Canadian Energy: Tariff Winner

Canada’s energy sector is cashing in on turmoil from Mr. Trump’s tariffs.

Happy Sunday and thank you for reading Dividends with Roger Conrad!

Please consider a trial subscription to Dividends Premium. If you do, next week you’ll receive Dividends Premium REITs, including top fresh money buys with safe and growing yields of 7 percent and more.

You’ll also get 24-7 access to the Dividends Roundtable forum I host on Discord. And you’ll get my Dividends Premium portfolio with complete analysis of top performing dividend stocks—including up and coming Canadian pipeline company South Bow (NYSE: SOBO) highlighted later in this article. See this email and the Substack app for more information. To your wealth!—RC

A 145% tariff on advanced Chinese batteries imported for US-made laptops—but zero tariff if that same battery is in a Vietnamese-made laptop, or just 20% if the finished product is entirely made in China:

That’s the latest wacky development in the still-escalating America-versus the world trade war, highlighted at length in my Substack last week “Dividend Stocks and Mr. Trump’s Tariffs.” And pity the White House PR flack whose job it is to argue against The Wall Street Journal’s assertion: “Mr. Trump is making it up as he goes.”

Uncertainty is the greatest enemy of investment. And over the last 10 days, American businesses and consumers have had to digest news of potential import taxes worth hundreds of billions if not trillions of dollars, followed by sharp reversals—some the very next day.

Some may call this the art of the deal. But at least for now, these unpredictable and unprecedented policy zigs and zags have made it literally impossible for anyone to plan intelligently to make large investments.

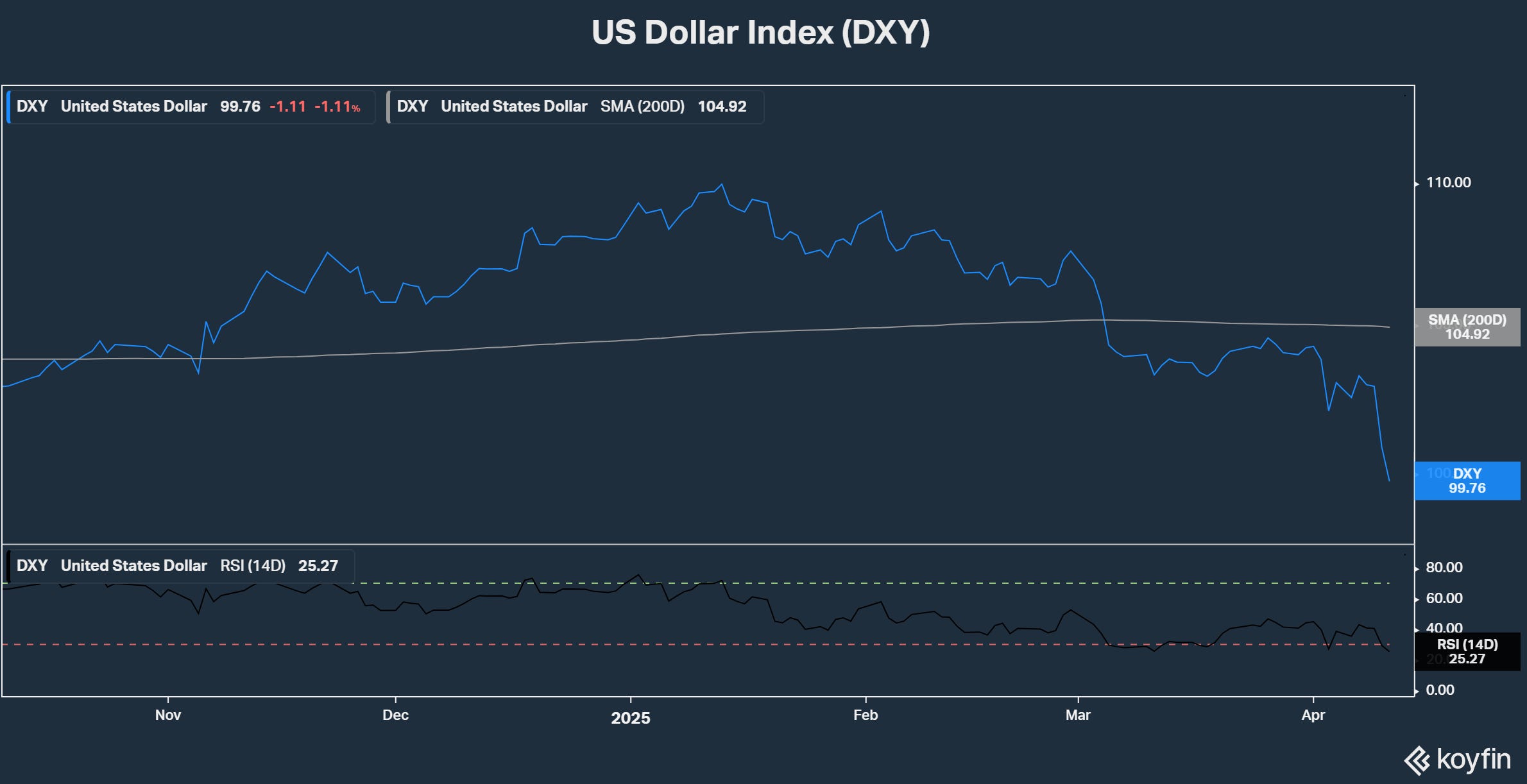

Now add in the impact of suddenly rising interest rates/borrowing costs, the nearly -10% decline in the US dollar since Mr. Trump took office and the S&P 500 increasingly acting like it’s in a bear market. And further adding to the caution, many now believe the US economy is headed for recession this year.

Bottom line: Only the very intrepid and certain (or foolish) are going to commit to a major new infrastructure project until there’s a lot more clarity.

Take US businesses now paying a 25% tax on imports of steel and other metals, which they must given the current lack of supply inside the tariff walls. For them, trying to estimate future costs is pure speculation. Even the largest and best connected can have the rug suddenly pulled out from under them—as US computer makers did last week when tariffs on Chinese electronics were suddenly reversed.

Count US energy as a another business where caution is king. A decade ago, producers ramped up output of oil and gas as much as fast as they could raise the money. Midstream and downstream companies built new pipelines, processing and storage infrastructure in anticipation of higher volumes to come.

Now shale discipline reigns. A small group of massive, financially powerful producers instead take their cue from price signals. And midstream and downstream companies build only when they have contracts in hand, as well as a firm grip on development costs.

Last week, growing recession fear pushed benchmark West Texas Intermediate Crude oil under $60. That’s a clear sign this isn’t a great time to boost production or build new pipelines. And where there is activity, it’s through partnering, rather than individual companies going it alone.

We’ll know more about US energy companies’ plans when they release Q1 results and update guidance the next few weeks. But the betting here is we see a lot more of what we did a couple months ago. That’s what’s been called “high grading” of projects, cutting costs and maintaining balance sheet strength and dividends.

I expect the much the same from the Canadian companies I track. But there’s a huge exception: The Canadian energy sector increasingly sees itself as a huge beneficiary from US tariff and trade chaos.

Western Canada’s current production and pipeline network is heavily geared to serving US demand. In 2023, over 80% of total Canadian oil supply (97% exports) was shipped to the US. Canada accounted for over 60% of all US oil imports, five times the next largest supplier Mexico. The country also exported roughly 45% of its natural gas supply to the US.

That’s why the initial 25% tariff the Trump Administration levied on Canadian imports—downsized to 10% for energy—was immediately and fiercely opposed by industry on both sides of the border as disruptive and costly. But while further tariff exemptions have been carved out, Canada’s energy sector has largely responded by pivoting to Asia.

In a keynote address to Canadian Club Toronto last week, the CEO of leading midstream company TC Energy (TSX: TRP, NYSE: TRP) challenged Canadian industry and government to “set a bold vision” to become the “number one exporter of LNG to Asia.”

Alberta Premier Danielle Smith recently offered two alternatives to the US. Come to an agreement and we’ll greenlight pipeline infrastructure capable of transporting another 2 million barrels per day to the US for export. That could include reviving the Keystone XL pipeline expansion, with project owner South Bow (TSX: SOBO, NYSE: SOBO) very likely profitably acquired.

The other alternative is don’t deal with us and Canada will ramp up exports to Asia, through the “at least six or seven projects that are emerging.” That sentiment is echoed by Provincial Energy Minister Brian Jean, who says Trump’s tariff threats have already forced Alberta to start “looking at more opportunities to get more barrels off our borders besides the US.”

Aiding a Canadian pivot to Asia are four huge energy projects, three already in service and a third on track for startup in weeks.

The TransMountain Pipeline project has tripled oil shipping capacity on the Alberta-to-British Columbia system. And the first big contract with a Chinese refiner was announced in March. The Coastal GasLink Pipeline is already shipping cheap Montney shale natural gas to the coast.

Altagas Ltd (TSX: ALA, OTC: ATGFF) has for several years been exporting LPG (liquefied petroleum gas) from its Westcoast platform, and continues to expand capacity. And the LNG Canada export facility built by a Shell Plc (NYSE: SHEL) led consortium will ship first cargos this summer.

Those projects are not only ramping up exports but they’re the forerunners of others, including the Cedar LNG facility developed in partnership between Pembina Pipeline (TSX: PPL, NYSE: PBA) and the Haisla nation entering service in 2028. And the long-stalled Northern Gateway pipeline to ship oil from Alberta to the Pacific Coast is also back on the table.

Canadian energy has a huge competitive advantage in far shorter transportation times to Asia. Given the variables of sea travel, it’s tough to get a hard and fast day count. But it appears shipping times for LNG from Vancouver to Tokyo or Shanghai could be as little as half what’s needed to transport from the US Gulf Coast—with no need to pay to navigate the Panama Canal.

That edge is money in the pocket of Canadian energy producers, midstream companies and the shippers that carry the trade—and their investors as well.

And for the first time in quite a while, energy sector political risks are arguably less in Canada than the US—with both leading parties professing support for industry ahead of the country’s April 28th election. Oh Canada!