It’s August 2025: Do You Know Where Your Money Is?

It’s time to take control and save your portfolio.

Welcome to Dividends with Roger Conrad!

Last week, I posted Dividends Premium, highlighting Q2 results and guidance for our model dividends and growth portfolio. Our broadly diversified picks have an average year to date gain of close to 20%. In contrast, my recommendations in Dividends Premium REITs, which posts Monday, are basically flat for 2025. But like the companies featured in Dividends Premium, they are performing well as businesses with a majority raising full year guidance. And that’s almost always a formula for big gains in coming months.

A subscription to Dividends Premium gets you both advisories. Give it a shot by clicking on the link in this email or elsewhere on the Substack application. I also host Dividends Roundtable on Discord 24-7, where I post comments and field questions. Here’s to your wealth and a great rest of the summer!—RC

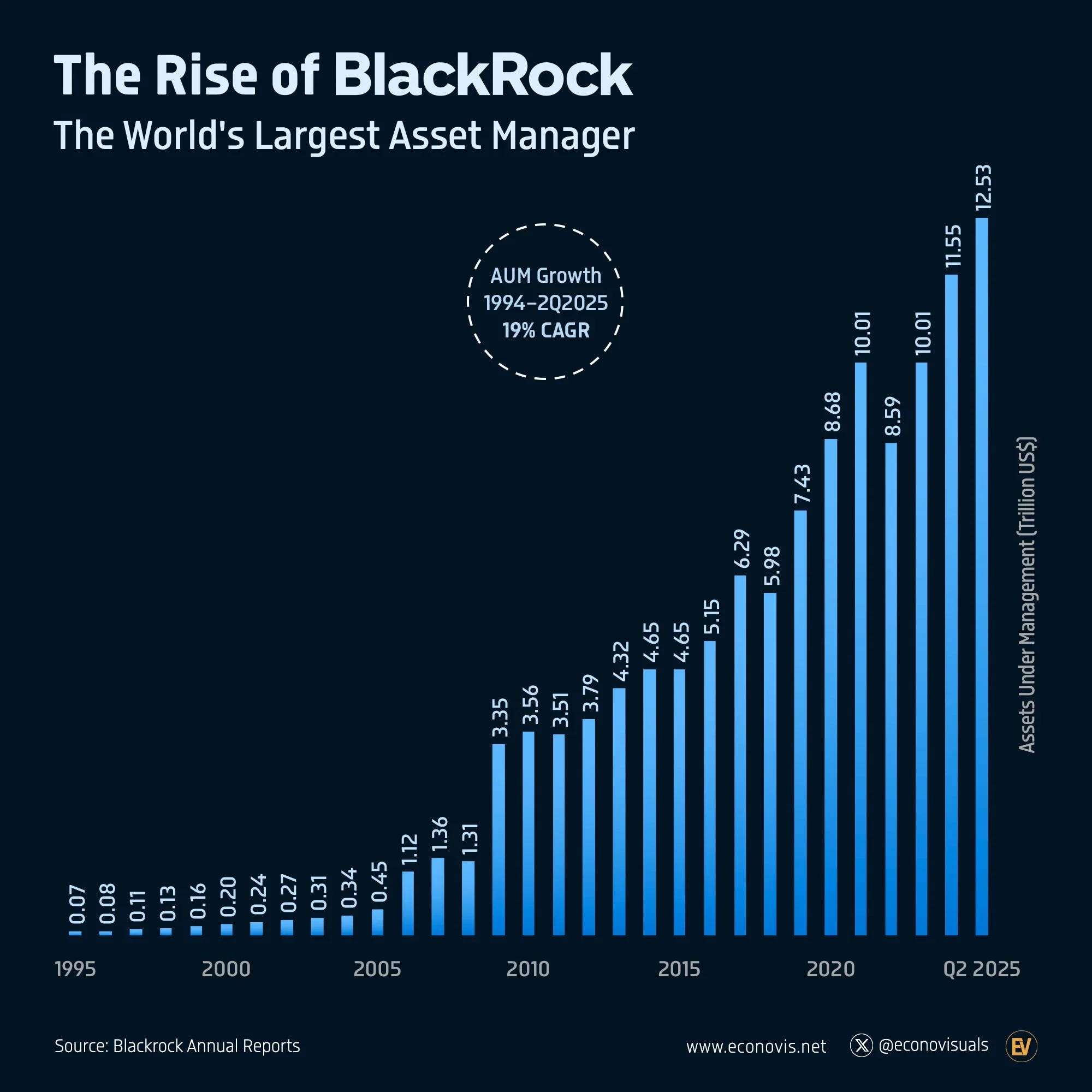

Depending on the source, the weighted S&P 500 index currently encompasses 80% of US stock market capitalization. And the so-called “Big 3” of “passive investing”—Blackrock, Vanguard and State Street—combined are the largest shareholder in companies comprising 88% of the index’ total capitalization.

It wasn’t always this way. Before the mid-1980s, individual investors acting through brokers made the vast majority of stock market trades. Then came the rise of mutual funds, billed as offering expert money management previously only available to Wall Street insiders.

The rise of super managers like Peter Lynch at Fidelity Magellan coincided with the soaring popularity of Louis Rukeyser’s Wall Street reaching millions of TV viewers. And the era of guru-led investing began, reaching a peak in the late 1990s as big technology stocks made many investors millionaires—provided they didn’t stay at the party too long.

The market crashes of 2000-02 and later in the decade in 2007-09 was a wakeup moment for many that no matter how well marketed, “experts” didn’t always get it right. In fact, those who fell into the trap of believing in their own hype often failed spectacularly.

Thus was born the era of ETF dominance, in which we now live. The premise was simple: Exchange traded funds were expertly constructed and by definition diversified to reduce risk. And best of all, there was little or no management fee, as was the case with mutual funds.

A rising tide raises all ships. And in the post Financial Crisis environment, investors saw quickly that broad based ETFs –including of the plain vanilla S&P 500 variety—were doing as well as anything else. ETFs’ popularity skyrocketed.

That’s when the Big 3 of Blackrock, Vanguard and State Street took advantage of the moment to shift their marketing in an even more profitable direction.

Being profitable in the ETF business depends on quickly gaining and maintaining scale, meaning a critical mass of investor dollars. Otherwise, issuers don’t collect enough fees to offset the constantly rising cost of the legal, regulatory and accounting burden.

When an ETF is popular and attracts enough investor dollars, these expenses are manageable. But when an ETF becomes unpopular, the investor dollars go elsewhere. The costs become an ever-greater load to bear. And eventually, the issuer will shut the whole thing down, returning cash to the ETF’s unitholders.

Morningstar estimates fully one-third all ETFs ever started have shut down. In 2024, that number was 189. Some were ETFs set up to bet on a particular market trend, strategy or sector. And when it lost popularity, investor dollars fled. Others just never gained enough size to be worth continuing.

Investors always get cashed out at asset value net of closing costs, just as shareholders of mutual funds do. But that’s never going to happen when it’s a good time to sell the ETF’s assets—when prices are high. In fact, if you’re in an ETF that shuts its doors, you’re getting sold out near the bottom. So much for buying low and selling high!

Blackrock, Vanguard and State Street didn’t like shutting down ETFs any more than investors like getting cashed out at a low point. So they’ve added a new layer of marketing: One size fits all “passive investing” plans that shift funds between the issuer’s ETFs by algorithm—or in these of “target funds” by calendar.

Passive investors pay little in fees. And after providing some basic information on objectives and lifestyle, they don’t make any decisions. As for the Big 3 and other passive investing firms, they effectively have a captive market to keep their ETFs at scale. And the more passive dollars they attract, the more their coffers swell.

What’s wrong with this picture?

By going passive, investors are effectively giving up the benefit of learning from making their own decisions. They’ve also effectively tied their financial fate to Wall Street’s latest and most profitable marketing pitch—that you’re better off not making investment decisions for yourself, or even the help of someone with experience and knowledge navigating financial markets.

I doubt Vanguard executives would ever disclose how much investment they have in Target Funds versus managed accounts—which they actually offer to customers with $5 million portfolios. But my point is whether you’re talking about physical, mental or financial health, you’re going to get best results by systematically exercising control yourself—not relying on a slick Wall Street product that’s clearly marketed for the masses.

OK, enough of the sermon. There’s also a timely reason to take charge of your portfolio now Mainly, the risk is rising rapidly that the whole passive investing house of cards is about to come crashing down.

We’ve already seen some pretty clear warning signs.

Earlier this decade, the value of Target funds approaching maturity collapsed when inflation started rising and the Federal Reserve began raising interest rates. These funds had followed their invest-by-calendar strategy to load up on bond ETFs, precisely at the time the bond market peaked. And rising interest rates undermined bonds’ value.

As my friend and colleague Elliott Gue has written in his Substack publication “Smart Bonds,” the bond market is a good bit healthier now. And there are many ways to make money if you’re willing to be a little bit active. But again the key word here is active—just sitting back and expecting to make money in the bond market is no longer an option.

The worse danger now for passive investors, is from the stock ETFs. And the most at risk is the weighted S&P 500 itself—which is the basic bedrock of what Wall Street’s Big 3 passive investing companies offer.

If market history teaches us one thing, it’s that the market’s premier index is at its most dangerous to your financial health when it’s:

· Extremely over-weighted in a handful of stocks in a specific sector, and under-weighted in pretty much everything else.

· Those over-weighted stocks are extremely expensive in terms of standard measures of business valuation.

Both are the case today.

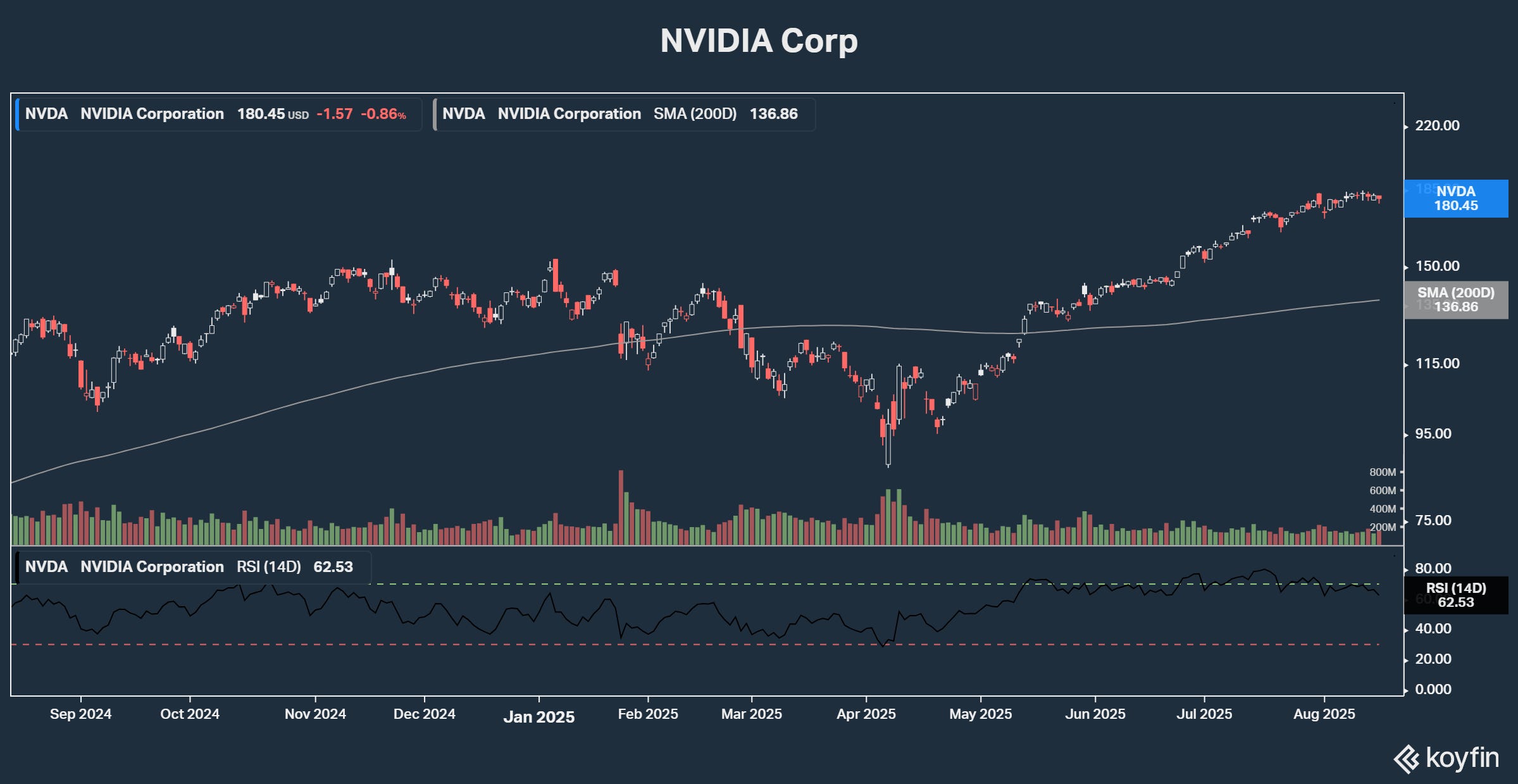

The S&P 500’s number one holding right now is NVIDIA (NSDQ: NVDA) at 8.1%. At number two is Microsoft (NSDQ: MSFT) at 7.1%. The next six—also Big Tech stocks—weigh in at 21.7%, That’s an historically high 37% in just 8 stocks, or well over one-third of the entire index.

In contrast, the entire financial sector—including all the big banks and Wall Street firms, as well as regional and community banks—weighs in around 7%. Big Pharma and the oil and gas industry are both less than 3% as are utilities. Real property is around 1%.

The last time Big Tech was this heavily weighted in the S&P 500 was in 2000, on the eve of the great Tech Wreck. And then as now, Big Tech stocks are priced for perfection—then for the promise of the Information Technology revolution, now for artificial intelligence.

IF anything, IT adoption has greatly exceeded expectations since the early ‘00s. And count me among the believers that AI will transform the global economy as well, no doubt in ways few are thinking about now.

But it’s going to take time. And if we learned anything from the first Tech Wreck, it’s that markets don’t have a lot of patience with extremely high prices stocks. The great march of history will continue. But the higher a stock’s price rises, the more vulnerable it is to even the slightest disappointment. And when that happens, it can take many years to regain previous highs—over a decade for more than a few of the market’s leaders of the 1990s.

So why is this important to today’s passive investors?

You won’t find this fact advertised by the Big 3. But the S&P 500 was actually underwater including dividends in the decade of the ‘00s. That was at a time when multiple non-Tech sectors paid huge returns.

The S&P’s problem then was that it was so heavily weighted in Big Tech when the decade began that it took years to restore balance to other sectors. Oil stocks, utilities, real estate investment trusts and other groups all had long days in the sun, producing outsized profits for investors. But the S&P was largely blocked from the warmth by underperforming Big Tech.

Market history never repeats exactly. But more often that not, it rhymes. And just as Target fund owners received a shock from crashing bond ETFs, they’re set up for potentially an even bigger meltdown when the extremely expensive Big Tech leaders eventually fly too close to the sun.

The single most important step every investor should take now is to get off the couch and take control. Maybe you can’t exit passive investment products right away. If that’s the case, look around to see what options you may have that do not involve weighted S&P 500 ETFs. Some retirement plans, for example, offer exposure to foreign stock ETFs—which are benefitting this year from the declining US dollar.