuts on hold, following the release of data showing an uptick in underlying inflation.

The Fed’s long-term goal is for its preferred measure of inflation—the Personal Consumption Expenditures Index (PCE)—to maintain an annualized rate of increase of 2%. It’s been willing to cut Fed Funds even with PCE above that level, on the belief that inflation was heading lower.

But recently, OEF fallout combined with tariffs and other global supply chain disruption has increased uncertainty. And that’s clearly raised the level of caution among the voting members of the Federal Open Market Committee (FOMC), which decides when to cut or raise Fed Funds—and by how much.

Notably, last week Fed governor Stephen Miran—in the past a supporter of more aggressive Fed Funds rate cuts than the majority of FOMC—stated the “inflation backdrop has deteriorated” since late 2025. And he didn’t chiefly blame OEF fallout but rather noted “a broader set of sectors contributing to price pressures,” suggesting inflation has become “more entrenched.”

That suggests Powell’s pending exit as chairman won’t necessarily usher in a Fed that’s more compliant with the president’s wishes. Neither does his prospective replacement Kevin Warsh, historically an inflation hawk who was likely picked in part to quell fears about future Fed credibility.

But any perception that the Fed is acting as adjunct to the White House would be extremely positive for gold prices going forward—as it was last year. And combined with persistent inflation, that could easily take the yellow metal to $6,000 an ounce and possibly higher, particularly if combined with increased geopolitical uncertainty.

Gold’s rally on Friday—the day Iran’s opening of the Strait of Hormuz was prematurely announced—is a crystal clear sign there are other factors spurring the metal higher. And they appear to be strong as ever.

I prefer gold stocks to the metal itself because the price of gold doesn’t have to rally for investors to reap a windfall the rest of this year. That’s in part because leading miners are arguably still more priced for gold in a range of $3,500 to $4,000 an ounce, rather than the current $4,500 to $5,000 level—let alone $6,000.

Here are the ones to watch: