How to Beat Rising Inflation

My portfolio has answers for income investors.

Editor’s Note: Thank you for reading Dividends Roundtable!

Inflation is back with a vengeance. But the high quality, dividend stocks we own in the Dividends Premium portfolio are a proven antidote for income investors.

This month, I highlight Q1 earnings and guidance for each of the positions in this report. And my top takeaway is they continue to demonstrate the balance sheet strength and pricing power in their underlying business to survive and thrive in this increasingly difficult environment.

My top fresh money buys for conservative and aggressive investors are both high yielding, deep value stocks that have affirmed their value with solid Q1 results and updated guidance. I also highlight several companies in this report where I may trim positions in coming weeks. Stay tuned.

Have a question? Then join my Dividends Roundtable web chat discussion on the Substack application, which I host 24-7. And if you’re not yet a subscriber, please check us out by clicking on the link in this email.

Here’s to your wealth!--RC

Parse it out however you want. But there’s no doubt inflation is on the rise in the USA.

Even the so-called “core” Consumer Price Index was up 0.4% in April from March. The CPI itself, which includes food and energy, advanced 0.6% on a “seasonally adjusted basis.” And the Producer Price Index was up a whopping 1.4%.

Put another way, even if you toss out soaring food and gasoline prices, the official annualized rate of consumer price inflation is 4.8%, compared to the Federal Reserve’s official long-term target of just 2%. And with annualized PPI inflation 16.8%, CPI inflation seems likely to go higher still.

Not surprisingly, investor expectations of inflation have followed CPI and PPI numbers higher.

Friday’s action highlighted the stock market’s vulnerability. The only sector closing higher was energy, as even the artificial intelligence-related favorites leading the S&P 500 higher over the last month sold off.

NVIDIA (NSDQ: NVDA), for example, that day lost more than -4.4% of its nearly $5.5 trillion market value—though that’s still greater than the GDP of every country in the world except America, China and Germany.

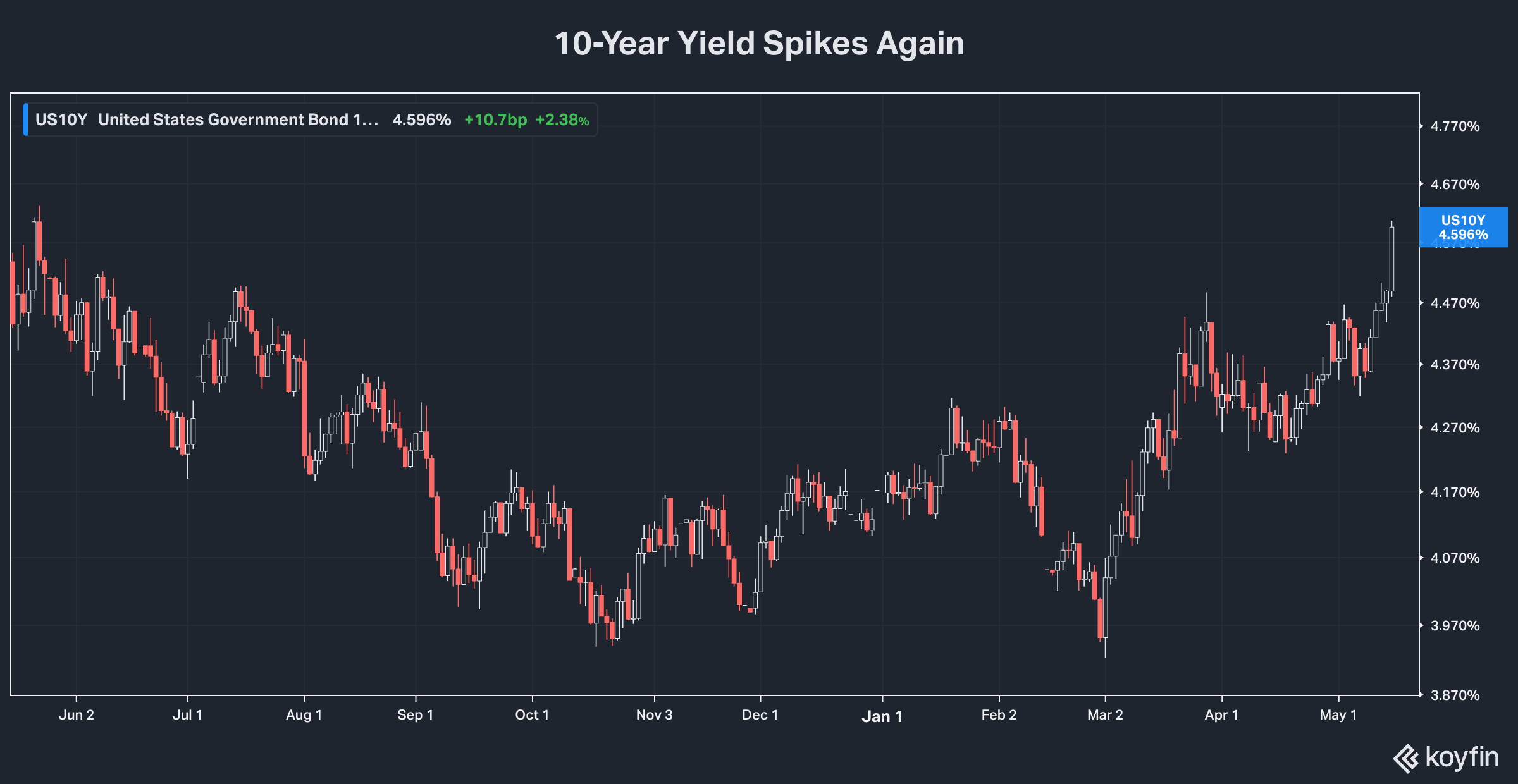

But as is always the case when inflation becomes an issue, the bond market was where the real action was. The benchmark 10-year Treasury note yield is now back at almost 4.6%, its highest point since last summer. And with the 30-year Treasury yield breaking over 5.1%--and the long-compressed yield curve starting to stretch out—there’s good reason to fear this key interest rate may go quite a bit higher.

This Portfolio is Still Making Money

Time for income investors to go to cash and wait out what’s coming? Not unless you want to sacrifice both high income and the still substantial upside of high quality, reliably growing dividend paying stocks.

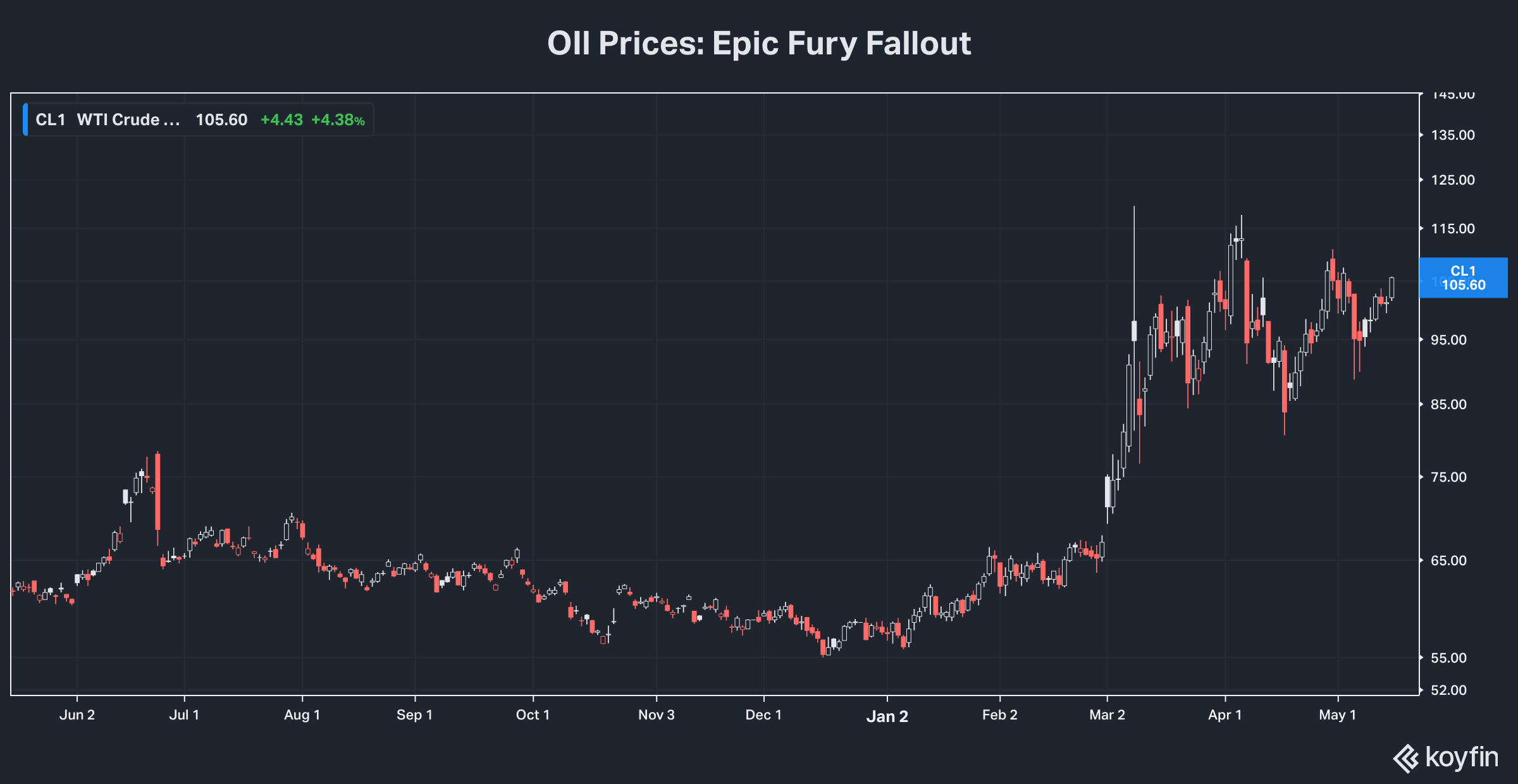

It’s been two-and-half months since the launch of currently stalemated Operation Epic Fury, and the resulting scramble of global energy markets. It’s about 13 months since the Trump Administration announced “Liberation Day” tariffs, disrupting global supply chains.

The 10-year Treasury note yield is roughly 60 basis points higher than where it began 2026. And borrowing costs have backed up with them.

To the extent inflation expectations keep rising, we can expect selling by algorithm of certain sectors deemed “interest rate sensitive.” That will touch numerous dividend stock groups such as real estate investment trusts and utilities. And the kind of large capitalization stocks held in ETFs sponsored by mega-corporations like Vanguard will potentially be most affected.

I expect we’ll wind up with another good opportunity to deploy cash in high quality stocks at bargain prices. Some may be companies we already own. Others may be in sectors where stock prices are currently unmoored from business value—and are currently uninvestable except as momentum-based trades.

But for anyone tempted to buy into conventional wisdom that stocks paying dividends are basically bond substitutes, consider this:

Here in mid-May with inflation fears on the rise, our portfolio stocks are up the most they’ve been all year at 18.14%. That’s after an average 2025 gain of nearly 36%, the year inflation started rising and taking the 10-year Treasury yield up with it.

Our stocks’ performance so far is about 10 percentage points better than the S&P 500. And we’ve avoided exposure to the historically expensive and therefore vulnerable Big 7 Tech stocks.

Since inception in late 2018, the portfolio is ahead by 100.61%. That’s close to a new high-water mark. And that’s assuming harvesting cash dividends rather than reinvesting. Our weighted yield is steady at 4.4%, as holdings’ dividend growth has partially kept pace with rising stock prices.

I never enter a year with the primary objective of beating the S&P 500 per se. With a dividends and value approach, we will most likely beat when the big market averages have a bad year. But I certainly never hope for or bet on a debacle. And we’re always going to make a lot more money when the overall stock market is on the rise.

Rather, I want to help readers build a long-term stream of high and rising income from stocks that will boost principal over time. And we use the principles of balance and diversification to limit overall portfolio volatility, so no one following the strategy will ever have to eat their seed corn by accessing funds at a bad time for the stock market.

The four basic strategy rules:

· Build and hold onto positions in companies with underlying businesses that are positioned for long-term growth and have healthy balance sheets. I sell when the business numbers tell me a company no longer offers that, even if it means taking a big loss.

· Maintain a cash reserve against the possibility of a broad correction. My favorite parking place for cash is still the Vanguard Federal Money Market (VMFXX), which currently has a 7-day SEC yield of 3.54%. It’s not the only suitable money market investment. But anything you choose should be sponsored by an organization that can protect $1 net asset value. And you should be able to access funds in a timely manner.

· Never overload on any one stock. That’s no matter how attractive a particular company looks or even if it trades below its “Dream Buy” price (see attached table), which are entry points that in the past have ensured windfall gains. Spreading your bets is the surest way to limit risk you’ll be taken down by an unexpected setback with a single company. I can guarantee if you invest for long enough, this will happen to at least one of your stocks. Diversification rather than doubling down also takes the emotion out of decision making.

· Make fresh investments in increments of two to three, rather than all in one purchase. And I will pare back positions when a stock rises far and fast enough to be out of balance with the rest of the portfolio.

So, what am I advising now?

First, let’s look at the current environment. The S&P 500—and therefore all those trillions of dollars invested in related ETFs and close cousins—is still an historically high 36.35% weighting in just 7 Big Tech stocks.

In fact, after the AI-excitement run-up, NVIDIA alone is 8.9%. That’s ahead of company earnings on May 20, which while likely to be quite robust will have a tough time meeting Cloud 9-level expectations.

All seven of those stocks currently trade at near historic price multiples to business value. And the only close precedent to where they are now in terms of weighting and price is 2000, just before the Great Tech Wreck took down the then equally revered drivers of the Information Technology revolution.

Certainly, there are plenty of stocks right now selling relatively cheaply to business value. That includes many companies in this portfolio, as my discussion of our positions’ earnings and guidance calls later in this report will readily affirm.

Stocks of companies like these did largely hold their own during the Tech Wreck. Businesses remained solid. They continued to pay a reliable and growing dividends. And when the market recovered, they became leaders over the next several years.

But very few stocks of any variety completely avoided any downside in 2000-02. And it’s been the same in every real bear market that lasted long enough for investors to stop buying the dips.

Bottom line: If this decade’s version of the late 1990s Tech rally ends similarly, even these stocks are likely to give some ground. That means at a minimum not chasing stocks that are trading above my highest recommended entry prices. And it also means being willing to pare back on our bigger winners, even though we continue to believe strongly in their long-term prospects.

It’s far easier to spot the catalyst for a market decline after it’s happened than in advance, when it might do some good. But rising inflation has been a reliable harbinger of doom for previous stock markets that are trading on momentum rather than business value.

How likely is inflation to rise further in 2026? The Trump Administration’s Liberation Day tariffs were eventually struck down by the courts. And its attempt to replace them with a 10% levy on all imports met the same fate. But the 50% tariffs on copper and steel are still in place. So are various levies on other products, particularly from China—still America’s third largest trading partner.

Tariffs are simply taxes on imports. And the cost of Trump Administration levies has either been absorbed by American businesses or passed onto consumers.

So has the cost of supply chain disruption caused by barriers to trade. That’s a lot harder to quantify, in part because the government doesn’t collect data. But it’s a reasonable assumption that the additional expense of dodging unpredictable new tariffs has been at least as much as the actual taxes, again with the entire cost either eaten by business or passed onto customers.

At this point, there’s no way of knowing if/when tariffs will be reduced. The second Trump Administration has frequently used them as a negotiating tool to get some “better” deal. And the Biden Administration largely doubled down on the import taxes held over from the first Trump Administration.

But so long as there are import taxes, they will add to costs and therefore inflation. They will also disrupt supply chains and worse investment flows, threatening production and supply. And that’s in addition to anti-immigration policies, which have choked off the supply of labor to many businesses including agriculture.

It’s within the power of politicians in the US and Iran to end the current Middle East war. Even opening the Strait of Hormuz tomorrow and starting energy infrastructure repairs won’t alleviate supply strains and restore now greatly depleted inventories in Europe and Asia. But it could greatly reduce expectations of future inflation.

That in turn would provide some cover for incoming Federal Reserve Chairman Kevin Warsh to push for further cuts in the Fed Funds rate. The Chairman is only one of 12 votes on the Federal Open Market Committee that sets the central bank’s monetary policy. But like outgoing Chairman Jerome Powell, Warsh comes in with a great deal of influence to push the agenda he called “regime change” during a contentious confirmation process.

The big risk is that what the Warsh Fed does is perceived by the bond market, banks and other lenders to be soft on inflation. If that’s the case, look for inflation expectations to skyrocket, and interest rates/borrowing costs along with them, regardless of what the Fed Funds rate is.

A big boost in borrowing costs is, of course, also a pretty good way to slow the US economy to a crawl, if not push it into outright recession. And if things slow down quickly, it could wind up reducing inflation expectations and ultimately interest rates. But history shows that’s not an environment that would be kind to stocks.

A real reduction in inflation expectations would bring down borrowing costs. That would be very positive for dividend paying stocks, boosting their appeal versus alternatives like cash and by putting the brakes on rising interest expense as an underminer of earnings and growth.

Unfortunately, these are all factors beyond our control as investors. And that alone is a reason not to chase stocks above prices where they’re firmly grounded in underlying business value.

As for going to cash, here’s something else to consider. Inflation expectations always set the tone for longer-term interest rates and borrowing costs. The Fed can only influence the 10-year yield by helping raise or lower those inflation expectations.

The central bank, however, does have a great deal more power when it comes to short-term rates. One potential consequence is we could actually see a decline in short-term rates at the same time longer-term rates are rising. And that means cash yields including for money market funds could fall at the same time rising inflation worries are hitting the stock market.

Cash would still hold its value. And it would be there for buying stocks when prices drop enough. That’s good reason to keep holding a fair portion of it, as we do in the model portfolio at about 14%. But it’s not a panacea for what ails us now.

Action Plan

So what I’m advising now is basically to stay the course—but with a very, very watchful eye.