Don't Be Tempted by the TACO Trade

Politics based strategies not only lose money but they take our attention off the real drivers of investment returns.

Thank you for reading Dividends with Roger Conrad!

Q2 earnings reporting season is getting under way. And thanks to consistent balance sheet strength and pricing power, I’m especially confident the recommended stocks in Dividends Premium and Dividends Premium REITs will continue building wealth.

If you like what you’ve been reading in these posts, you might want to check out the Dividends Premium service with the link attached to this email, or alternatively in the Substack application. My service also includes the Dividends Roundtable investment discussion forum, which I host 24-7 on the Discord application.

Hope everyone is having a happy and profitable summer!—RC

Leave it to Wall Street to come up with a trade based on the premise that President Trump will always back off from an import tax—tariff—that’s a threat to do real damage to the American economy.

But investors should avoid the “Trump always chickens out” or “TACO” trade like the plague. And the same goes for other politics-based investment strategies, especially at a time of American political division when emotions are running high.

Yes, in the now roughly six months he’s been in office, the president has made a dizzying number of trade policy stops and starts. And those who’ve consistently bet that the most aggressive proposals wouldn’t stick have been rewarded, at least so far.

But here are three very good reasons to avoid the so-called TACO trade going forward.

Maybe you’re very confident in your powers as a long-distance mind reader. But for the rest of us, betting on TACO means investing real money on what amounts to little more than a guess about the president’s intentions.

Also, though the president has walked back some proposals, he’s also made some pretty consequential moves. That includes the 50 percent tariff on steel imports. The American Iron and Steel Institute reports that approximately 23 percent of US steel consumption is fed by imports. And not surprisingly, domestic steel producers have raised their prices to take advantage of the rising cost of imports.

About a month ago, TACO traders got excited about a rumor the Trump Administration was nearing a deal to exempt Mexican steel imports from tariffs. So far, however, nothing has happened. And Mexico is only the fourth largest source of imported steel, well behind heavily tariffed exporters Canada, Brazil and South Korea.

Then there’s the 50 percent tariff on imports of copper, a metal essential to construction, electronics manufacturing, transportation and industrial machinery. Despite a large domestic mining sector, more than half of copper used in the US is imported, more than 70% from Chile.

You might believe as I do that Mr. Trump’s tariffs are a terrible idea that hurts Americans first and hardest. And I would argue tariffs have been thoroughly discredited throughout economic history, as accomplishing nothing but making everyone poorer.

But you can’t deny Mr. Trump’s tariffs have teeth—And that’s no TACO. In fact, the June Consumer Price Index showed so clearly that tariffs are boosting inflation that JP Morgan CEO Jamie Dimon publicly defended Federal Reserve Chairman Jerome Powell’s “restraint for longer” policy last week.

Even Administration threats to fire Powell have become fodder for TACO traders lately. Last week, for example, the “news”: the president presented a termination letter for the Fed Chairman to House Republicans triggered a selloff, which was later reversed when he publicly denied it.

Still sound like TACO is something you can consistently place winning bets on?

The second reason for just saying no to TACO is government policies are notorious for impacting investment returns 180 degrees opposite from what the consensus expected.

If you’ve read my posts for a while, you’ve seen me cite the oil and gas sector’s performance of the last 8 years as an example of politics-based investment strategies proving wildly off the mark.

“Drill baby drill” was basically the energy policy of the first Trump Administration. And they pulled out all the stops to make it easier to produce oil and gas in this country, as well as coal. Nonetheless, the fossil fuel industry was the worst performing sector in the S&P 500 from 2017-20. And it was the best performer from 2021-24, when the Biden Administration was aggressively advantaging renewable energy.

President Trump was inaugurated for a second term at noon on January 20 of this year. That day the Energy SPDR ETF—which is comprised of the largest energy stocks with ExxonMobil (NYSE: XOM at 23%--closed at 93.48. It’s now about -8% below that level.

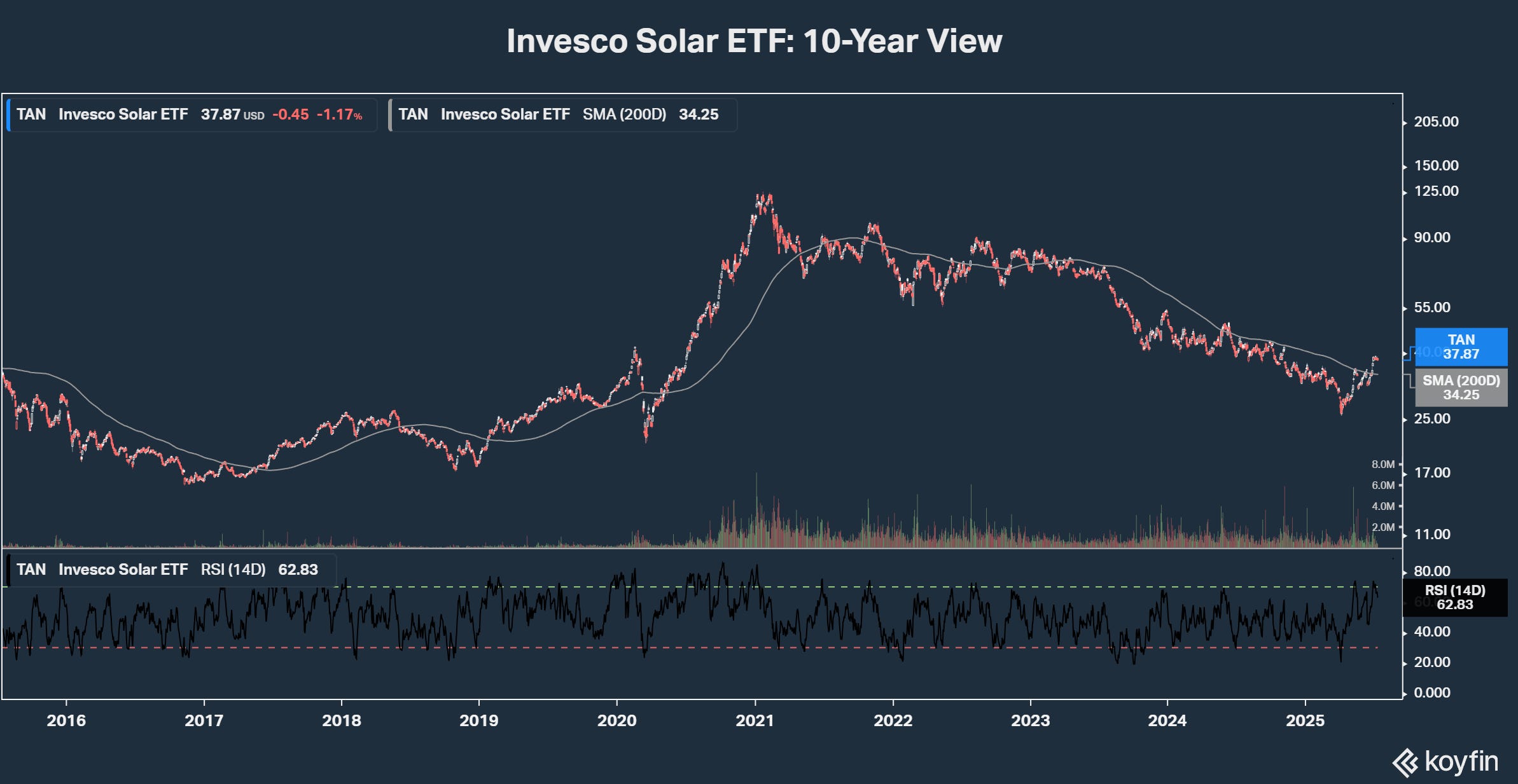

In contrast, the Invesco Solar ETF (TAN) is about 12% higher than where it closed on Trump’s second Inauguration Day. That’s even as the Administration and Congressional Republicans have been every bit as aggressive disadvantaging wind and solar energy as the Biden Administration was advantaging them.

And one more thing: TAN closed January 20, 2021—Biden’s Inauguration Day—at 114.78. On January 17, 2025, the trading day before Trump took office, the ETF finished at just 34.39.

Why have even the most aggressive government policies utterly failed to produce the returns so many investors expected?

The answer is the third major reason why today’s TACO trades are likely to end in tears for so many. Mainly, no matter how loudly the popular investment media proclaims otherwise, there are far more important factors impacting stock and bond market returns than politics.

In fact, the more attention investors pay to politics when making decisions, the more likely they are to miss what is truly important.

Back in 2017, for example, the oil and gas industry was in the middle of a multi-year down cycle, the result of too much supply chasing too little demand. But the bottom was in by mid-2020 and by 2021 the up cycle began.

Renewable energy was a top-performing sector during the first Trump Administration. That’s because plunging component costs and rapidly shrinking deployment times made wind and solar an increasingly attractive source of megawatts, for utilities especially. But the excitement also created an investment bubble. And despite supportive Biden administration policies, it basically deflated for four years.

The energy cycle--the long-term balance between supply and demand—is the primary driver of investor returns in oil and gas stocks, period. Despite pausing in first half 2025, we expect the uptrend to resume because long-term supply is still lagging demand, not because of politics.

The Great Rotation from Big Tech to quality stocks across other sectors is another mega trend shaping investment returns with no link to politics.

Not since 2000 has the S&P 500 been so heavily weighted toward such a small group of extremely expensive stocks. Led by NVIDIA Corp (NSDQ: NVDA) at 7.87% and trading at an extremely expensive 55 times earnings, the Big 8 Tech companies are now an unprecedented 35.6% of the index, and therefore a similar percentage of the tens of trillions of “passively managed” funds that now outnumber all actively managed money.

NVIDIA alone has three times the S&P 500 weighting of the entire oil and gas sector as well as global pharmaceuticals and utilities. And those sectors collectively far outweigh the AI processor producer in terms of economic impact, including revenue, taxes paid and people employed.

Maybe this time is different. But every time the stock market has become so concentrated in a few names in the past, it’s eventually rebalanced, sometimes quite painfully. That was the case in 2000-02, commonly referred to as the “Tech Wreck.” So far, the market has avoided such a cataclysm. And after NVIDIA’s surge last week, the Nasdaq 100 hit a new all-time high.

Less noticed is the fact that over the past 12 months, money has been flowing gradually into other sectors, which as a result have outperformed Big Tech. Whether the leaders muddle along or crash, that trend has a long way to run, given how out of balance the S&P 500 is. But it has zero to do with politics.