Buy REITs, Beat Inflation

Misunderstood real estate investment trusts offer high yields with upside.

Editor’s Note: Thank you for reading Dividends Roundtable special REITs report!

Inflation is rising again. That induced the Federal Reserve last week to eliminate its prior bias to lower interest rates. And the Federal Open Market Committee decided unanimously to leave the Fed Funds rate unchanged, in a range of 3.5% to 3.75%.

The implication monetary policy will stay tighter for longer has since triggered knee jerk selling of most dividend stocks, including REITs. That’s hardly surprising. But the Select Real Estate SPDR ETF and my First Rate REIT list nonetheless closed the week up about 7% year to date, just a couple percentage points behind the Big Tech-leveraged S&P 500.

REITs have made money so far in 2026 in part because of rock bottom investor expectations. But best-in-class companies across property sectors outperformed business guidance in Q1. And there’s every indication they will with Q2 results, which start showing up in mid-July.

REITs continue to be priced as bond alternatives, rather than the inflation beneficiaries they’ve been historically. That too should change with property markets tightening across sectors, and as companies like W.P. Carey (NYSE: WPC) are increasingly able to peg rent increases to inflation.

Carey is one of my top five REIT fresh money picks for this month, highlighted later in this report along with five sector stocks to sell now. And see my REIT Rater for buy/hold/sell advice, business analysis, payout ratios and “Quality Grades” for 81 individual REITs.

Got a question or comment? I host a webchat 24-7 on the Substack application as well as Discord. And look for the Dividends Roundtable application coming soon!

To your wealth!--RC

Follow the headlines! That’s what algorithms now controlling trillions of passively invested dollars are trained to do. And with a 24-7 Internet news cycle, the result is a great deal of sound and fury in the US stock market.

Last week featured two blockbuster headlines: The president’s peace deal with Iran and the Federal Reserve’s move to a more neutral stance on monetary policy. And the resulting volatility made for some exciting day trading.

Big investment media have been breathlessly suggesting big moves afoot—and that viewers had better stay glued to their screens to find out what’s to come. But if you don’t mind my paraphrasing Shakespeare, what we saw last week for stocks really didn’t signify much of anything for investors who want to boost income and build wealth, while keeping liquid for a rainy day.

The point of this report is to help you build positions in top quality real estate investment trusts, when their stocks sell at good entry points. Secondarily, I highlight when a particular REIT has reached a price where it makes sense to take a partial profit. And to accomplish these objectives I follow the following four rules:

· Own only REITs with underlying businesses that are growing and getting stronger. Q2 results will start to flow in about a month. For now, the best clue of what we’ll see then is in my analysis of Q1 earnings and guidance updates, found in the “Commentary” column of the REIT Rater databank. For more information on this comprehensive table of 81 REITs, see the “Key Points and Ground Rules” discussion at the end of this report. I also now feature my A (safest) to F (riskiest) Quality Grades, to give readers a more comprehensive assessment of risk.

· Do not chase REITs above my highest recommended entry points. And take new positions in increments of three, rather than all at once—even if stocks are at Dream Buy prices. This is basic dollar cost averaging. Follow this rule and you’ll always buy more shares at the lowest price.

· Take profits in big winners when they trade above “Profit Taking” prices in the REIT Rater table. These stocks are trading at price levels that have not held historically. It’s time to take at least some of the money and run!

· Never load up on any one REIT. Always balance and diversify your portfolio. The corollary is I never double down on a falling stock to reduce cost basis.

I follow this rule not because I don’t trust my analysis. In fact, I’ll frequently stick with a fallen REIT, provided the business still looks solid.

But we’ll never have perfect knowledge of what’s going on at any company. And doubling down on a position often introduces emotion into decision making. Mainly, it gets harder to pull the plug if I’m wrong.

Most important, if one of your stocks has dropped sharply, chances are other high-quality REITs have as well. You’ll maximize your chances of riding a recovery by spreading your cash around. And doing so cuts risk to your portfolio from stocks that ultimately don’t work out.

Focus on the Micro

So-called “big picture” issues affecting the economy—including geopolitics and war—are only important to us in how they affect the “micro.” That’s the health and growth prospects of the companies we own. And the situation is often a lot different if you’re looking at it on the ground, rather than from 30,000 feet up.

Macro issues are important for REITs. Stronger growth is always better for commercial property occupancy and rent growth, as well as collection rates. And the direction of interest rates affects funding costs. Higher rates, for example, raise the bar for investment returns. And they raise the cost of refinancing maturing debt as well.

All else equal, lower interest rates/borrowing costs mean more investments make sense. And because the property business uses a fair amount of debt, lower rates keep a lid on debt interest expense when it’s time to refinance.

All else, however, is not always equal in the commercial property business. And some REITs are dealing with higher for longer interest rates better than others.

Since last month’s REIT report, for example, 10 companies in the REIT Rater coverage universe have announced and executed bond sales. That includes several issuances that were ultimately upsized.

Data center owner Iron Mountain (NYSE: IRM), for example, was able to increase a $1 billion offering of 6.25% bonds maturing in 2035 to $1.5 billion. Retail REIT Kimco Realty (NYSE: KIM) boosted a sale of 3.5% exchangeable notes due 2031 to $525 million from $500 million. That’s very low-cost money. And with the notes carrying an initial exchange price of $32.36 per share, they’ll only be converted if Kimco shares appreciate at least 33% from their current level.

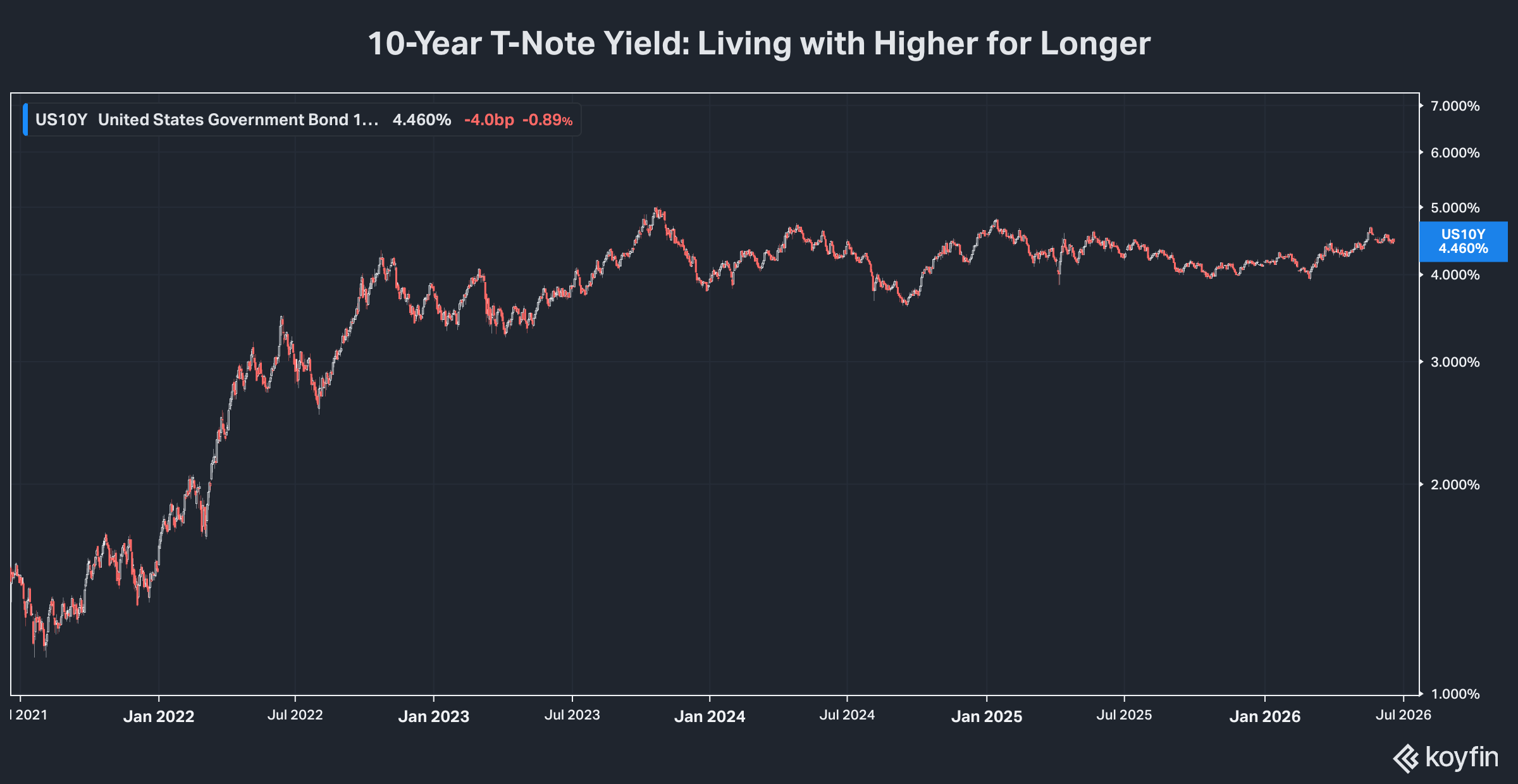

No doubt, these REITs and the other 8 issuing debt would have preferred a lower benchmark 10-year Treasury note yield by this time. And selling bonds now could be fairly interpreted as tacit acknowledgement this is the best they’re going to do for a while.

Some of the issuance, for example, is to refinance maturing debt that has a lower interest rate. Innovative Investment Properties (NYSE: IIPR) was able to upsize an offering of convertible debt from $250 to $350 million. And like Kimco’s convertible sale, the “initial exchange price” of $69.39 is well above the REIT’s current price. But the private offering’s interest rate is 6%, versus the 5.5% the REIT was paying on the senior notes that matured in May.

That means Innovative is likely to see debt interest expense rise going forward, putting a further strain on its $1.90 per share quarterly dividend. So will Outfront Media (NYSE: OUT), which has issued $500 million of senior notes due 2034 with an interest rate of 6% to pay off bonds maturing in 2028 with a rate of just 5%. And Starwood Property Trust (NYSE: STWD) sold $600 million of notes due 2031 paying 6.125%, using $400 million of proceeds to pay off notes maturing this year paying just 3.625%.

Starwood’s debt interest expense rose by 12.6% in Q1 from last year. And it’s a safe bet that earnings will be further pressured by higher costs going forward. That will further reduce the margin for paying a dividend that was 123.1% of Q1 distributable earnings.

Nonetheless, these bond issues are the most we’ve seen sector wide in some time. And they’re a clear sign that, whatever the Fed is doing, investors are still willing to buy REIT debt at reasonable prices.

That’s good reason to expect more REITs to raise investment targets for 2026, and by extension guidance for adjusted FFO. Several already have, including W.P. Carey (NYSE: WPC).

Simply, there’s no magic level of interest rates that’s bullish across the board for property companies. Neither is there a level that’s universally bearish.

What matters is how the individual REIT is positioned. And a growing number are finding investments that can earn strong returns at the current level of interest rates—including with acquisitions, mergers, new development of properties and redevelopment of existing stock.

LTC Properties (NYSE: LTC), for example, projects annual internal rates of return in the “low to mid-teens” percentages for its aggressive SHOP (senior housing) investments. That compares to the cost of the REIT’s current senior debt, which has coupon interest rates between 3.66% and 4.5% and maturities between 2026 and 2033.

LTC is almost surely going to have to refinance a good chunk of that debt at higher interest rates in coming years. And in fact, Q1 debt interest expense was already 36.3% higher than a year ago, though that mainly reflects cost of debt to fund SHOP acquisitions. But even at coupon rates twice current levels, returns on SHOP investments will be strongly accretive to the bottom line.

Not every REIT sector is handling higher for longer interest rates well. High dividend yields offered by mortgage/financial REITs should be considered especially at risk in the current environment.

KKR Real Estate (NYSE: KREF) enjoys the backing of giant, diversified private capital firm KKR (NYSE: KKR), which also owns 14% of the company. And from all indications, portfolio restructuring is laying the groundwork for stronger future returns. But the REIT nonetheless cut its quarterly dividend by -60% to 10 cents per share, effective with next month’s payment.

The reason: A need to re-set the payout to where it’s supported by the current spread between the REIT’s cost of capital and available returns on investment with acceptable risk. That’s the same imperative that forced Franklin BSP Realty Trust’s (NYSE: FBRT) -43.7% dividend cut earlier this year, despite the support of a solid parent in Franklin Resources’ Benefit Street Partners.

Interest rate pressure is also good reason to be wary of other financial REITs that have yet to cut. That includes Redwood Trust (NYSE: RWT), which just sold $125 million of bonds maturing in 2031 with a coupon interest rate of 9.75%. The REIT’s dividend is currently just 53% the pre-2020 pandemic rate. But coverage is thin. And both economic returns and book value per share have relentlessly fallen over the past year.

It’s fair to say the current yields on mortgage/financial REITs already reflect severe dividend cut risk. But consider KKR Real Estate shares dropped sharply following the dividend cut and are lower by -14% year-to-date. Franklin BSP is down -16%. So it’s reasonable to expect other M-REIT cutters will get sold if they have to cut payouts in coming months.

There are no financial REITs currently on the First Rate REIT list for this reason. And my preference is to avoid this group while their shakeout/dividend re-sets continue.

But the larger point here is higher for longer interest rates are not necessarily an earnings and dividends killer for REITs. Some are learning to thrive while others are still adjusting.

REIT Mergers Heat Up

Also in the past month, we’ve seen our second mega-REIT sector merger, between leading residential property owners AvalonBay Communities (NYSE: AVB) and Equity Residential (NYSE: EQR).

Based on this merger-of-equals’ exchange ratio of 2.793 EQT per AVB share, our AvalonBay will get an effective dividend increase of about 10% at the close. That’s expected to happen “in the second half of 2026,” following a shareholder vote at both REITs.

The deal’s real benefits are long-term. Roughly 95% of the REITs’ markets overlap. And management has identified $125 million of “net synergies after real estate tax reassessments” it can realize within 18 months. That should flow right to the bottom line, as the combined company deploys a projected $2 billion of “annual cash flow and self-funding capacity.”

Then two REITs currently have a total of 10,800 apartments under construction ($4.4 billion), as well as a $4.2 billion “development pipeline.” They start out with 180,000 premium properties, A3 (Moody’s)/A- (S&P) credit ratings and plans to self-fund development CAPEX. And during the merger announcement call, management cited numerous opportunities to deploy technology to lift margins and boost occupancy.

The combination should also take advantage of improving business conditions. The residential REIT sector has faced headwinds the past couple years from a flood of new supply, initiated when development costs including interest rates were at meaningfully lower levels. Now supply is tightening.

Presenting at NaREIT’s 2026 Investor Conference, executives of Mid-America Apartment Communities (NYSE: MAA) noted new supply coming into its key SunBelt markets was -40% less than a year ago. That means tighter supply on the way, with rising occupancy and eventually a return to rent growth.

At roughly 2.5X the size of the next largest residential REIT, AvalonBay/Equity Residential will be able to take full advantage of this emerging tailwind. And their example is likely to spur further sector consolidation, as other residential property owners find ways to profitably bulk up. And I’ve identified several good candidates for M&A in the REIT Rater.

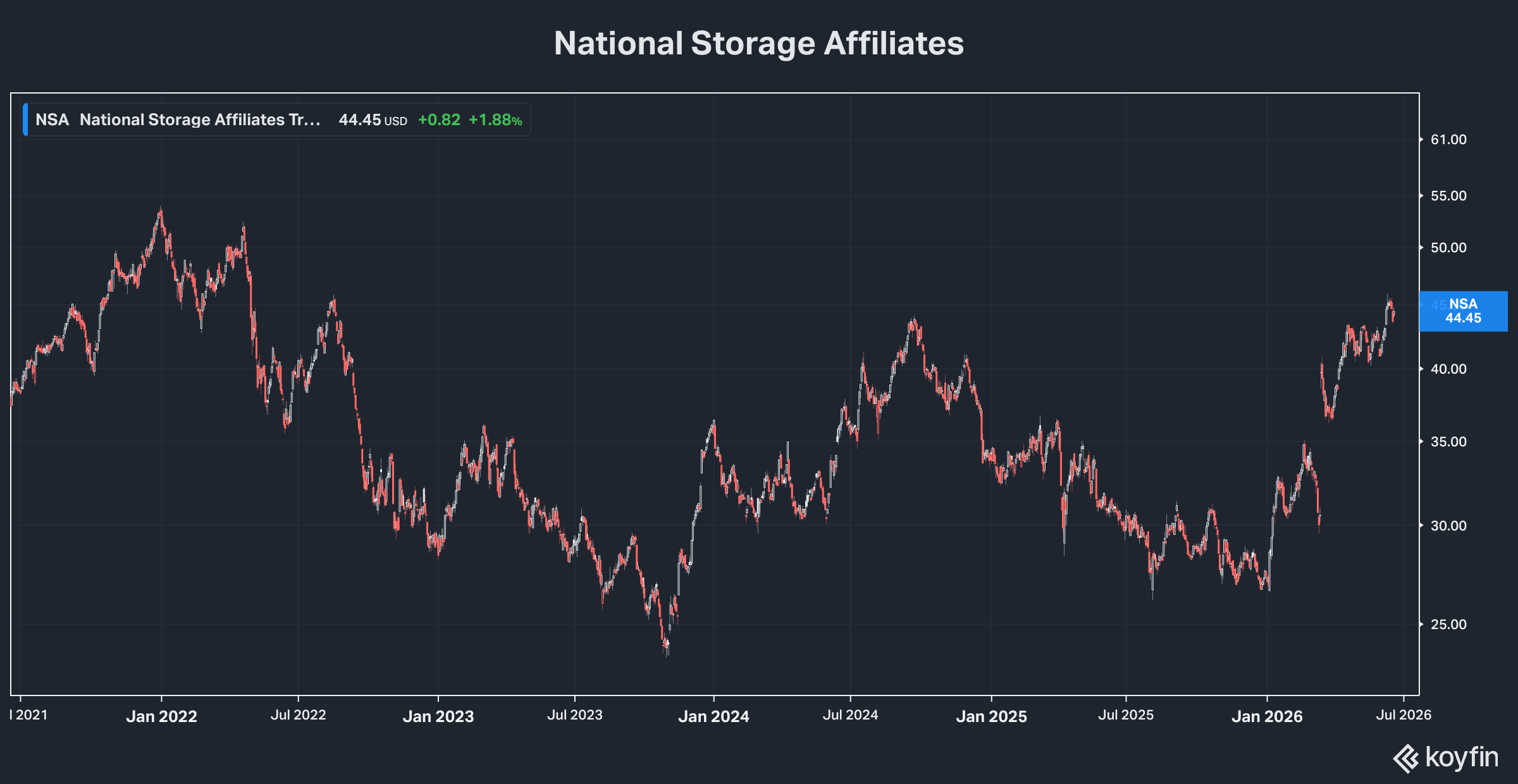

The other ongoing mega-deal in the REIT space now is between self-storage owners National Storage Affiliates Trust (NYSE: NSA) and Public Storage (NYSE: PSA).

As with residential property, self-storage REITs have dealt with a supply glut that now appears to be contracting, with far fewer new facilities coming on the market now than in the past few years. That’s good news for this combination, which will be number one in the sector after a projected Q3 close.

At the exchange rate of 0.14 share NSA per PSA, there’s an implied dividend cut of -26.3% for National Storage shareholders. But that’s more than made up for by the hefty premium Public Storage has offered.

If this deal should come apart for any reason, National Storage shares will likely drop back towards where they traded before the offer, which was high 20s/low 30s. Based on Public Storage’s closing price this week, its offer is worth $44.54 per National Storage share. That’s just pennies higher than the current price for NSA shares ($44.45). And at the same time PSA is trading above my highest recommended entry point of 300.

I like this deal. And I expect it to create a much larger and stronger REIT than even PSA is currently. The storage segment is also likely to do quite well in the next several years as the market tightens. But given the limited upside to the close and the potential downside of highly unlikely deal failure, it makes sense to take the profit on NSA and move onto better values in the storage space, as I identify later in this report.

Six Good Reasons to Buy REITs Now

Bottom line, despite the cloudy macro picture, high quality REITs should add to their gains the rest of the year for these reasons:

· Continuing business momentum that should lead to more earnings beats and guidance increases this summer and into the fall, with occupancy and rents advancing and REIT investment plans expanding.

· More REITs will demonstrate their ability to raise debt capital on favorable terms relative to prospective investment returns. That’s even if benchmark interest rates remain higher for longer and Federal Reserve monetary policy becomes more restrictive to fight inflation.

· More REITs will decide to merge, as management looks for ways to boost margins by cutting costs and growing investment.

· REIT shares are still historically under-owned in the major stock market ETFs that dominate passive investors’ portfolios. The sector, for example, is only about 1% of the Big Tech-focused S&P 500. That makes REITs increasingly attractive as alternative investments that are less exposed to a long overdue 20% correction in the big market averages.

· Share prices relative to business value remain historically low, with many REITs trading near book value and yields several times the S&P 500. The average yield for the 81 REIT Rater companies is 5.5%, First Rate REITs are 5% on average.

I also believe REITs will be increasingly attractive going forward for property investments’ ability to keep up and beat inflation.

Both Producer Price (wholesale) and Consumer Price inflation are already running at their highest levels since 2022. The Personal Consumption Expenditures Index—the Fed’s preferred inflation gauge—was at a 3.8% year-over-year rate in April with May numbers due out June 25.

PCE was just 3.3% excluding food and energy. But even that’s well above the central bank’s often stated long-term target of 2% inflation. And in an environment where spiking gasoline and food prices are demonstrably starting to affect the elements of so-called “core” inflation—shelter, transportation etc—it’s likely that PCE will remain elevated this summer, as will CPI and PPI.

More than a few investors been betting that a US/Iran agreement to open the Strait of Hormuz will send oil prices plunging back under $60 a barrel, where they started the year. And they’re banking the resulting lower gasoline and jet fuel prices will bring overall inflation back under control, allowing the Federal Reserve to resume cutting the Fed Funds rate.

We can only hope they’re right. But even after dropping last week on the news of a deal, oil prices are still hanging around in the upper 70s. And the Fed’s removal of rate cut bias language from last week’s policy statement demonstrates clearly that having a new chairman doesn’t necessarily mean lower rates.

The central bank knows full well that cutting Fed Funds won’t bring down real borrowing costs, unless lenders and bond buyers are confident inflation is under control. Conversely, cutting rates with inflation rising is a prescription for even higher borrowing costs. And it now looks like they won’t cut until inflation comes lower, regardless of the president’s wishes.

Will inflation drop later this year? Maybe. But energy prices were headed higher on tightening global supply, long before Operation Epic Fury was launched and Iran’s asymmetric warfare tactics bottled up 15% of global oil and gas. And tariff-related supply chain disruption was already driving up core inflation.

That suggests inflation won’t be so easily quelled. But again, that’s not necessarily bad for the REIT sector, provided companies can handle volatility in the capital markets. And that means the lower share prices resulting from recent selling of top-quality REITs are an opportunity to build positions, not to sell and move to cash.

Top 5 Fresh Money Buys and Sells

What are the top buys in the REIT sector now? With Q2 results and guidance updates more than a month away, I favor REITs that have provided updates in the past month that affirm their investment plans and guidance are on track. And these five REITs have done so: