Offshore Wind Lives!

In energy, investor returns always flow from the project, not the resource.

Thank you for reading Dividends with Roger Conrad!

All subscribers are cordially invited to check out my Dividends Premium service on a risk-free trial basis. That includes the actively managed model portfolio, Dividends Premium REITs and exclusive access to my Dividends Roundtable investment discussion forum, which I host 24-7 on the Discord application. For more on Dividends Premium, see the link attached to this email and the Substack application.

Here’s to a great August!—RC

The energy industry has always been in transition—to less expensive, more abundant and reliable, safer and cleaner sources.

Politics can sometimes get in the way of progress. But sooner or later, better energy projects replace less efficient ones.

Where does offshore wind fit in?

The Global Wind Energy Council (GWEC)—an organization with over 1,500 members drawn from corporations and other institutions in 80 plus countries—reports there were 83 gigawatts of installed offshore wind capacity worldwide at the end of 2024. That’s after 8 GW of installations last year.

GWEC also reports 48 GW of additional capacity in various phases of construction, including the five ongoing projects in US coastal waters. And governments worldwide awarded contracts for another 56 GW during the year. Based on those contracts, GWEC forecasts a 28% average annual growth rate in offshore wind capacity through 2029, and 15% for the subsequent half decade.

China is by far the largest market, with more than half existing generating capacity and 2024 installations. It’s followed by the UK at 19.2% of total capacity and 14.7% of 2024 installations, and Germany (10.9% total, 9.1% of 2024 installations).

Put in perspective, 83 GW of total offshore wind generation is less than 0.9% of the 9,400 GW of global electricity capacity estimated by Statista. And even in China, the leading producer with the industry’s best scaled supply chain, it’s just 0.4%.

Still, there enough of these massive machines in operation right now for us to draw some clear conclusions about offshore wind’s utility as an energy resource.

Let’s start by considering the strengths. Operators don’t have to continually buy natural gas, oil, coal or uranium to keep them running. The process creates no atmospheric or liquid emissions, or solid waste such as spent nuclear fuel or coal ash. And once built, they require relatively little maintenance.

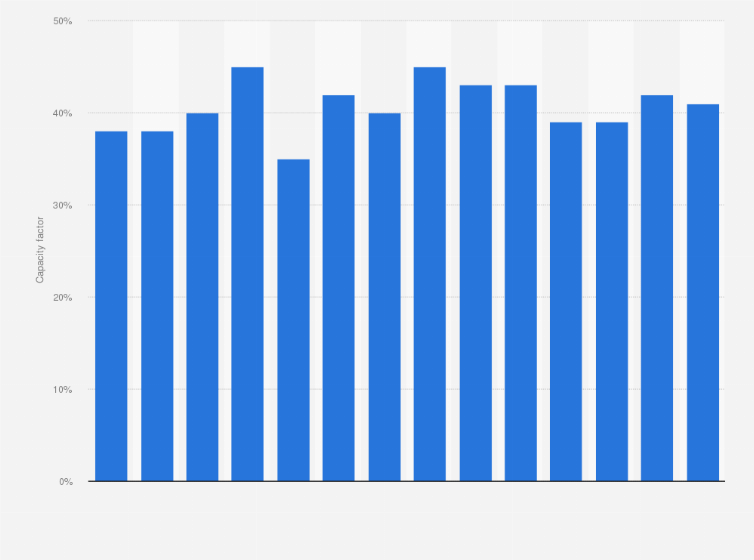

In contrast to onshore wind facilities, actual offshore wind generation is surprisingly reliable, with averaging operating rates 40% to 50% of nameplate capacity. In fact, “unpaid curtailments” are a far bigger headwind for profitability at Northland Power’s (TSX: NPI, OTC: NPIFF) three North Sea facilities in Germany than variable wind resource.

The table below shows 14 years of offshore wind capacity factors for German facilities as captured by Statista. Not only is there little variation from year to year. But this data was collected over a period when installed capacity was rising from close to zero to nearly 10 GW, with all the challenges inherent in starting up major energy projects.

Offshore wind’s chief disadvantage is that even swiftly permitted facilities will take several years to fully plan, site, finance, procure for, build and finally connect to the power grid. And the record for large energy projects of any stripe—from transmission lines to nuclear, hydro and even natural gas generation—is the more time it takes to open, the greater cost overruns are likely to be from initial estimates.

Listening to a coal industry advocate speak about offshore wind’s environmental disadvantages quite frankly rings hollow to me. And recent statements from the US Department of Energy asserting wind is “unreliable,” “not green” and so on and so forth should be taken with an equally large grain of salt.

But as executives of leading US wind and solar energy producer NextEra Energy (NYSE: NEE) have pointed out repeatedly, locating wind turbines at sea does subject facilities to massive wear and tear that doesn’t occur onshore. And despite altering project construction schedules to accommodate marine life, developers can only mitigate potential disruption, not realistically prevent it entirely.

The Trump Administration stands alone among the world’s governments in its hostility to wind power. But offshore wind’s growth had already stalled in the US due to soaring financing costs well before he took office, which the generous tax credits passed in 2022 only partly mitigated.

Tax credits will now phase out completely at the end of 2027 for wind and solar. That’s five years earlier than they did under the Inflation Reduction Act.

Developers will still qualify for the full credit if they meet a definition of “beginning construction” by July 4, 2026—or if they finish work by the end of 2027. If projects are deemed in construction, companies will have four years to complete them to qualify for the full credits. And they still have “transferability” rights to sell tax credit benefits to third parties.

The US Treasury Department still must define what “starting work” means, in a decision due by August 21. And given this administration’s hostility to wind and solar, it’s likely to take a hard line. That’s despite an ongoing effort by Republican senators to soften any new rules, and the likelihood of multi-year litigation hanging up any particularly aggressive action.

The five US offshore wind facilities under construction, however, are well past the decades-old standards to qualify for tax credits. And they’re fully federally permitted, making it extremely problematic for the Trump Administration to stop work as it tried to last spring at Equinor’s (NYSE: EQNR) 810 MW Empire Wind project.

In June, Northland Power proudly announced the connection of the 1 GW Hai Long facility to Taiwan’s power grid, well ahead of schedule. In contrast, Equinor hasn’t said much about Empire Wind since construction resumed.

Neither has Orsted A/S (Denmark: ORSTED, OTC: DNNGY), as it pushes through with Sunrise Wind and Revolution Wind in New England. And Iberdrola SA (Spain: IBE, OTC: IBDRY) said little about its Vineyard Wind facility off the Massachusetts coast, even though its already operating at 25% of capacity.

The exception is Dominion Energy (NYSE: D), which this week updated investors on its 2.6 GW Coastal Virginia Offshore Wind (CVOW) project. Management announced construction is now 60% complete. And the facility is on track for first production in “early 2026,” with full operations at the end of the year.

The company has completed 76% of CVOW’s monopiles after setting a one-month installation record in July. The vast majority of needed components have been fabricated and most delivered. And the construction ship Charybdis is on track for delivery to the project this month, with costs on budget.

There’s still uncertainty about the impact of tariffs on a handful of component costs. Increases will be shared with Virginia ratepayers and 50% partner Stonepeak. And the same is true for whatever transmission charge the PJM regional grid operator assigns the project, though management budgeted in a high-end estimate earlier this year.

But even after all that, CVOW’s LCOE (levelized cost of energy) projects at just $63 per megawatt hour. That’s competitive with new onshore wind, solar and natural gas generation.

During the earnings call, Dominion announced board member Paul Dabbar was stepping down after being confirmed as US Deputy Secretary of Commerce. The company also said it was “quite pleased with how OB3 (federal budget bill) landed,” despite the phase out of wind and solar tax credits.

That’s a great sign Dominion is adapting successfully at the right time to erratic federal energy policy that’s by no means business as usual. And despite offshore wind’s challenges elsewhere, the state of Virginia and the company’s investors will benefit from what continues to be a very good project.