Building a Dividends Portfolio to Last

Q3 results are investors' latest and best opportunity to separate winners from losers.

Editor’s note: Thanks for reading Dividends Roundtable! In this post, I highlight what we’ve learned so far about the health of corporate America from Q3 earnings results, and what that means for us as dividend investors. See the links in this email to find out more about Dividends Premium, Dividends Premium REITs and the Dividends Roundtable forum I host 24-7 on the Discord application.—RC

Paying a generous and sustainably growing dividend: That’s perhaps the surest outward sign of a company’s inner strength.

Investors who buy and hold such stocks will see income grow reliably year after year. And you’’ll reap substantial capital gains as well, as the underlying businesses become more valuable, and stock prices rise.

In my view, building a diversified and balanced portfolio of just 12 to 15 high quality dividend stocks is the surest road to real wealth in the stock market long-term.

And some years the reward just for being patient with an underperforming stock(s) one year can astound you the next. Even with a few notable laggards, Dividends Premium model portfolio stocks are up 27 percent on average year-to-date.

Companies with reliably growing dividends are all around us. Some sectors have more than their share of potential targets, for example regulated utilities, midstream energy and real estate investment trusts. But suitable candidates can literally be found across the industry spectrum, from super oil majors and big pharma to regional banks and mining companies.

Two things set a real wealth building dividend stock apart: The health and growth trajectory of the underlying business, and the stock’s price.

If you pay too much for a company, you’ll never realize more than a mediocre return from its stock. That’s a fact all too many investors ignore when they chase a hot sector that’s already produced big gains. Not only are they buying high. But when the tide inevitably turns, they’re at risk to large losses.

Equally important to success buying high quality dividend stocks is discerning company quality. I use a five criteria system developed based on investment lessons learned over 40 years in the advisory business.

I highlight the quintet in the September 28 Dividends Roundtable post “When a Dividend is Safe, Or Not.” Check it out on the Dividends Roundtable Substack webpage.

The five criteria are dividend policy relative to earnings growth, revenue reliability, regulatory/legal risk, balance sheet strength and operating efficiency. The numbers I use to assess each criterion may vary by company and sector. But taken together, they provide us a pretty good assessment of whether a company is in shape to continue growing and paying us a rising stream of dividends.

Markets change. And even the best performing companies can stumble. So the process of assessing good health is dynamic.

Fortunately, all the information we need to do the job is available to anyone with Internet access who is willing to spend a little time learning. And ongoing Q3 earnings reporting season is our latest best opportunity to do that.

Before we go any further, I have a confession to make. I’m a crusader for financial literacy. And nothing energizes me more professionally than convincing an investor that they can pick their own stocks—either by doing their own analysis of the primary data from earnings reports or consulting with an advisor or service who will do that work for them.

Giant Wall Street marketing machines like Blackrock and Vanguard have spent a fortune over the last decade convincing investors they shouldn’t try to take charge of their investment decisions. And unfortunately, they’ve been more than a little successful: For the first time in history, there’s more stock market money invested in passive funds than is actively managed.

Don’t get me wrong. Having money passively invested in stocks—mainly in giant index-based funds that never change except by pre-determined algorithm—is better than not being invested in the market at all.

But even in the best of times, you’re only going to have average returns by going passive. You’re not going to learn anything about the stock market by abdicating your decision making. And you’ll have no one to blame but yourself if we are indeed entering a lost decade for the S&P 500 index, the cornerstone for the vast majority of passively run funds.

Why? Because the index is historically over-weighted in just 7 Big Tech companies comprising 37.22% of the index. And those stocks are historically expensive: The S&P 500 overall sells for historically high valuations of 30X earnings, 42.5X free cash flow , 13.2X tangible book value and a yield of barely 1%.

That’s basically where the stock market was in early 2000. And the aftermath was lost decade for the S&P 500. It took years to fully re-balance from sinking Big Tech to sectors like energy that made real money in the ‘00s.

I really can’t blame the Wall Street giants for not talking much about the ‘00s. The primary selling point for passive investing products is very low fees. The sponsors put almost no effort into running them. But profits can only grow by sucking in more investment dollars. And that won’t happen if enough investors have the confidence to make their own decisions.

Fortunately, the dominance of Big Tech in the S&P 500 means that other sectors with stocks paying big dividends are both underowned and undervalued. The average yield of the 84 real estate investment trusts I track in the October issue of Dividends Premium REITs (posted last week), for example, is nearly 6%. And many of the companies trade near the book value of their properties, which is generally lower than market value.

I’ve talked at length in Dividends Roundtable recently about high quality midstream energy companies yielding 8% and higher. Equally, there are multiple bargains in the utility sector offering a combination of 10% plus in yield plus annual dividend growth. And some big pharmaceutical and communications companies pay over 7%.

Bargains are all around us. The key to success is doing your due diligence to ensure the dividend policy is sustainable. And the way to do that is to use the most recent earnings results and guidance updates to assess how companies stack up on the five ratings criteria.

Over the next few weeks, I’ll be putting Dividends Premium and Dividends Premium REITs companies through that prism. But here’s what we know so far from the handful that have already reported.

First, tariffs are starting to take a bite out of earnings for companies importing to the US. But best in class companies are adjusting. And the result for them is not nearly as ugly as it appeared it would be back in April.

For example, energy services company Baker Hughes (NYSE: BKR) set a range of losses from tariffs of $100 to $200 million in April. It’s now guiding to the low end of that range. And Q3 earnings were up 9% from Q2.

The key for Baker in shaking off the tariffs was robust sales including of imported equipment sold to data centers and pricing power. And I expect other high quality companies taking a hit from import costs to demonstrate the same resilience in their Q3 results.

Electric utility Centerpoint Energy (NYSE: CNP) has affirmed its guidance for 2025 and 2026. The key factor is robust demand for electricity, including astronomical 17% year-over-year growth in industrial demand. And rising power demand should also more than offset tariffs’ negative impact on earnings for other electric companies with robust investment plans, including operators of renewable energy projects.

That’s positive for utility companies’ dividend safety. So is oil and gas companies’ continuing focus on cutting costs at a time of soft commodity prices.

EQT Corp (NYSE: EQT) raised its dividend this month for the first time in two years. And Q3 results demonstrated how: The company cut operating costs to a record low. It also reduced CAPEX 10% below the mid-point of guidance while producing “toward the high end of guidance.”

Energy midstream company Kinder Morgan Inc’s (NYSE: KMI) robust natural gas pipeline and infrastructure construction pipeline ($9.3 billion) is heavily pre-contracted, tapped into powerful growth of artificial intelligence and LNG exports. The company is still on track to beat initial 2025 earnings guidance, as it “continued to internally fund high quality capital projects” under long-term contracts. And the results are promising for other best in class midstream companies yet to report.

T-Mobile US’ (NSDQ: TMUS) highest quarterly customer additions “in over a decade” apparently didn’t impress investors, as the stock sold off following its strong Q3 earnings report. So did AT&T Inc’s (NYSE: T) shares following a solid result.

Verizon Communications (NYSE: VZ) has also taken a hit, though it won’t announce Q3 numbers and updates guidance until later this week. But it’s clear from the numbers that these three companies are still building market share at the expense of the rest of the industry. And that adds a solid vote of confidence for dividend yields that are as high as 7%.

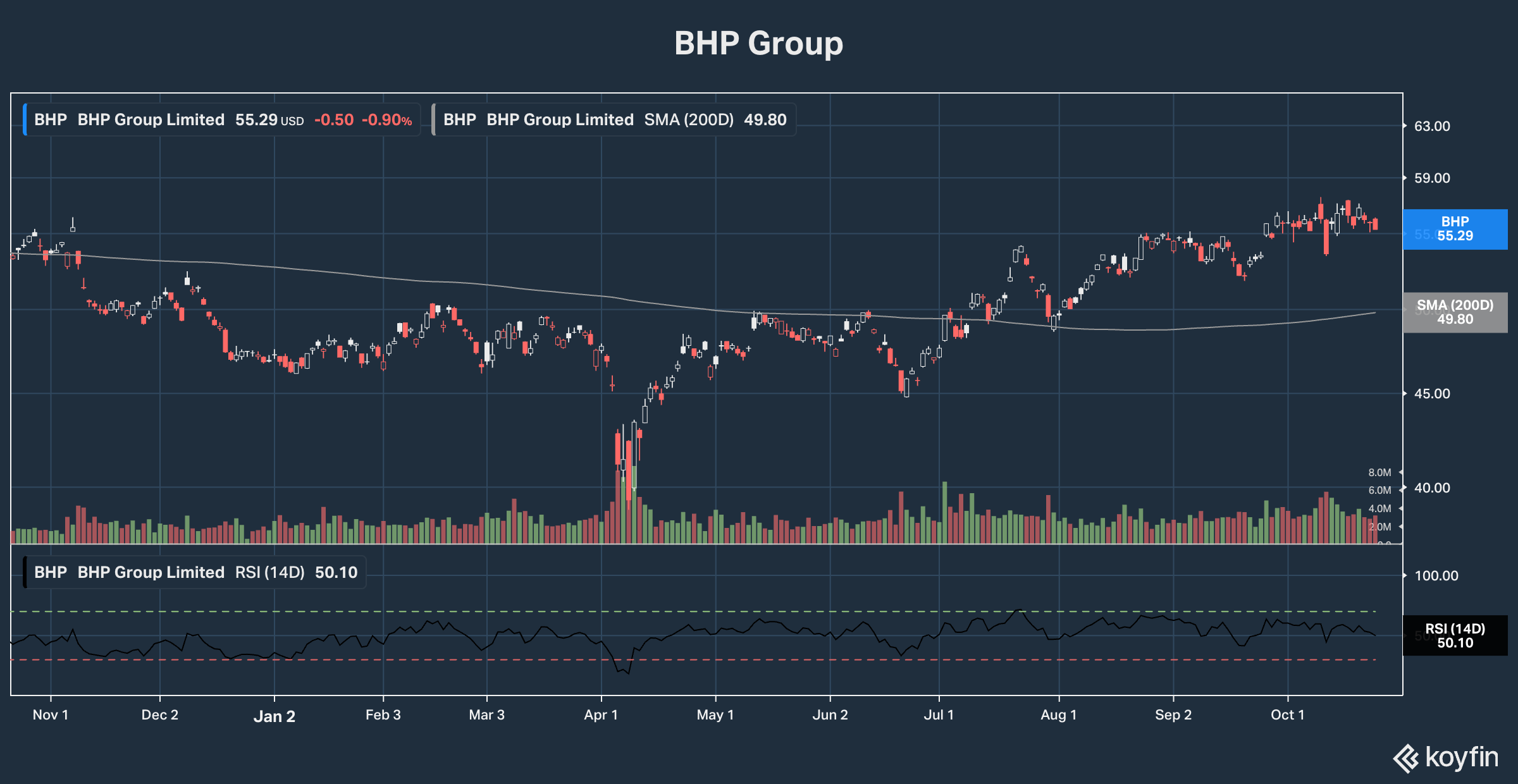

UK and Australian companies typically release full financial results only twice a year. But BHP Group (ASX: BHP, NYSE: BHP) reported solid operating results for its fiscal year Q1 (end September 30). That included a 4% boost in copper production, supported by 8% higher output at the Escondida mine in Chile.

The most important thing all of these companies had in common with their Q3 results is they delivered on management’s previous guidance. I consider that essential to whether we want to own a company’s stock.

Mainly, if management cuts guidance it means one of two things. One, there were outside factors it did not foresee when it issued initial guidance. Two, the company itself failed to execute.

Even the strongest companies occasionally stumble. In an unforgiving market like this one, even slight misses can send a stock reeling quickly. And such reactions often well overshoot. So it often makes sense to stick and see if management can turn things around. A second consecutive guidance miss, however, is a definite sell signal.