Pricing Power: Your Ticket to Rising Dividends

Here's how to grow income in an inflationary world.

Editor’s Note: Thank you for reading Dividends Roundtable!

Producer or “wholesale” price inflation is now running at the highest rate since 2022. And consumer prices are close behind.

Dividend stocks, however, are still beating the Big Tech-heavy market averages by a wide margin. And the 18 positions in our Dividends Premium model portfolio are at a new high-water mark for 2026 so far, with an average year-to-date total return of 20.67%.

The key is pricing power. Simply, companies able to push on rising costs to customers always keep up with inflation. And that means shareholder returns—capital appreciation and dividends—will as well.

Pricing power and strong balance sheets are the hallmarks of the stocks in this portfolio. With a little less than three weeks left in Q2 2026, there’s every sign they’re going to continue keeping pace this year with rising inflation and the resulting higher for longer interest rates. Two on the bargain counter are this month’s best fresh money buys: Altria Group (NYSE: MO) and Newmont Corp (NYSE: NEM).

As an added feature to the service, I’m now rating each portfolio position on my Quality Grade system from A (safest) to F (riskiest). See the portfolio discussion in this report for an explanation of the five criteria I use.

Have a question? Then check out the Dividends Roundtable investor forums I host 24-7 on Substack and Discord. And keep an eye out for the Dividends Roundtable application I’ll be launching in the near future, exclusively for readers.

Here’s to your wealth!--RC

It’s official: Producer or “wholesale” price inflation is now running at its fastest rate since November 2022.

The Bureau of Labor Statistics’ Producer Price Index for May accelerated 1.1% from April, and 6.5% from the year ago month. “Goods” prices were up 2.8% sequentially and 7.4% from a year ago. The cost of “services” increased 0.3% and 5.5%, respectively. And even stripping out a 22.7% increase in energy prices as well as food and trade services costs, PPI inflation was up 0.8% sequentially from April, and 5.1% from last year.

Consumer price inflation for May was up 0.5% sequentially and 4.2% year-over-year. Stripping out a 3.9% lift in energy costs from April and 3.1% higher food prices, the year-over-year increase in the so-called “core” CPI for May was 2.9%, up from 2.8% in April.

The Federal Reserve under former Chairman Jerome Powell used the “Personal Consumption Expenditures Index” (PCE) as its primary inflation gauge. It won’t be updated for May numbers under June 25. But it’s a safe bet PCE will highlight the same trends, following a 3.8% year-over-year increase for April or 3.3% excluding food and energy.

Rising Inflation and Dividend Stock Returns

During his confirmation hearings, new Chairman Kevin Warsh promised “regime change” at the central bank, including a recalculation of inflation that would strip out the highest and lowest components of indexes. Such a change would moderate the official numbers we’re seeing. And no doubt incumbent politicians would love the chance to take credit for successful inflation fighting, with November mid-term elections approaching.

But as dividend stock investors, we need to consider the following:

· Inflation is driving up companies’ costs across industries. That’s clear from a quick look at income statements. And the longer it remains at these elevated levels, the more those costs will rise, pressuring margins and earnings unless offset.

· Higher for longer inflation also means higher for longer borrowing costs. That means companies with debt as a meaningful percentage of capitalization will continue to see higher interest expense when they refinance maturing debt or borrow to finance expansion. And that in turn will pressure earnings unless it’s offset.

· Elevated operating and financing costs raise the bar meaningfully for corporate investment decisions. That’s slowed expansion moves in many industries, and therefore earnings and dividend growth.

Recalculating inflation to a lower level may provide cover for a Fed Funds rate cut. And that in turn could reduce near-term borrowing costs, such as for credit lines. But if such a move is perceived by lenders as going soft on inflation, it would result in higher longer-term borrowing costs.

I’ve commented on the fact that longer-term borrowing costs are little changed over the past few years. And that includes the now roughly three-and-a-half months since the Strait of Hormuz has been closed, further fracturing supply chains already strained by tariffs and other barriers to trade.

My graph of the 10-Year Treasury Note Yield makes the point clearly. Mainly, we haven’t yet seen that big drop in longer-term interest rates that would have given dividend stocks a powerful lift. But neither have rates entered a 1970s-style stagflation spiral.

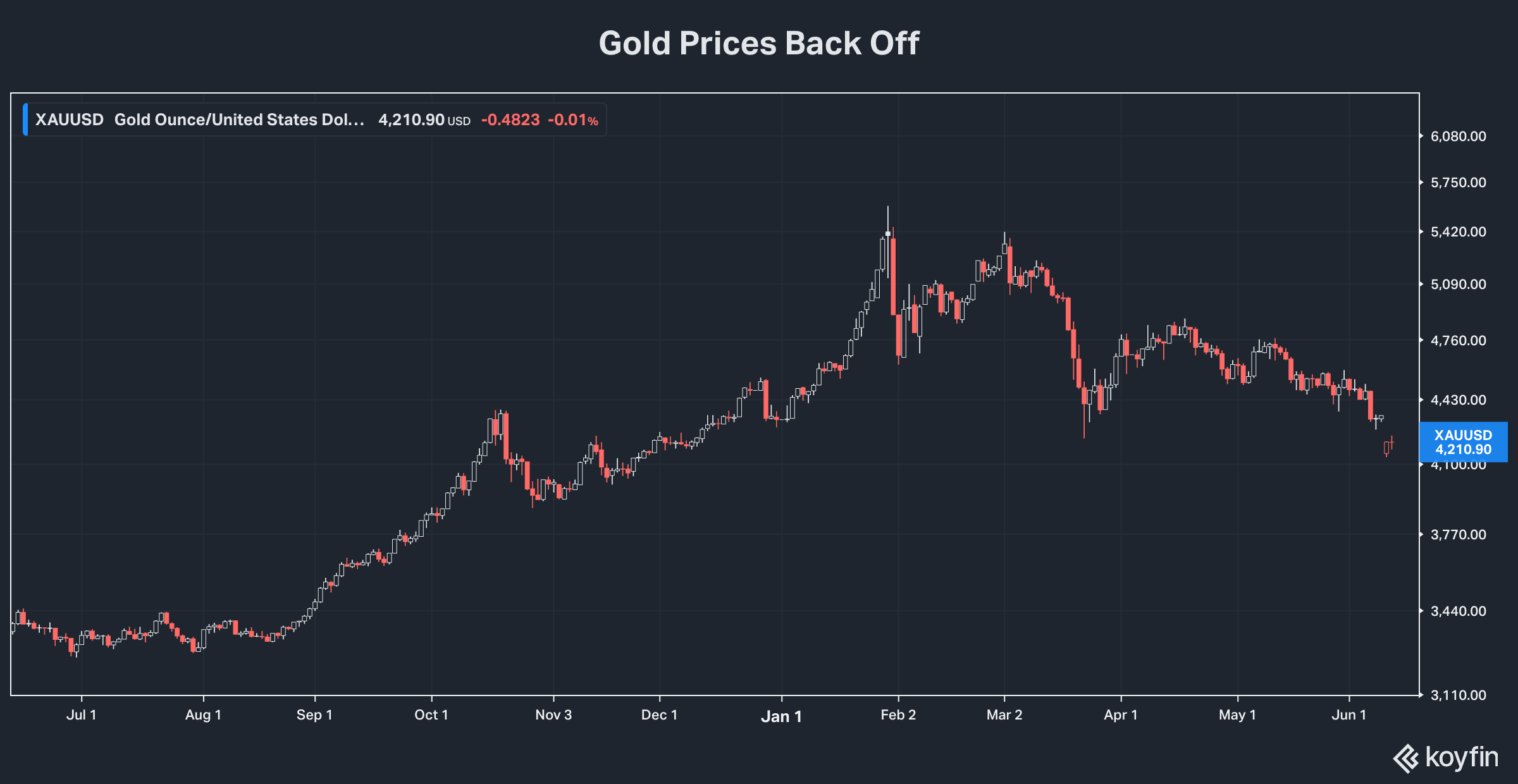

Instead, they’re holding steady. And at the same time, gold prices have backed off, with the spot price of an ounce of the yellow metal retreating to the $4,100 to $4,200 range from over $5,600 earlier this year.

That’s still about $1,500 an ounce higher than the January 2025 price. But as with the 10-year Treasury yield, this moderating action is hardly what one would expect with the onset of hyper-inflation or stagflation. Rather, it indicates a broad investor expectation that recent jumps in PPI, CPI and PCE inflation will moderate in coming months.

It’s fair to ask what happens if the center doesn’t hold, as investors seem to be assuming. And with so many are expecting a benign outcome to current market stress, we have good reason to maintain positions in gold-related investments, particularly mining stocks.

But the fact remains that despite the cataclysmic financial headlines—and the trillions of investor dollars governed by algorithms trained to respond to them—shareholder returns from dividend stocks have generally increased so far in 2026.

The only real exceptions have been companies with earnings and dividends negatively impacted by inflation. And that means they either had too much debt to manage, or they lacked pricing power.

Pricing power comes in many forms and varies across many sectors. The common element is companies sell a product or service that customers have little choice but to pay up for and therefore will absorb a price increase.

Electricity, for example, is not only more essential than ever to a functioning modern world. But regulated electric utilities are allowed to push through to customer rates the added expense of everything from higher borrowing costs to rising fuel prices and employee wages.

Earnings for producers of energy and other commodities tend to follow long-term price cycles. But in years when underlying supply is lagging demand—as is the case now with oil and copper, for example—producers can raise prices to more than compensate for the higher cost of extraction.

Real estate investment trusts operating in many property sectors are negatively affected by a supply glut. That includes most office. And even traditionally recession resistant property types like residential have seen pressure on occupancy and rents in some areas of the country.

But when supply and demand are loosely balanced—as is usually the case—real estate rents have generally kept up with inflation. And real estate property values have a strong record of reliable and robust appreciation in inflationary times.

Outside those industries, pricing power basically comes down to having some unique strength. Most often, that’s an unassailable market position for a particular product or service, or a unique niche. But it could also be a company coming off a cyclical bottom for its business and/or sector, with a recovery in progress that will continue regardless of macro factors like inflation.

It’s fair to say I hold these companies’ quarterly operating results to a higher standard than I would if they were in an industry with a clear history of maintaining pricing power in inflationary times. That is to say, I’ll cut their stocks loose faster, if the numbers and guidance indicate pricing power isn’t what it once was.

The likelihood of higher for longer inflation also makes me less attracted to most companies advertising a value proposition based on cost cutting. Expense reduction is the key selling point for a lot of M&A, for example. And it’s a popular Wall Street theme as well, with companies across a wide swath of industries touting deployment of artificial intelligence as a game changer for margins and earnings.

AI does have massive potential for efficiencies in industries that operate large systems—where faster and more effective data collection, processing and analysis can mean meaningful efficiency gains. One of those is electricity, where intelligent AI could potentially greatly improve wildfire response. Another might be communications, which is not currently represented in this portfolio.

But as far as I’m concerned, most industries’ ability to use AI to improve profitability without losing business is strictly TBD. And it’s a fair bet that for many, results are going to fall far short of the current hype.

That means—so long as higher for longer inflation is a factor in the US economy—pricing power is where we need to keep our focus when it comes to picking the right dividend stocks.

Even companies that have pricing power aren’t immune to real stock market corrections. And in my view, we’re overdue for a drop of -20% or more in the big market averages, which are currently loaded up with extremely expensive Big Tech stocks trading on price momentum.

But companies with pricing power will continue to generate solid returns in coming years. And those that lack it will be at rising risk to falling behind and at worst cutting dividends.

Building positions in dividend paying stocks of companies with pricing power is how we’ll realize this portfolio main objectives. That’s to build a rising stream of income and grow capital, while maintaining enough stability of value so investors never have to sacrifice those core objectives if they need to harvest cash.

To control near-term risk—such as from a meaningful stock market drop—I follow four basic strategy rules:

· Build and hold onto positions in companies with underlying businesses that are positioned for long-term growth and have healthy balance sheets. I sell when the business numbers tell me a company no longer offers that, even if it means taking a big loss.

· Maintain a cash reserve against the possibility of a broad correction. My favorite parking place for cash is still the Vanguard Federal Money Market (VMFXX), which currently has a 7-day SEC yield of 3.56%. It’s not the only suitable money market investment. But anything you choose should be sponsored by an organization that can protect $1 net asset value. And you should be able to access funds in a timely manner.

· Never overload on any one stock. That’s no matter how attractive a particular company looks or even if it trades below its “Dream Buy” price (see attached table), which are entry points that in the past have ensured windfall gains. Spreading your bets is the surest way to limit risk you’ll be taken down by an unexpected setback with a single company. I can guarantee if you invest for long enough, this will happen to at least one of your stocks. Diversification rather than doubling down also takes the emotion out of decision making.

· Make fresh investments in increments of two to three, rather than all in one purchase. And I will pare back positions when a stock rises far and fast enough to be out of balance with the rest of the portfolio.

Since inception, the portfolio has a total return of 106.05%, a new high-water mark. That calculation assumes harvesting rather than reinvesting dividends, which for would have produced a higher return for all 18 current holdings.

I calculate returns based on harvesting because a rising stream of current income is a key priority. Similarly, this portfolio also holds a sizeable portion of cash in part because it still provides a competitive yield. And it provides a ready source of funds for anyone who needs cash, which won’t require sacrificing future returns by selling a position prematurely.

The other reason to hold cash is it will maintain value in a market-wide selloff. And therefore, it will be a ready source of funds to buy top quality stocks that fall to good entry points.

Action Plan

Over the past month, most of the stocks in the portfolio have moved higher.