It's Time for Monthly Dividends

Reliable, consistent cash returns are the cure for today's big picture insecurity.

Aston Martin DB5, James Bond

Editor’s note: Thank you for reading Dividends Roundtable!

Volatility is the one constant in global stock markets. Sometimes, it’s the result of business developments and price changes are permanent. But more often, it’s ephemeral factors like sentiment triggering big moves. And investors who focus on the big picture issues rather than the health and growth of the investments they own can lose big.

One of the surest antidotes to excessive macro-thinking is just focusing on getting paid. Dividends are cash on the barrel. Payments show up in your account, regardless of the latest inflation numbers or developments in geopolitics.

I like dividend stocks for another reason: Sustaining a generous and growing payout has historically been the surest sign of a company’s inner strength. And stocks of healthy, growing enterprises always appreciate in the long-term. Your money grows and you get paid while you wait.

Monthly dividends go one better, especially for those of us living off our portfolios. And they’re the subject of this week’s post.

Got a question or comment? Join the discussion at forums I host 24-7 for full Dividends Roundtable members on the Substack and Discord applications. Coming very soon: The Dividends Roundtable application, with an exclusive chat forum and stock databank. Here’s to a profitable summer!—RC

With just two trading days left in first half 2026, the average year-to-date return for Dividends Premium stocks is a robust 18%. The portfolio itself sits near its high-water mark, up 104% plus since inception.

We’re getting paid am annualized yield of 4.5%, based on the weightings of the 19 positions. And that includes a 13.6% position in my favorite cash alternative Vanguard Federal Money Market Fund (VMFXX), which has a 7-Day SEC yield of 3.57%.

It’s a fair bet most investors aren’t aware of how competitive dividend stocks have been generally with the big market averages. The iShares Trust Dividend Select Dividend ETF (DVY) is too heavily weighted in a small number of big capitalization names for my taste. And the yield is paltry at 3.3%, largely because the ETF’s sponsors churn the portfolio to chase capital gains.

But the DVY is ahead 13.8% so far in 2026. And that beats the S&P 500 by 6.3 percentage points, or almost a 2-to-1 margin.

Dividend stocks’ solid performance comes despite rising inflation, which no matter how you measure is running at its hottest in three years. It’s despite spiking oil prices and global supply chains disrupted by wars, geopolitics, tariffs and other trade barriers. And it’s despite the Federal Reserve pivoting more hawkishly than many investors expected.

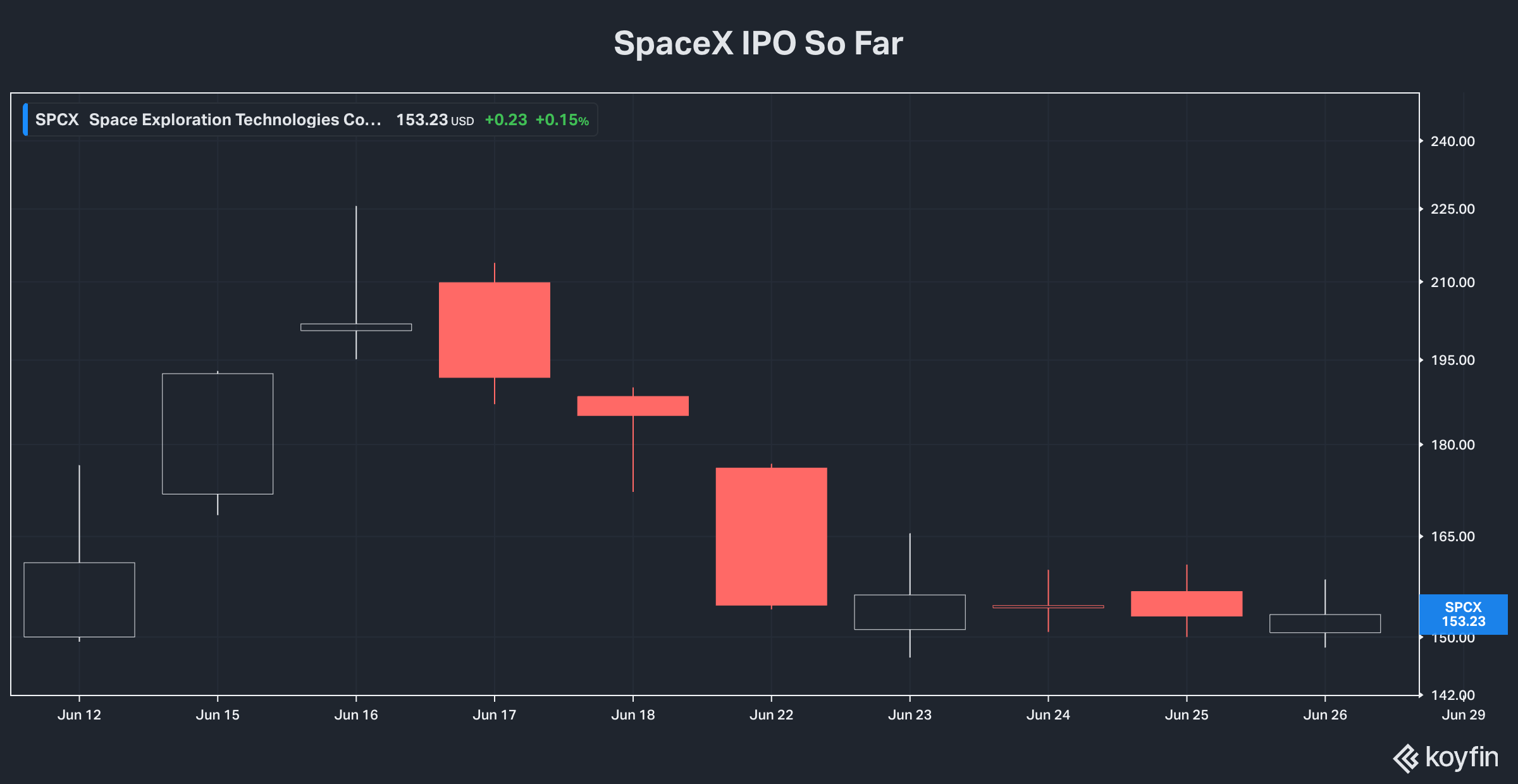

Dividend stocks are also outperforming at a time of breathless hype for anything to do with artificial intelligence, especially the seven biggest technology stocks that still comprise more than one-third of the S&P 500. And they’re on top at the same time the Elon Musk’s Space Exploration Technologies (NSDQ: SPCX) just launched what was arguably the most expensive IPO in history.

On June 16—the stock’s third day of trading—SpaceX shares soared as high as $225. As of Friday’s close, they’re back in the low 150s. But the stock is still one of the priciest in history with an enterprise value 105X annual sales and at nearly 26X book value. Their $2 trillion plus market capitalization—over 80% owned by Mr. Musk—is roughly 55X its sales for FY2026 and 766X forecast earnings for FY2027, which appear based on wildly optimistic assumptions.

That’s not to say SpaceX won’t succeed. And the same is true of the so-called “Magnificent 7” big technology stocks that are still a return-shaping 34% of the S&P 500.

Their products are household names. And their stocks are the rock stars of the current market. But like freshly minted SpaceX shares, they’re more expensive relative to any sane measure of business value than even the Nasdaq 100 was circa late 1999, on the eve of the Great Tech Wreck. And they’re all stratospherically priced on the very same currently popular investment theme: Artificial intelligence as a primary driver of global economic growth and investment.

You might recall that the Information Technology (IT) stock market leaders of the 1990s did go on to change the world. But prices in the late 1990s rose too far too fast. Business kept booming. But the stocks were priced for much better and faster. And as a result, the stocks busted. And the Nasdaq didn’t best its 2000 high for another 15 years.

It’s Time for Dividends

If your retirement money is passively invested in some generic “stock” option, your portfolio’s fortunes are inexorably tied to the fate of this so-called “Magnificent 7.” And unless you want to meet the same fate as those who stayed too long in Tech a quarter century ago—basically a “lost decade for returns”—it’s time to do three things:

· Take control of your portfolio. If you’re passively invested, at least find out what’s inside the funds you own. If you’re locked into a retirement plan, there may still be options available that aren’t historically heavily weighted to a handful of stratospherically priced stocks. Making your own investment decisions is always best. But if your choices are limited, balance and diversification is always best—and arguably now more than ever

· Stop mono-focusing on the macro. Big media are in the business of getting your attention. Investment media is no different. And those who pontificate about big picture issues like geopolitics and inflation are always going to command the largest audiences. But the macro is only important insofar as it impacts the actual investments we own. And 99% plus of what you’re going to see on television or the Internet simply does not. The micro is where the real action is. And it’s where our attention needs to be, especially now.

· Build a diversified and balanced portfolio of high-quality dividend stocks. I’ll never chase a high yielding stock unless it’s backed by a growing company. And you’ll never have income without growth for very long. But there are plenty of great, growing high yielding stocks to choose from now.

Even dividend stocks can become overvalued and overextended. And there are more than a few in my coverage universes. But there are also dozens of companies that have raised dividends at least once already this year yielding at least 4 to 5 percent. That includes 27 of the REITs I track in Dividends Premium, as well as 42 companies in my utilities and essential service company coverage.

That’s remarkable value at a time when the stock market is arguably well overdue for another correction of at least 20%, and possibly worse.

Historically, nothing much outside of cash is fully spared from a major market selloff. And it’s likely even the highest quality dividend stocks will see some near-term red ink the next time Wall Street really rolls over.

But low valuations, high yields and business resiliency are ultimately powerful backstops for stocks in falling markets. And so long as companies stay healthy on the inside, their stocks will be among the first to bounce back in the recovery.

After Big Tech topped out in 2000, there was a great rotation to the rest of the stock market. Dividend paying stocks from real estate investment trusts to Big Oil shares were major beneficiaries. Even utilities—many of which were caught up in the wreck of Enron—were huge winners by mid-decade.

We’ve yet to see Tech Wreck II. And in fact, SpaceX’s IPO still looks like it will be the first of many we’ll see in the sector this year. But dividend stocks are already consistently outperforming. And the longer the bull market continues, the more gains they’ll likely pile up this year.

When the Macro Matters

It’s fair to ask what macro issues in the news now could affect the all-important micro—meaning the financial health, growth and investment ability of the stocks we own. And the big one is inflation.

If you’ve filled up your tank lately, you’ve no doubt noticed the spring spikes in the price of a gallon of gasoline have moderated a bit. That’s the result of global oil prices backing off, with the North American benchmark WTI price sliding under $70 a barrel as of Friday’s close.

Falling crude in turn is presumably the result of growing optimism that global energy flows will return to something resembling normalcy, now that the US and Iran have signed a “memorandum of understanding” to end their conflict and keep the Strait of Hormuz open.

On the other hand, inflation was rising long before Operation Epic Fury was launched. And the Federal Reserve’s preferred inflation gauge—the Personal Consumption Expenditures Index—rose by 4.1% in May, up from a 3.8% year-over-year rate in April. That’s the largest increase in more than three years. And it’s more than twice the central bank’s official inflation target of 2%.

Excluding food and energy, PCE inflation was 3.4%, the highest level since October 2023. The so-called “Trimmed Mean PCE”—excluding components with the biggest movements in either direction—was only 2.4%. But alarmingly, it’s the “a-cyclical” elements that are increasing driving core PCE inflation, rather than “cyclical” factors that tend to be less permanent.

Interestingly, peak inflation earlier this decade was primarily driven by cyclical factors that only peaked in mid-2023. By then, the a-cyclical factors—which include the cost of healthcare, financial services, technology and telecom, transportation, clothing and motor vehicles—were declining sharply.

One reason a-cyclical inflation declined earlier this decade was global supply chains were unfreezing from pandemic restrictions. Now tariffs, trade barriers and geopolitics are disrupting them again. And the result is risk inflation may remain higher for longer.

Inflation affects the micro in several ways. The price of materials and cost of labor rises. Customers’ budgets are more stretched, potentially threatening sales volumes and companies’ ability to pass on costs in prices. Borrowing costs tend to stay higher for longer, raising interest expense when maturing debt must be refinancing. And a higher cost of capital raises the bar on new investment, which all else equal means less opportunity to grow.

Two key strengths are necessary for companies to thrive during inflationary times: Strong balance sheets and pricing power. And it’s essential any stocks you own feature both, whether they pay generous dividends or not.

Both strengths are hallmarks of the stocks in my Dividends Premium portfolio. And they’re one big reason why I’m comfortable owning them now with inflation risk elevated.

Dividends = Constant Returns

Another good reason: Held together in my recommended allocations, their diversification and balance combined with the cash component minimizes near-term volatility and risk. And we realize high and consistent monthly income.

That’s mainly a function of payment dates in different months. Four holdings, for example, distribute dividends in January, April, July and October. Three pay in February, May, August and November. And five pay quarterly in March, June, September and December. I also hold three positions that make larger payments twice a year.

Each week, I highlight links to the Dividends Premium Portfolio and Dividends Premium Dream Buy tables. This week, I’ve put together a third: The Dividends Premium Dividend Chart, also accessible by clicking on the link in this post.

In it, I highlight the dividends investors following our model portfolio stock weightings would receive each month of the year—shown both by position and total for the month. Monthly amounts don’t match up exactly. But even in the lighter months, there’s consistent income.

What about buying stocks that pay dividends on a monthly basis?

I currently hold just one monthly payer in the Dividends Premium portfolio, in addition to my favored money market fund. But the “First Rate REIT” list in every monthly Dividends Premium REITs post features five, which I highlight in this post. And there are 20 companies in the broader REIT Sheet Rater coverage universe.

Unfortunately, utilities and essential services companies have largely abandoned the practice of paying monthly. So aside from a pair of Brazilian stocks that make irregular payments throughout the year, your choices are mainly closed-end funds and ETFs.

That includes one Dividends Premium recommendation: