Energy Crisis: Nuclear Power Has Answers

3 ways to bet on it.

Editor’s note: Happy Easter for those celebrating today. This weekend, I’m presenting at MoneyShow’s Investment Masters Symposium in Hollywood Florida, along with my friend and fellow Substacker Elliott Gue. Thanks for reading Dividends Roundtable!--RC

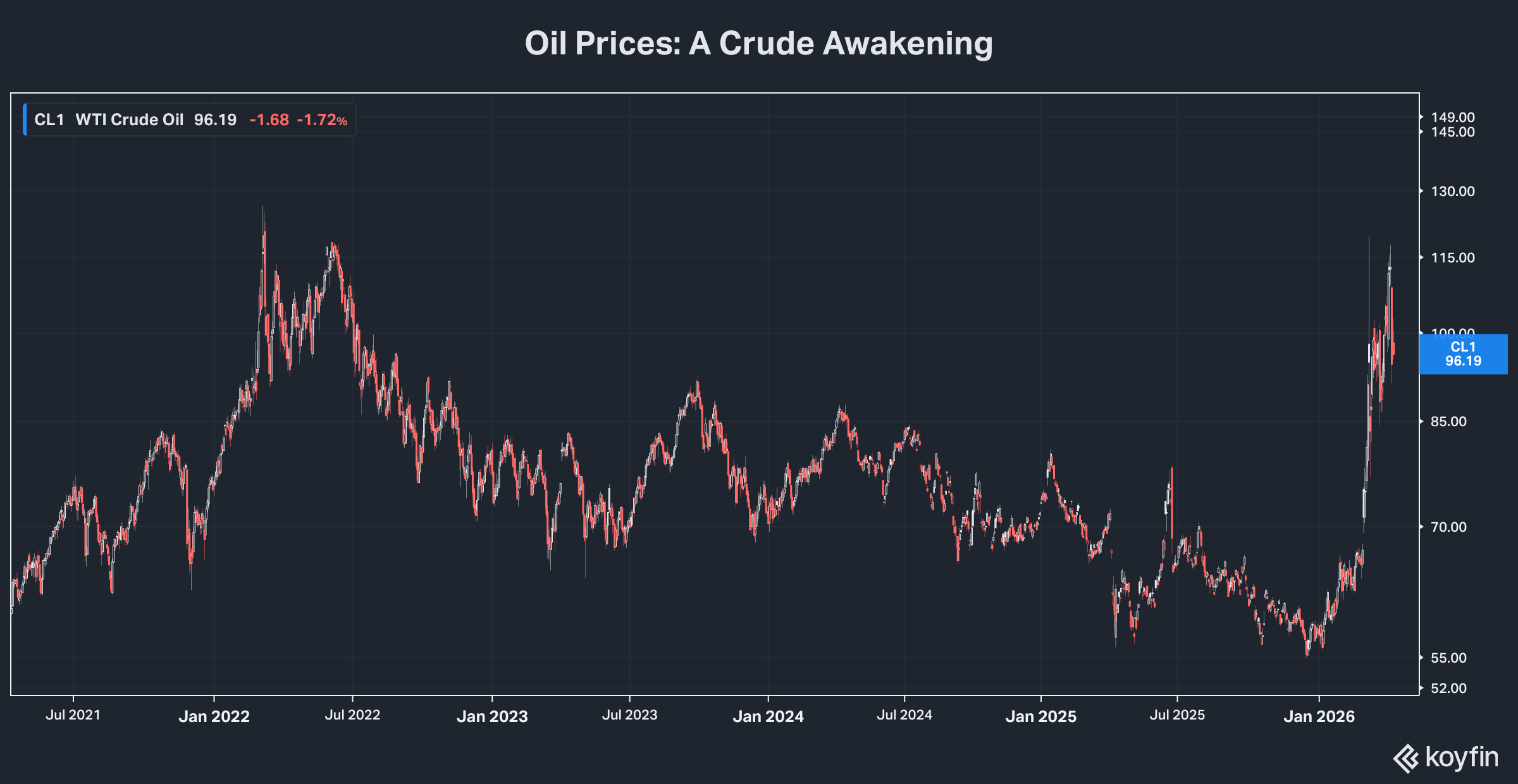

Has Operation Epic Fury entered a de-escalation phase? Are oil prices headed back to the $75 range, where the forward curve is now?

Those questions are understandably front and center in investors’ minds. But we’re going to be better off not trying to answer them and instead focusing on what’s going to benefit regardless of events in the Middle East. And that means nuclear power.

First, let’s look at where we stand now. This is an age of spin maestros. And what used to be viewed as dry economic data is now fodder for political diatribes. But there’s no sugar coating the fact inflation spiked in March to a sequential rate of 0.9%, largely because of a jump in gasoline prices to over $4 a gallon nationally.

So-called “core” inflation was considerably lower at 0.2%, by “virtue” of excluding food and energy. But it’s fair to say the Federal Reserve is now putting further monetary easing on hold, as it waits to see what the impact of a potential energy price shock will have on the broad economy. And that’s kept companies’ borrowing costs higher for longer, even though the Fed Chairman recently declared there was “zero” job creation in the private sector.

All things considered, the US stock market is proving resilient so far. S&P 500 ETFs, the bedrock of most Americans’ portfolios, have been up and down all year but are currently sitting at about breakeven. And despite concerns about inflation and interest rates, the top-quality dividend stocks I recommend in Dividends Roundtable are market leaders.

The SPDR S&P 500 ETF is still slightly underwater even after last week’s rally. But the iShares Select Dividend ETF (DVY) is up 8.83% year-to-date, after bouncing back from a late March low point. The Utilities SPDR ETF (XLU) is ahead 10.8%, also following a late month recovery. And even real estate investment trusts are showing signs of life, with the Real Estate SPDR ETF (XLRE) ahead about 6.8% for the year.

The Dividends Premium Portfolio is up solidly over the past week and is ahead 15.2% for 2026 so far. That’s adding onto one of the best performances for the first three months of the year since the portfolio’s inception back in 2018.

I expect dividend stocks to continue outperforming in coming months. For one thing, they remain historically under owned. Just 7 Big Tech stocks continue to make up more than 35% of the S&P 500 ETFs that dominate Americans’ portfolios. And whole sectors like utilities and REITs remain a low single digit percentage of that index.

We’ve just lived through a period of market history where—like the late 1990s—investors have prized promises of future growth. Dividends in contrast have largely been an afterthought if they’ve been a consideration at all.

Now the shift is on. But it’s going to take months if not years to restore any semblance of balance to the S&P 500. And since more money is invested passively in US stocks through ETFs than actively managed, that means dividend stocks are going to be catching up for a long time to come.

Historically, few if any stocks emerge from a real bear market wholly unscathed. In 2007-09, for example, utility stocks held up well until the collapse of Lehman Brothers in September. That was the event that turned a year-and-a-half long retreat into a full-scale market rout.

Best in class utilities kept paying dividends even as the banks failed. But the stocks took a huge hit. And it took a couple years after the March 2009 bottom for the group to fully recover what it lost over a roughly six-month period.

Buy and hold after the selloff began was the right call. But taking a little money off the table in summer 2008--when sector stock prices were still rising in a falling stock market—was also a great idea. Gains have nasty habit of disappearing if you aren’t willing to sell a little from time to time.

Now is such a time for harvesting some gains. And we’ve done so in the Dividends Premium portfolio this year on more than one occasion.

But there are also still opportunities for buying good stocks on the cheap. And one area to look is nuclear power.

There’s no doubt how Operation Epic Fury comes out will have a major near-term impact on the stock market. And the bets are lining up on one side or the other.

I think it’s likely import-dependent China will eventually convince Iran to open the Strait of Hormuz and get the oil and LNG flowing the Asia again. But before that happens there could still be considerably more destruction from bombing, drone attacks and sub-sea mines.

And here’s more food for thought. When oil prices spiked in mid-2008, it was the last straw for a US economy that was already teetering on a debt crisis. Inflation adjusted oil prices are still well below the $150 a barrel reached then. But is there a similar pain point this time around?

Going Nuclear, Again

Bottom line, there are many unknowns in the current environment that can and will affect your portfolio the rest of 2026. But as important as these questions are, it’s largely a waste of our time trying to guess how the macro picture may change in the next few months as the result of Operation Epic Fury fallout. Instead, we’re going to be best off focusing on what’s likely to keep making money, no matter how this comes out.

Nuclear power is one of those themes. When Qatar declared force majeure on LNG contracts last month, it set off a mad scramble of buyers in Europe and Asia to replace the supply.

Qatar and other producers and exporters of oil and gas had no choice but to declare contracts unfillable with the Strait of Hormuz effectively shut. Damage from Operation Epic Fury fallout will continue hobble their ability to sell energy even after the bombs stop falling, the drone attacks stop and shipping resumes. And perhaps worst of all, the region has suffered reputational damage to go with the physical destruction. Can an Asian or European buyer really count on Persian Gulf energy to flow?

One group of beneficiaries of Qatar’s challenges are energy producers and midstream companies in the US and Canada. After Epic Fury, North American energy has earned a safety premium, for no other reason than it’s produced and shipped from a region far from the Middle East. And as safe suppliers, companies up and down the energy value chain are going to get a multi-year boost, signing on contracts as soon as they can fill them.

Nuclear power is another option global energy importers are likely to turn to. Facilities take years to build even in countries with supply chains to execute on construction like China. But once built, they not only replace the imported natural gas needed to generate electricity. They provide the power at scale to enable electrification of industry and transportation, further reducing import needs.

There are challenges. The accident at the Fukushima Daiichi facility in Japan arguably did more reputational damage to the nuclear power sector than Chernobyl in a previous decade.

On February 9, Japan finally restarted one of the nuclear power plants shut since the accident, unit 6 of the Kashiwazaki-Kariwa facility. But the rest of the fleet is still shuttered, despite the energy crisis triggered by Qatar’s force majeure.

I expect more Japanese nuclear plants to reopen the next few years. Germany’s, however, remain closed. And there’s little sign anyone is interested in reopening them, despite soaring energy prices that have already undermined the country’s industrial base.

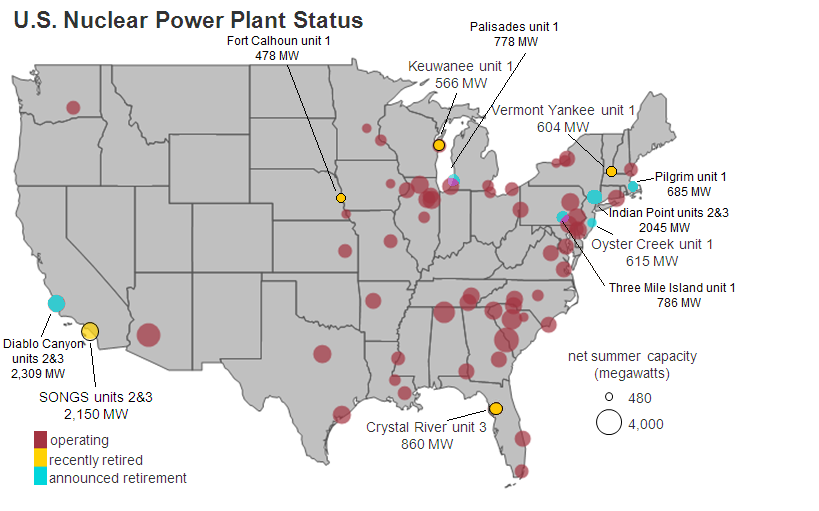

In America, political fallout the Three Mile Island accident in 1979 did not escalate to the point where nuclear plants were shuttered around the country. That was in part thanks to then President Jimmy Carter being a nuclear engineer and resisting pressure for such drastic action.

But the price to the industry was dramatically stepped up regulation that pushed up costs and extended construction times to the point where it undermined economics of plants then under construction. And the resulting writeoffs, dividend cuts and bankruptcies basically ended what had been a building boom.

Ownership of US nuclear power plants consolidated dramatically in the 1990s, as deregulation in 15 states forced regulated utilities to divest ownership. The chief aggregator was Exelon Corp (NYSE: EXC), which earlier this decade spun off the operation as Constellation Energy (NYSE: CEG).

Scale economics enabled US operators to apply lessons from one reactor to others. The result was dramatically shortened outage times for refueling and maintenance. And annual operating rates at US reactors rose from the 60-70% range to 90-95% and higher.

Despite these greatly improved economics, however, no US company ventured to build a new reactor until the 00s. At that point, a half dozen large utilities submitted plans with state regulators to build reactors based on Toshiba Westinghouse’s AP-1000 model.

The new reactors relied on a self-cooling technology eliminating the risk of a Chernobyl style meltdown. And Westinghouse was so confident in its ability to execute on construction it signed fixed price contracts with two companies: Southern Company (NYSE: SO) to build two new reactors at the Vogtle site in Georgia, and the former SCANA to build two reactors at the Summer site in South Carolina.

The projects were enthusiastically embraced by regulators in both states. And as a further inducement, the utilities were allowed to recover costs in customer rates as incurred, rather than ask for one major boost when the reactors came online.

As it turned out, that proved to be the utilities’ saving grace. The self-cooling feature of the AP-1000s meant there was no possibility of a Fukushima-style accident, where the combination of an earthquake and tsunami prevented the facility from pumping in water at the crucial moment. But in the fearful days following the accident, plans were shelved anyway, as would-be builders rightly feared political pressure would still push up costs and condemn their stocks to perpetual underperformance until these decade-plus projects were finished.

They weren’t wrong. Southern and SCANA pushed ahead. But after a few years, it was clear Westinghouse could not fulfill its contracts. And shortly after that company filed bankruptcy, SCANA cancelled the Summer project. Only Southern kept going. And after absorbing billions of dollars in additional costs, it finally brought Vogtle reactors 3 and 4 on stream in July 2023 and April 2024, respectively.

Vogtle is now a key contributor to Southern’s power mix. And the stock has been restored to its historical premium valuation as a best in class utility. But following the plant’s entering service, the utility’s executives left little doubt they were not considering another nuclear project, instead emphasizing a strategy of building natural gas, solar and storage to meet the Southeast’s surging electricity demand.

Then last year, two unknowns trounced two veterans in statewide elections for the Georgia Public Service Commission. The key issue in the campaign was affordability, with the challengers blaming increased utility rates on the Vogtle project.

Republicans retained their 3-2 majority on the PSC. And the final rate cases regarding Vogtle are now well in the rear-view mirror for Southern. But the project remains a cautionary tale for utilities, regulators and investors alike.

So where does nuclear power stand in the US now and how should we invest in it?