How to Beat Inflation

I'm making income investors' enemy my friend.

Editor’s note: Thank you for reading Dividends Roundtable! This week, I’m premiering a slightly different format for my Sunday posts, featuring actionable investment advice for Dividends Premium members. I’ve also launched a 24-7 Dividends Roundtable chat room on Substack, which allows members to start their own threads. Here’s the link:

I hope you find the new features useful. Here’s to your wealth—and an early Spring!—RC

Inflation is the silent killer of all income portfolios—relentlessly chipping away at principal and purchasing power.

Some years, the damage the swift and devastating. In others, it’s less noticeable. But even at the sub-2% inflation rate targeted by the Federal Reserve, a “safe” portfolio of cash and fixed income will steadily erode.

That’s an inconvenient truth for the universe of “Target Date” funds that dominate most corporate-sponsored retirement accounts. Each fund has a designated “Target” date, by which time it’s supposed to have achieved the investor’s target return to be ready for retirement.

It’s allocation by calendar. As target dates approach, funds automatically allocate a greater percentage of assets to fixed income ETFs. That’s supposed to lock in value against stock market volatility. But it also increases exposure to inflation. And if interest rates and inflation happen to be rising around the target date, investors may find considerably less money in their account than they were expecting.

Just ask anyone who cashed out a Target Date fund following the Federal Reserve’s tightening of monetary policy in 2022-23. That first year wasn’t great for the S&P 500 and related ETFs either. But the stock portion of Target Date funds did recover in 2023, while bond values continued to erode.

So much for safety! But Target Date funds remain the staple of the passive investing options that are many retirement plans’ only choice. Another boondoggle is only a matter of time.

S&P 500 index-related ETFs dominate the stock portion of Target funds. And right now, the State Street S&P 500 SPDR ETF (SPY) has 35.8% of its assets in just 7 very expensive Big Tech stocks—all riding momentum from the single theme of artificial intelligence investment.

I’m a believer in the possibilities of AI, just as I was in information technology a quarter century ago. But the lesson of 1999-02—when the Nasdaq doubled and then cratered in the Tech Wreck of 2000-02—is the stock prices during a boom will outrun companies’ actual growth by years. And when the market inevitably rebalances, it can for the underweighted new leaders’ gains to offset the former leaders’ slide.

Fortunately, investors can avoid the damage from creeping inflation and the risk of a meltdown in the heretofore Magnificent 7 Big Tech stocks.

The first step is to take control of your investments. If your portfolio is a corporate sponsored retirement plan, find out what your options are. An “unweighted” S&P 500 ETF, for example, would not suffer nearly as much damage from a new Tech Wreck as a weighted ETF.

If you already have control, you have considerably more options. And for the record, I have nothing against bonds. But if you want to avoid the scourge of inflation, you’re going to have to manage what you own, just as you would stocks.

My colleague Elliott Gue does precisely that in his “Smart Bonds” advisory, which he also publishes on Substack. And he does it with ETFs, so his members never have a problem buying and selling on his signals.

Beating Inflation with Utility Bonds

I have also recommended buying individual bonds of regulated utilities over the years. My focus: Bonds of maturing in 5 years or less that are issued by companies with sub-investment grade or “junk” credit ratings.

“Maturing” or paying off at par value in 5 years or less means these bonds have only minimal risk of erosion to inflation. In contrast, inflation can greatly impact the value of the payoff from a bond maturing in 20 years.

Bonds rated BB+/Ba1 or less trade at price discounts to bonds rated BBB or higher because they’re perceived as riskier. And they pay higher annualized yields-to-maturity (YTM) as well. YTM is the annual return you receive from owning a bond until it pays off or matures.

Usually, those price discounts are justified. A company with lower rated bonds, by definition, carries more credit risk. So its bonds will have to offer a higher prospective return to compensate.

Regulated utilities, however, are a special case. Uniquely among industries, no sector company has ever gone out of business.

Sometimes companies file for Chapter 11 bankruptcy protection. In the previous decade, for example, PG&E Corp (NYSE: PCG) did so to buy time to resolve billions of dollars of liabilities resulting from the Camp Fire.

The stock price fell to low single digits at one point. But the utility was ultimately able to work with California regulators to resolve its situation. And it’s since emerged from bankruptcy and resumed paying dividends, with the stock price rising more than six-fold. PG&E bonds’ interest payments were temporarily halted. But bondholders were made completely whole—both on principal and back interest—when the company came out of Chapter 11. Investors who ignored the media storm and bought got a windfall.

Utilities have been able to fully financially recover from every catastrophe thrown their way because they’re dominant providers of essential services. At the end of the day, their product is vital. So effectively stopping the bleeding from the catastrophic event, maintaining/restoring good relations with state regulators and cutting costs and debt has always eventually led to full recovery.

That means junk-rated utility bonds throughout history have invariably become investment grade again. As ratings have increased, perceived risks have dropped and the bonds’ prices have increased.

At this point, PG&E’s bonds are still rated below investment grade. That means they still have some upside as the utility continues to strengthen. Earlier this month, the company raised its guidance range for 2026 core earnings to $1.64 to $1.66 per share. That’s not only a sign of growing strength, paired with projected 9% plus growth through 2030. But it’s an extraordinarily tight range, demonstrating how few factors can upset the company’s steady strengthening.

The biggest drawback buying individual corporate bonds is they tend to trade by appointment. Unlike when you buy a stock, there’s no guarantee the specific issue you want will be available when you place an order. That’s because even the biggest issuances of large companies are only a few billion dollars. And most of those who buy are going to be large institutions that plan to hold until maturity.

That includes everything issued by PG&E. And it means you’re going to be most effective working with a broker who has a handle on what’s available.

The good news is all of a company’s bonds are likely to trade at similar prices and yields to maturity, because they have basically the same credit risk. So, you can pretty much get the same results buying a PG&E bond maturing in 2032 as one paying off in 2031 or even 2035.

Bottom line: Buying junk-rated debt of regulated utilities that matures in five years or less offers the prospect of a generous yield and capital gains with very little credit or inflation risk.

Stocks of utilities with unfolding “rags to riches” stories offer even more upside. The caveat is companies with the most potential reward, by definition, are going to be less far along in their recoveries. Some may not even pay current yields. And patience is essential, as is willingness to live with some volatility in the near term.

Beating Inflation

How much inflation should we worry about this year? My view since the now cancelled “Liberation Day” tariffs were announced last April has been that import taxes were as likely to slow the economy as boost prices. And that appears to be the case, with companies not connected to the AI boom cutting back investment and Q4 GDP growth slowing sharply to just 1.4 percent.

On the other hand, Federal Reserve Governor Christopher Waller commented last week that “continued improvement in the labor market” and higher inflation would tilt his decision in favor of not cutting rates next month. And the Fed’s preferred gauge of inflation at last count ticked up to 3 percent, versus the often stated 2 percent long-term target.

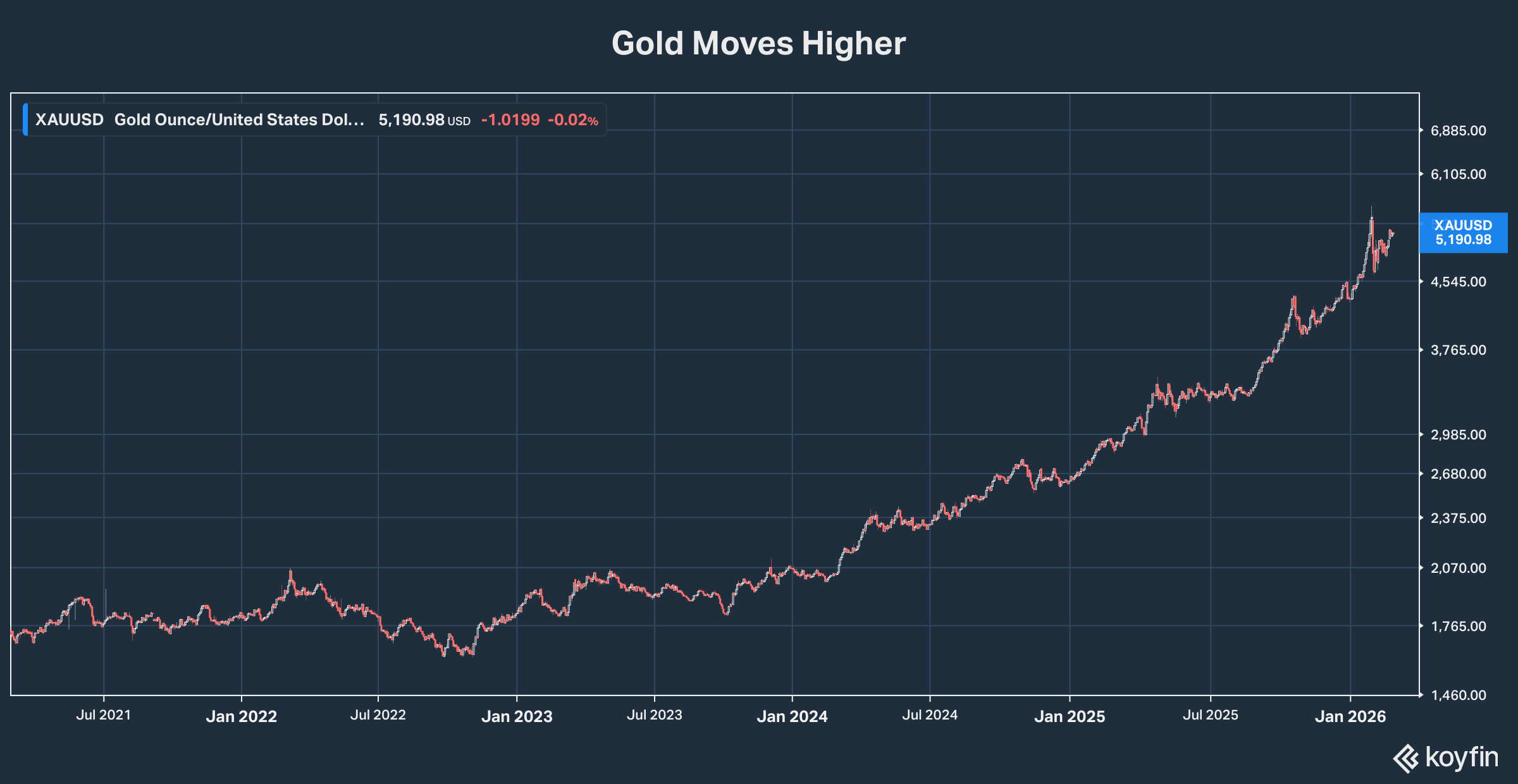

Not every commodity’s price has moved higher. But oil has continued to strength, while copper prices have surged. And after dropping sharply in late January on the news the president will appoint Kevin Warsh as Fed Chairman, gold prices moved over $5,200 an ounce last week.

Gold has been described as the only financial asset that’s not simultaneously someone else’s liability. And since then-President Richard Nixon ended the gold standard in 1971, it’s been a reliable barometer of investors’ inflation worries.

That doesn’t mean an actual burst of inflation has inevitably followed a surge in gold. But one certainly can’t be ruled out.

A little over a week after losing at the Supreme Court, the government appears determined as ever to find some way to tax imports heavily. To date, companies have been mostly eating them, unless they enjoy pricing power like utilities and electricity producers. And we’ve seen our first lawsuit attempting to claw back the illegal Liberation Day tariffs. But it’s a safe bet higher copper and steel prices are starting to have an impact. And if the newly announced import taxes stand, they’re likely to be passed on as well.

That’s why we need to be prepared for inflation. Better, income investors should bolster portfolios with stocks especially that make this enemy our friend.

We’ve done well on that score over the past year in the Dividends Premium portfolio. The updated version is in the attached table “Dividends Premium Income Portfolio.”