Forget SpaceX, Buy Big Telecom

America's Big 3 are rolling and no one's paying attention.

Dragon 2 hover test. Space X Photos.

Editor’s note: Thank you for reading Dividends Roundtable! This week’s edition as always includes an update of my Dividends Premium portfolio, with an average gain of 18% year to date. Premium subscribers are cordially invited to check out the webchats I host 24-7 on the Substack and Discord applications. Here’s to your wealth!—RC

For all too many investors, the coming week will be simply a countdown to the main event: The initial public offering of Elon Musk’s SpaceX.

The hype is already flowing fast. Expect it to gain intensity as the big day arrives.

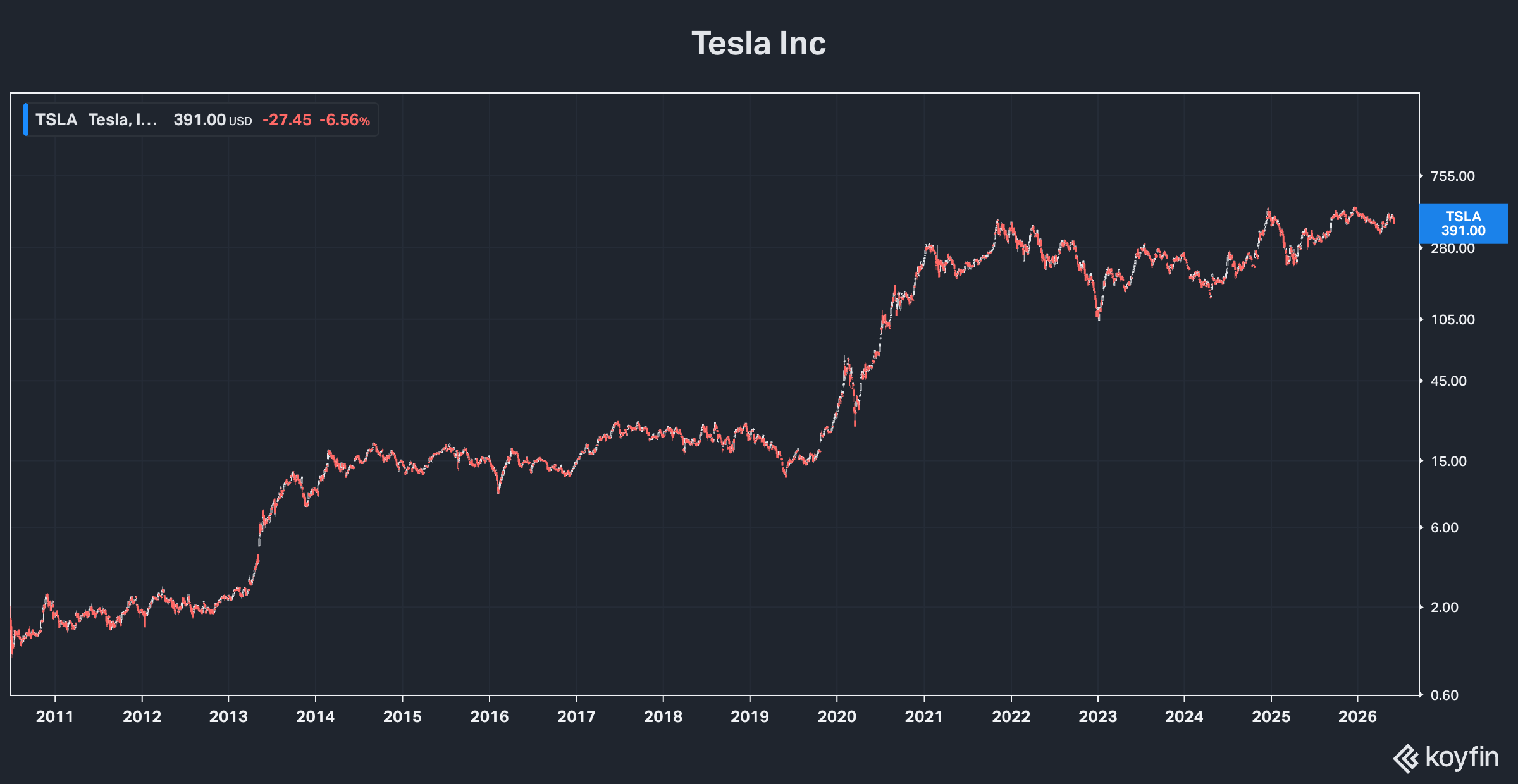

The enigmatic CEO of EV manufacturer Tesla Inc (NSDQ: TSLA) and social media forum X has reportedly bypassed Wall Street’s usual process for setting IPO prices. And that move has apparently convinced more than a few large institutions to stand aside.

Instead, Mr. Musk appears to be counting on his panache with retail investors to raise a target $75 billion, which would imply an astronomical total market value of $1.75 trillion for the company.

SpaceX has made the news regularly in recent years with its exploits in outer space, though some were less than successful. And it made another huge splash acquiring wireless spectrum from Echostar (NSDQ: SATS), which the Federal Communications Commission signed off on last month.

SpaceX appears to be a long way from real earnings, posting a $4.4 billion loss in 2025 and losing almost that much in Q1. And at $1.75 trillion, the stock would be selling at 100 times annual sales, an extreme initial valuation that in the past has ensured a sizeable post-IPO drop.

All that may not make any difference for what happens Friday. For one thing, Musk always thinks big, at least in public. And announced plans to literally build a space fleet have obviously captured many investors’ imaginations.

It’s undeniable that Tesla made electric vehicles cool, though it’s Chinese companies like BYD that now dominate the market. Love it or hate it, X is arguably a more dynamic forum for sharing opinion than ever. And though Musk’s rooftop solar company SolarCity never panned out, his forecasts of solar’s growth have if anything proven to be too conservative.

The International Energy Agency estimates global installed photovoltaic (PV) capacity rose from around 759 gigawatts in late 2020 to nearly 2,400 GW by the end of 2025. And the pace of new installs has picked up every year, from 130 GW in 2020 to 800 GW last year with even more expected in 2026.

The levelized cost of electricity (LCOE) for utility scale solar has dropped to just 4.3 cents per kilowatt hour, making it cheaper than any other universally deployable energy source. A flood of new production capacity has driven down solar module prices by 50%, while increasing panel efficiency from 19-20% to 22-24% over the last five years. And the cost of solar-plus-battery storage systems—which Tesla does sell—has dropped by as much as -45%.

That didn’t prevent Tesla’s energy, generation and storage revenue from dropping by -11.8% in Q1, as competitors in that business did even better. But lower costs did improve margins greatly: The company’s Q1 cost of energy storage revenue dropped to 60.5%, down from 71.2% a year. And it’s likely headed even lower this year.

As for Tesla overall, the company like all EV manufacturers was counted out by many when the President Trump’s OB3 fast tracked elimination of federal tax credits. But even as US behemoths like Ford Motor (NYSE: F) predictably tacked and wrote off billions, Tesla’s Q1 revenue increased by 15.8%, while income from operations surged 135.8%. And that’s in a year when sales from regulatory credits—basically a pass through to earnings—plunged by -36.1% to just 8.1% of gross profit, versus 18.9% a year ago.

Bottom line: Over the past 5 to 10 years, Tesla has gone from hype machine to an enterprise with real sales and earnings. And with sales of China-made EVs rising 39.4% in May—in part a global response to spiking gasoline prices with the Strait of Hormuz still shut—the company looks like it’s here to stay.

Great Company, Un-Investable Stock

Of course, whether Tesla is an investable stock for long-term wealth building is a totally different question. Anyone who bought it in the previous decade is up huge. But the stock is down about -13% year-to-date and has made no real headway the past couple years.

Tesla is also the eighth most heavily weighted stock in the S&P 500 at nearly 2%, meaning it’s very much tied to the stratospheric expectations of the artificial intelligence theme—a fact further confirmed by sky-high valuation of 180X “normalized” earnings.

The bigger they come, the harder they fall. And for anyone tempted to chase the SpaceX IPO this week, that’s food for thought.

I don’t share the view that SpaceX isn’t a real business. And the company also has multiple friends in high places, who for one reason or another seem to be pulling out all the stops for a successful launch.

Last week, for example, the company won tax incentives for its chip manufacturing project in Texas. FCC Chairman Brendan Carr last month reflected the pro-Musk sentiment in the Trump Administration with this extraordinary admonition to opponents of Echostar’s sale of wireless spectrum to SpaceX:

“I would be very hesitant betting against Elon Musk. A lot of people have tried to do so and have lost a lot of money along the way.” He also went on to opine “To see this level of investment by SpaceX/Starlink in spectrum I think speaks to the amount of diligence they’ve done and the confidence that they have either in direct-to-cell or whatever innovative use cases they may have.”

That’s an extraordinary endorsement of a company Mr. Carr is regulating. And while there’s “no public evidence” the Chairman has a financial stake in SpaceX ahead of the IPO, Trump Administration officials do have at least $44 million in the company and its AI affiliate xAI.

Does that mean the fix is in? Maybe, maybe not.

One other IPO fact is that Mr. Musk will still own 82.4% of the combined company after the IPO. That should mean his interests are conjoined with the minority shareholders. But that level of ownership also means SpaceX can be classified as a “controlled company,” with everyone else the equivalent of a limited partner as far as decision making and access to information.

None this will likely matter to Musk fans, who are already convinced he’s their ticket to riches. And maybe they’ll be proven right. But in my view, post-IPO SpaceX is basically in the same category as Tesla—an interesting company with a stock that trades purely on momentum fueled by investor sentiment.

Buyers on Friday may make money if they’re nimble. Those privileged to get in before the IPO—like those Trump Administration insiders—have a better shot at getting their beaks wet. And Mr. Musk will clean up, almost no matter what happens.

There will be at least two potential major market moving events before the IPO. That’s Wednesday’s release of Consumer Price Index data for May, followed by the Producer Price Index on Thursday.

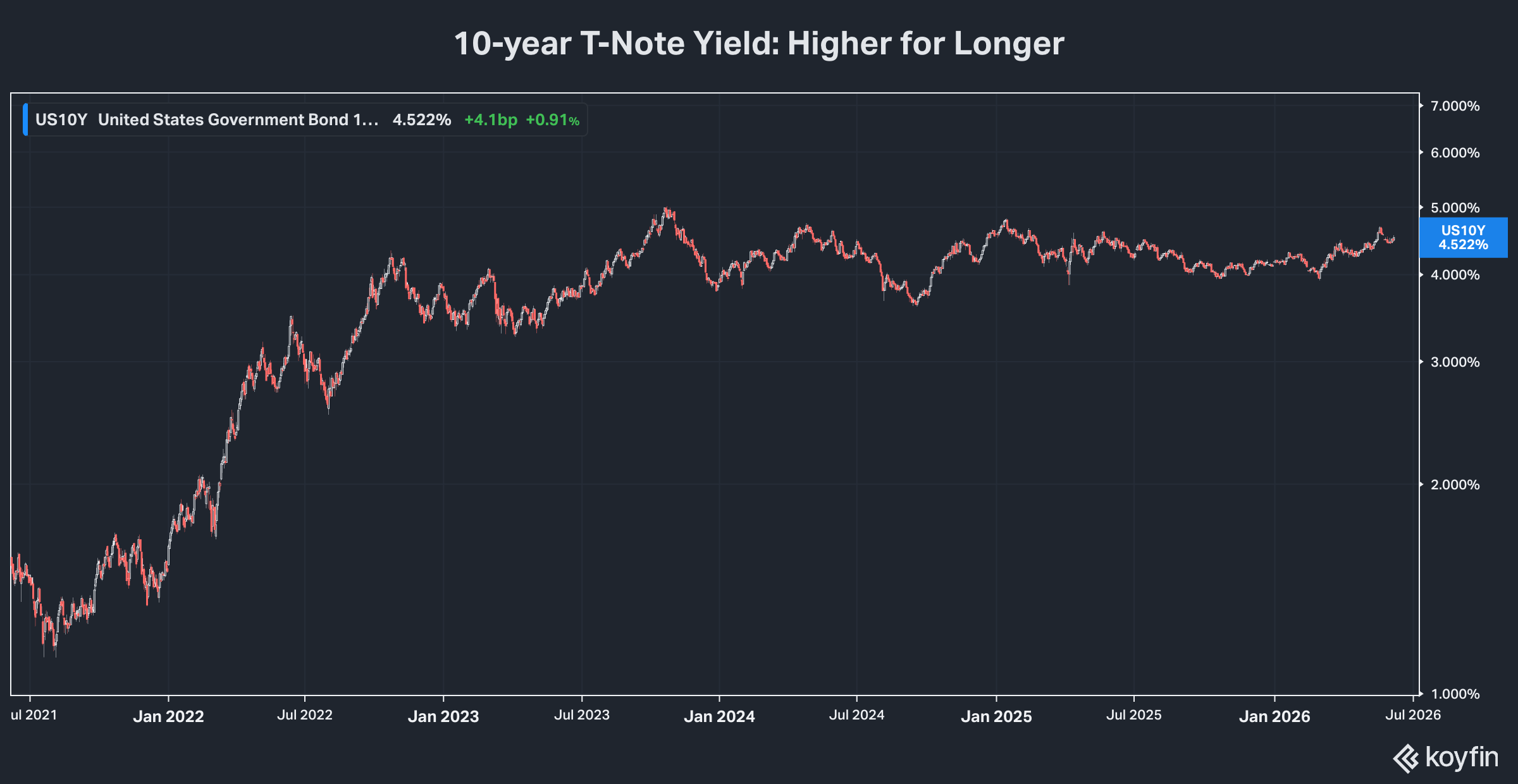

On Friday, a sliding bond market pulled the Big Tech leaders lower, following a solid employment report that seemed to portend more inflation. Another round of CPI and PPI numbers like what we saw for April will only further stir those worries. And by extension it will boost bets that—new Fed Chairman or no—the central bank’s next move will be to raise rather than lower the Fed Funds rate.

Anything too dramatic could theoretically weigh on the SpaceX IPO. It seems unlikely Musk will cut the price from the planned $135 per share. But the price of publicly traded shares may sell off in a hurry after the IPO. Buyer be wary!

These Stocks Held Their Own

Concerns about rising inflation and interest rates did fall hard on some dividend paying stocks as well. But damage was hardly universal.

In fact, 17 of the 20 real estate investments trusts on my Dividends Roundtable First Rate REITs list posted gains on Friday, two of them close to 4%! So were more than half the utilities and essential services stocks I’ve tracked the past four decades. And so were half the Dividends Premium Portfolio positions.

Another group in the green on a day when the S&P 500 and Nasdaq 100 were shedding -2.6% and almost 5% of their value, respectively: The Big US 3 Telecom stocks.

This group has been a mixed bag this year. And a good portion of blame can be laid at the feet of SpaceX hype, as expressed in FCC Chairman Carr’s extraordinary tacit endorsement of the upcoming IPO.

As rumor had it, Echostar CEO Charlie Ergen last summer called in a favor from the White House. And the FCC dropped its threat to seize company wireless spectrum for violating investment pledges. The former DISH Network had made those pledges during the first Trump Administration, as a condition for buying spectrum assets from T-Mobile (NSDQ: TMUS) when it merged with Sprint. Dropping the investigation allowed Ergen to sell the valuable spectrum to AT&T Inc (NYSE: T) and SpaceX.

Echostar had long been an ineffective fourth national wireless competitor. But as I wrote in the September issue of Conrad’s Utility Investor, the spectrum sale officially launched a “Big 3” world for US communications, with three rather than four national wireless networks.

That’s been China’s model for more than a decade. The result has been consistent industry margins and robust investment—with the result the country is now a global leader in network quality and innovation including artificial intelligence.

That same positive trend has been unfolding in the US over the past year. And the sector has continued to consolidate, even as Big 3 earnings are the best they’ve been this decade.

Big 3 stocks, however, haven’t felt the love. And one big reason seems to be a persistent belief that SpaceX intends to crater industry margins once again by launching a fourth national wireless network.

Perhaps following on FCC Chairman Carr’s statement about a “direct to cell” business for SpaceX, an Oppenheimer analyst last week forecast “competitive risks from low Earth orbit satellite providers” could “pressure broadband and mobile growth” at the Big 3.

Maybe. But the record of satellite technology going head-to-head with 5G wireless and fiber broadband networks is quite dismal indeed.

Take Echostar, currently the largest player in the space. The company lost another 366,000 of its satellite-based pay television users in Q1. It also shed 58,000 broadband users (7.8% of its base), or nearly twice the number of losses in the year ago quarter. Broadband and satellite service revenue dropped -11.1% from Q1 2025. And earlier this month, the company was forced to delay interest payments on three bond issues.

The company has a 30-day grace period to pay. And by then, it should have closed FCC-approved sales of spectrum for $20.25 billion of proceeds. But Echostar’s operating performance is a clear reminder that satellite technology does not measure up currently to the 5G wireless and fiber broadband networks the Big 3 offer. And now that the Big 3 have formed a joint venture to eliminate wireless broadband “dead zones” in the US, competitive pressures will only increase.

Could SpaceX offer something better to undercut the Big 3? I never say never when it comes to technological possibility, particularly if there’s money, vision and determination behind it. But the Big 3 are also furiously innovating to provide faster, more reliable connections at a lower cost. And they’re increasingly leveraging to the same artificial intelligence tech SpaceX would use.

Pre-SpaceX has pursued partnerships with the Big 3 that build on each other’s expertise for mutual benefit. In my view, there’s every reason to expect post-IPO SpaceX will continue doing the same—rather than make a hugely expensive, highly speculative effort to compete in a business in which it has no experience.

In fact, by offering service and bringing the number of US wireless competitors back to four—as is the case in Canada—Mr. Musk would be undermining the very sector margins that would make SpaceX’ entry profitable. Better to partner with the Big 3 to grab a share of future business than compete for share in a largely mature market.

At the end of the day, only actions and Big 3 earnings growth will disprove the SpaceX as a communications sector disruptor thesis. But in the meantime, we have a golden opportunity to pick up shares of the three companies that are rapidly increasing dominance of their industry and paying a rising stream of dividends as they do.

The cheapest of the three: