Hey WSJ: Where’s Your Utility Wildfire Armageddon Story?

Could it be sliding down the memory hole along with last’s year’s debunked sensationalism about telecom lead cables?

It’s been roughly two months since Berkshire Hathaway’s (NYSE: BRK/B) legendary Chairman Warren Buffett released his annual letter to shareholders. And speaking as a shareholder, the news was quite good: 27.9 percent higher Q4 operating earnings, with balance sheet cash and equivalents reaching almost $600 billion.

Nonetheless, Mr. Buffett focused on a handful of negatives: Broad statements to the effect shareholders shouldn’t expect more “eye-popping” investment gains, a greater than expected decline in railroad earnings due to “wage increases promulgated in Washington,” and what the Chairman called a “severe earnings disappointment” at Berkshire Hathaway Energy.

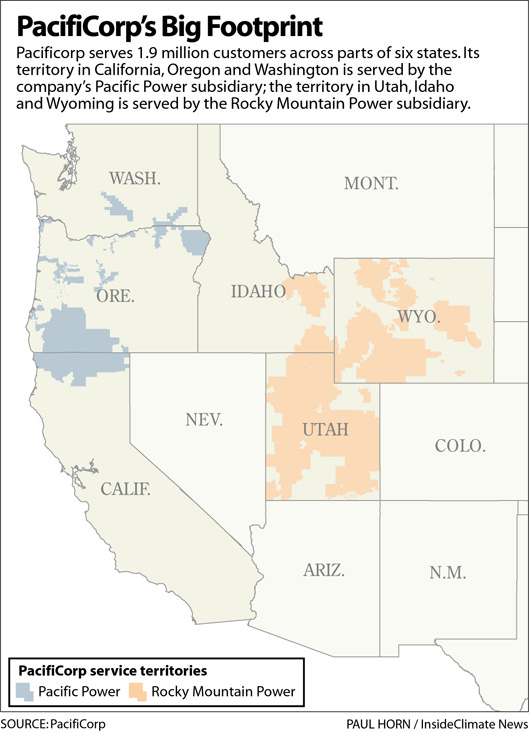

As I highlighted in my March 3 Substack “Warren Buffett’s Wrong,” Buffett’s main beef with the utility and pipeline business wasn’t operating performance. It was the ruling by an Oregon court awarding $5 million in damages to 17 victims of wildfires allegedly involving power lines owned and operated by Berkshire’s PacifiCorp unit.

The decision potentially opens the utility to as much as $11 billion of related claims from a much larger pool of plaintiffs. And Buffett responded by tacitly threatening to stop investing in states where PacifiCorp was at risk to paying large wildfire awards.

In my Substack article, I stated investors could “read Buffett’s letter as a warning to regulators/politicians to get moving on the issue.” And barely six weeks later, PacifiCorp’s most important state has apparently listened.

Utah SB 224 establishes a “self-insurance” plan for the state’s utilities—mainly Berkshire’s PacifiCorp—that will be funded entirely with a surcharge in utility rates. The residential monthly cap of $3.70 per customer is unlikely to provoke much opposition. And it will be eliminated when the fund reaches $1 billion in assets.

Further, the “prudence” of using the Utah Fire Fund to pay claims can’t be challenged in court. Regulators could order replenishment of “imprudent” amounts up to 10 percent of a utility’s rate base. But even that worst-case scenario wouldn’t come anywhere close to threatening PacifiCorp’s financial health. Claims against PG&E Corp (NYSE: PCG) for the 2018 Camp Fire, for example, were at one time several times its California ratebase..

And it’s extremely unlikely PacifiCorp/Berkshire would ever face a significant prudence review, barring grave misconduct. Utah SB 224 also caps damages for parties with physical injury and no economic claim at $450,000. Damages for parties with no physical injury or economic claim are capped at $100,000.

So score one for Berkshire at a time when weather changes have made wildfires quantitatively a much higher risk in many western states than they’ve been historically. And it’s equally clear thousands of miles of power lines and related infrastructure in multiple states need substantial grid-hardening investment.

The Edison Electric Institute—the principal US power industry trade group—is spearheading four initiatives to reduce risk: (1) Direct mitigation actions and implementation of new technologies such as data science, drones and artificial intelligence to identify potential troubles spots before they become deadly wildfires and further improve industry best practices, (2) Partnerships with customers and governments to accelerate and magnify the impact of actions taken, (3) Structuring insurance, credit and financial risk transfer to boost companies’ ability to handle the cost of wildfire claims and preventative actions and (4) Enlisting federal and state authorities to ensure utilities stay healthy enough to make needed investments.

In my view, state action to cut utilities’ risk and encourage needed investment is the most critical of the four. And the “Beehive State” has provided other states a template for how to make that happen.

The utility most on the hot seat for wildfire damages right now is still Xcel Energy (NYSE: XEL), which faces litigation over wildfire damages in Colorado and Texas.

Earlier this month, Colorado Governor Jared Polis ordered state regulators to study measures to “protect customers” when the utility shuts off power when wildfire risk is extreme. That follows understandably negative customer reaction to shutoffs amid “hurricane force winds.” Xcel equipment has been blamed for allegedly helping ignite the December 2021 Marshall Fire in Boulder County, as well as Texas’ Smokehouse Fire this year.

Together, Colorado and Texas contribute more than 50 percent of Xcel’s total rate base. And estimates put potential liability exposure “in the billions of dollars.”

The Wall Street consensus is Xcel will settle these cases with plaintiffs, probably in the 2026 timeframe. And the stock now reflects the risk, selling for about one-third less what it did before the Marshall Fire. But at the end of the day, Colorado and Texas need to keep Xcel healthy, if for no other reason than the utility is key to making needed grid investments.

Earlier this month, the Texas House of Representative held three days of hearings focused on the state’s 4,000 plus wildfires since late 2020. The committee’s report is expected around May 1. But despite angry testimony from witnesses, legislators appeared mainly focused on regulatory changes.

If there was a corporate scapegoat, it was Georgia firm Osmose Utilities Services, the company Xcel hired to perform safety inspections. And only a week after the hearings ended, Texas regulators approved Xcel’s rate settlement without modifications with a solid return on equity of 9.55 percent.

There’s no guarantee the Texas legislature will propose steps to mitigate utilities’ wildfire liability risk. And in fact this week a cattle rancher filed a multi-billion dollar class action suit against Xcel and Osmose in the US District Court for the Northern Division of Texas—a possible effort to avoid a potential legislated liability cap.

But unless you’re in the business of publishing sensationalist pieces to get investors’ attention by scaring them, it’s clear the aftermath of the Texas and Colorado wildfires isn’t following the playbook of the California’s 2018 Camp Fire that temporarily ran PG&E Corp (NYSE: PCG) into bankruptcy.

Simply, no one but a handful of trial lawyers wants a utility bankruptcy to derail needed investment to reduce the risk of future wildfires. And that goes for Hawaii as well, site of last year’s deadly Maui wildfire

Last week, the State Attorney General released a 376-page report that largely affirmed Hawaiian Electric’s (NYSE: HE) previous statements and declined to name the utility as the cause. The AG’s office has said that later this year it will release a report on the effectiveness of Maui’s fire protection systems and another on recommendations for the future.

The US Bureau of Alcohol, Tobacco, Firearms and Explosives has a separate ongoing investigation into the wildfire’s causes. And the US House Energy and Commerce Committee recently sent a letter to the company alleging “questions persist” about its wildfire mitigation plan, part of an apparent effort to discredit Hawaii’s renewable energy goals.

No doubt the small army of trial lawyers now traipsing Maui in search of plaintiffs will make as much as possible of whatever comes of this. But Hawaii is co-funding a $150 million relief fund to wildfire victims who don’t sue. So it’s obvious the state wants to keep the utility whole as the best and only way to prevent future wildfires.

Bottom line: Wildfires are a deadly and growing danger, particularly in western states. But united by common interest, stakeholders are working together as never before.

That’s a 180-degree attitude shift from the constant confrontation of the previous decade, which led to the PG&E bankruptcy. And it adds up to an opportunity for investors to buy good utility stocks cheap—provided they’re willing to draw their own conclusions, rather than simply take mainstream media sources like WSJ at their word.