Buy Like Buffett in 2026

Quality is still king and slow and steady wins the race!

Warren Buffett has stepped down at Berkshire Hathaway (NYSE: BRK A/B). That’s the investment company he founded in 1962, the year after I was born.

I say he’s more than entitled to: The man’s 64 years of hard work has raised the price of a Berkshire A share from $7.60 to over $740,000.

Buffett’s “secret” is really no mystery: He consistently built meaningful positions in high quality companies when they were cheap.

Over the years, his targets ranged from insurance companies, banks and early-stage Apple Inc (NSDQ: AAPL) to oil companies, railroads and utilities. Not all of the investments worked out, processed food company Kraft Heinz (NYSE: KHC) a recent example. But over time, the aggregate did spectacularly, as Buffett and his team stuck to strategy.

I’ve been a happy owner of Berkshire’s far more affordable B shares for a quarter century. Successor Greg Abel will almost certainly do some things differently. But so long as the basic approach is buying quality companies on the cheap, I’ll be content to hang in for the next 25 years.

Sticking to cheap stocks has special importance in 2026. The 7 largest Tech stocks that have led the market higher the past few years are both historically overweighted at 37.6% of the S&P and off-the-chart expensive. And they’re all tied in one way or another to a single investment theme: The artificial intelligence revolution.

All of that has been true for a while. But historically extreme market concentration has never ended well for anyone staying too long at the party. And more money in the US stock market is now passively invested than actively managed, which means it’s tied up in Big Tech heavy S&P 500 and related ETFs. So, fallout from a correction could be devastating to more retirement accounts than the 2000-02 Tech Wreck.

When the big averages drop rapidly, almost every stock is going to slip. But investors who like Buffett have built positions in high quality businesses on the cheap will avoid the worst of it. Their stocks will also be the first to recover. And if the latter ‘00s are any guide, they’ll lead for years as the S&P 500 rebalances towards them.

How likely is a major stock market correction in 2026? Selloffs are quickly forgotten if recovery comes fast enough. But they’re far more common than you might think.

In the first nine months of 2022, for example, the S&P 500 responded to the Federal Reserve’s upward push on interest rates by dropping around 1,200 points. It fell a like amount in early 2025, as the Trump Administration announced increasingly large tariffs.

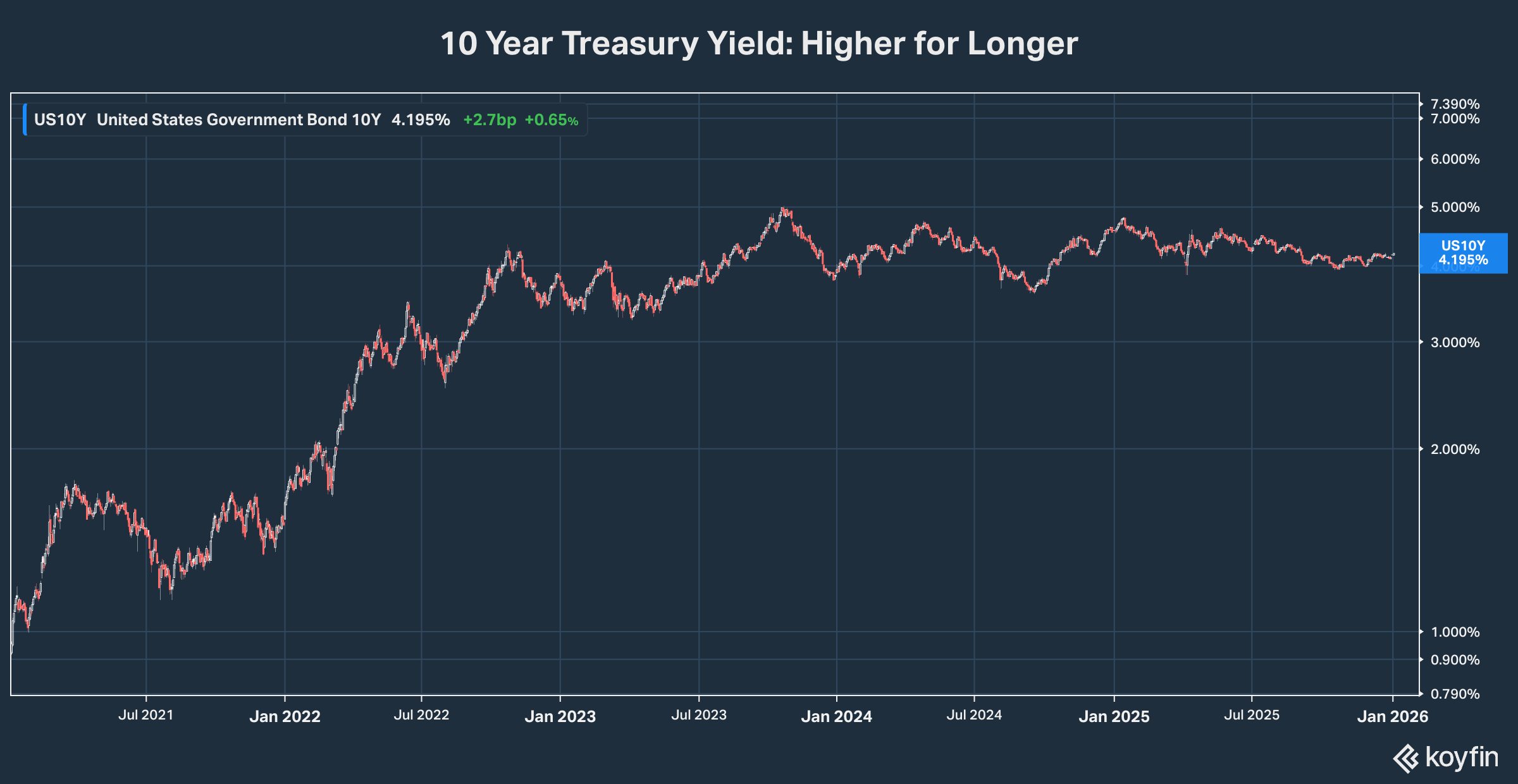

Inflation expectations are a potential selloff catalyst this year. The government will play catchup on economic data for a while. But inflation expectations are elevated on Wall Street as well as Main Street:

Exhibit A is last year’s big rise in gold prices. B is the failure of long-term interest rates to follow Federal Reserve rate cuts lower. And C is the rise of an “affordability crisis” as a primary election theme. Affordability played a huge role in Democrats’ landslide wins in several states last November. And at this point, it seems likely to play an even bigger role in voting this November.

I can make a pretty good case why faster Federal Reserve rate cuts—such as President Trump is publicly pushing for—will fire up the stock market. Historically, investors love nothing more than liquidity. But there’s also risk that a Fed perceived as too willing to please politicians won’t be serious about controlling inflation.

That would be great news for metals and mining stocks. And I intend to hold a solid portion of them in Dividends Premium.

A further rise in inflation expectations, however, would keep real borrowing costs elevated.

Most of the dividend cuts we saw last year were a direct result of management holding in cash to cut debt. Many companies throttled back or halted dividend growth for the same reason. And the longer borrowing costs remain elevated, the more companies will follow their example.

Fortunately, you can inoculate your portfolio against dividend risk by doing the same thing you’d do to protect against the worst of a Tech Wreck. That’s following Buffett’s way: Building positions in high quality companies that aren’t expensive.

What exactly is a “high quality” company? I use five basic criteria in my searches:

· A dividend policy that’s sustainable for the company’s specific business.

· Revenue that will reliably grow over time and be strong enough to maintain investment plans, dividends and balance sheet strength in tough environments.

· Manageable legal and regulatory risks.

· Balance sheet strength. Investment grade ratings will be increasingly important if supply chain disruption weakens the US economy this year.

· Operating efficiency. Does the company run its assets well? Is it able to control its costs?

Every business is different. And that means criteria will vary as they apply best to specific sectors and individual companies.

These criteria are also self-reinforcing. A business that scores highly on at least two will likely measure up well on all of them. Conversely, a company that fails on one or more criteria is less likely to pass muster on any.

What dividend sectors are ripe for the picking this year? Renewable energy stocks enter 2026 with a lot of momentum. After dropping roughly -70% during the four years of the Biden Administration, the Invesco Solar ETF (TAN) gained nearly 50% in 2025. And top quality, dividend paying stocks like Clearway Energy (NYSE: CWEN) have de-risked their investment plans and are still not expensive.

US communications had a generally weak 2025 on worries about what Elon Musk will do with spectrum acquired from Echostar (NSDQ: SATS). But the Big 3 of AT&T Inc (NYSE: T), T-Mobile US (NSDQ: TMUS) and Verizon Communications (NYSE: VZ) continue to aggregate wireless and broadband market share. And Verizon still trades for less than 9 times earnings.

A recovery in oil prices should mean a better year for energy midstream companies. And while battered real estate investment trusts still face headwinds, the best in class are as cheap as they’ve been in decades relative to property values.

Bottom line: Opportunities to buy like Buffett abound in 2026. And ignore the usual start of the year hype. You can take your time looking. Slow and steady still wins the race.