Quality Dividends Shine Through the Fog of War

Operation Epic Fury won't knock us off our game.

Editor’s Note: Thank you for reading this week’s edition of Dividends Roundtable!

The fog of war has descended on investment markets. But stocks of best-in-class companies are holding their own, as they always do in times of trouble and uncertainty. And though there are many possible outcomes from the ongoing turmoil in the Middle East, the one certainty is solid underlying businesses will be building wealth for investors on the other side.

One silver lining of what’s going on now is most portfolio stocks are back at prices where they’re worth buying, or very close to it. I’m taking advantage to add to several positions. And I’veraised buy-in targets for several others, following what were very robust calendar Q4 results and guidance updates.

Have a question? Then join my Dividends Roundtable live chat on Substack, which I host 24-7.

Here’s to your wealth!--RC

Fog of war: Confusion caused by the chaos of war or battle.

War is the realm of uncertainty. When battle begins, change is a constant and unexpected consequences are the rule. Everyone’s situational awareness is limited. You can’t see everywhere at once. The only thing that’s sure is you’re going to overlook something, and it will probably be important.

Investing in wartime boils down to two simple rules: If you’re going to move, do so deliberately. And if you’re going to buy, focus on top quality dividend stocks that will shine through the fog of war.

It’s fair to say “Operation Epic Fury” has at least so far failed to rally Americans around the flag, as previous US military actions have. The Trump Administration may have a clear ultimate objective and end game for strategic bombing in Iran. But it’s yet to communicate what it is to investors. And until/unless they do, we can only speculate how long this action will last, and how it will ultimately impact investment markets.

That hasn’t stopped investors from making some big bets on ultimate winners, keeping markets volatile. For example, the long-feared closing of the Strait of Hormuz in the Persian Gulf—and effective shut-in of energy exports from several key Middle Eastern producers—pushed oil to over $100 a barrel last week.

That’s a significant jump from the $60 to $70 range of late February. And it’s already having a widespread impact, from surging gasoline prices even in the largely self-sufficient US to providing a big advantage to chemicals companies like LyondellBasell Industries (NYSE: LYB) that rely primarily on natural gas feedstocks.

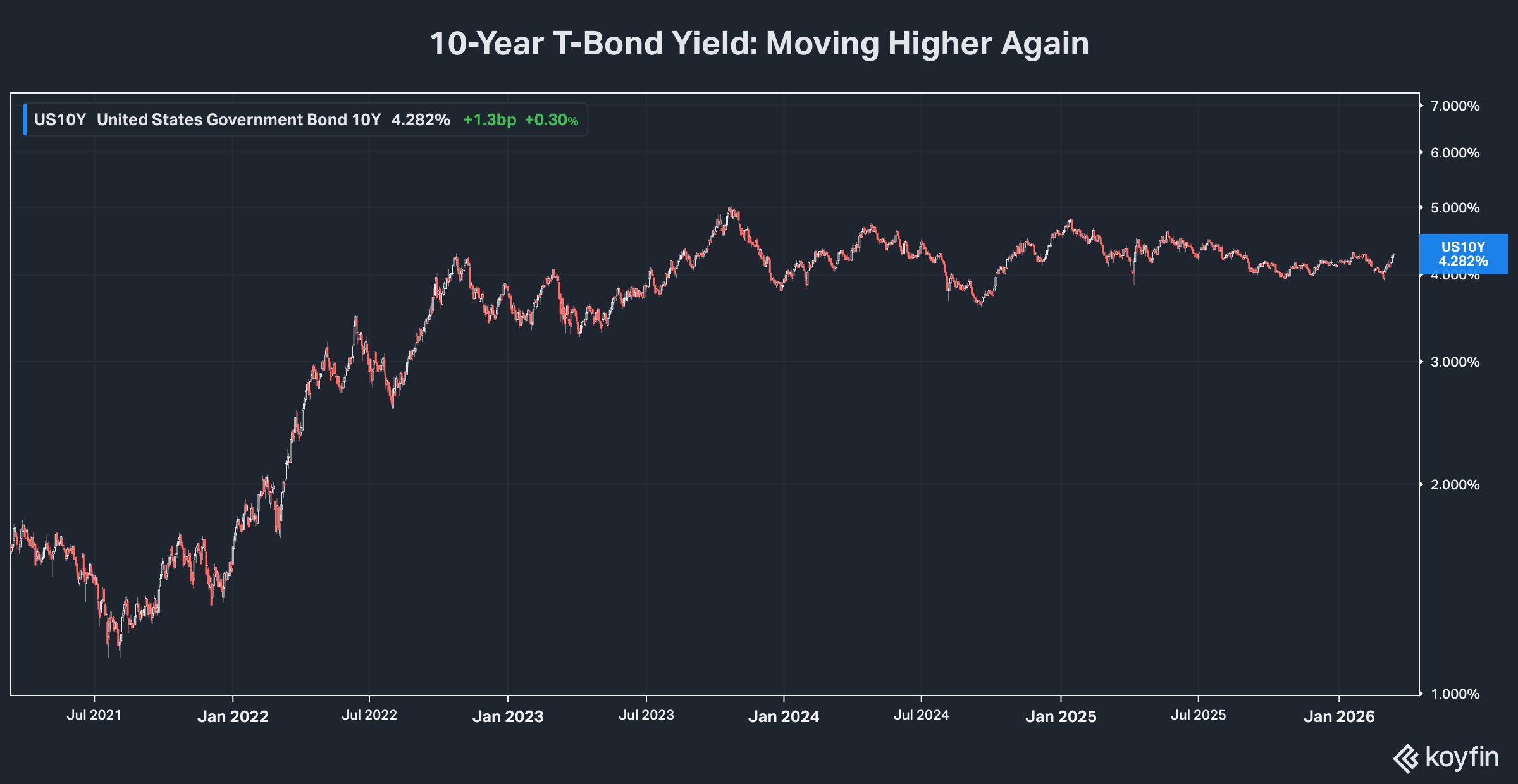

We’re also seeing a backup in long-term interest rates. The 10-year US Treasury bond yield finished last week around 4.3% after briefly dipping under 4% earlier this month.

Short-term rates have so far been less affected, with the Vanguard Federal Money Market Fund (VMFXX) still yielding 3.58%. But even before Epic Fury, companies were rolling out 2026 guidance under the implicit assumption that borrowing costs were going to stay higher for longer.

It’s a fair bet what’s happening now will only increase conservatism, especially when it comes to raising debt capital. Industrial REIT WP Carey (NYSE: WPC), for example, has issued initial investment guidance for 2026 that’s one-third less than the $2.1 billion achieved last year. Management plans to fund roughly half of that with proceeds of asset sales, the rest mainly with internally generated cash flow.

Electric utilities are not slowing CAPEX, as opportunities to serve data centers continue to increase. Dominion Energy (NYSE: D), for example, last month announced a $65 billion investment plan for the five years ending in 2030. That’s a 30% increase from what management had planned for 2025-29. And it’s part and parcel of 48.5 gigawatts of prospective incremental demand from data centers, all of which is now under some arrangement that guarantees payment to the Virginia utility.

Dominion, however, does not plan to raise its dividend this year or next. And it’s hardly the only company announcing plans to throttle back payout increases, despite strong earnings growth. The reason: Higher for longer interest rates make holding in additional cash a far better opportunity for financing, than issuing more debt.

Epic Fury and the Economy

The last report on inflation before Epic Fury showed price pressures lessening in the US after increasing in late 2025. The ongoing spike in the price of gasoline, jet fuel and related commodity and product costs may prove ephemeral if the action ends reasonably soon. If so, inflation gauges may resume falling. And borrowing costs would likely follow it down.

But so long as geopolitics is keeping interest rates elevated—or pushing them higher still—companies are going to stay conservative when it comes to dividends. And we’re also likely to see more cuts at companies where revenue is under pressure, like Lyondell’s reduction in its quarterly rate from $1.37 to 69 cents a share last month.

Will Epic Fury fallout also pressure economic growth? Food and energy prices don’t count in measures of so-called “core” inflation used by policymakers like the Federal Reserve. But when they rise, Americans do have less money to spend on other things, at least without racking up more debt.

Last week, my friend Elliott Gue posted “The Great Labor Catch Down” in his Substack “The Free Market Speculator.” A key point in his discussion of employment was the massive recent revisions in Bureau of Labor statistics data, which have undermined their ability to accurately gauge current conditions, let alone predict anything. And in any case, employment data is basically a lagging indicator, with economic weakness showing up there only after it already has elsewhere.

Epic Fury could make things worse than they are now if it further depresses investment, which is ultimately the driver of employment conditions. And the extent it does or doesn’t will also likely depend in large part on how long it lasts—and how much it increases concern about inflation and therefore borrowing costs.

There are already signs that the Gulf States may be pulling back on their global investment plans, as they cope with what they can only hope is a temporary interruption of oil and LNG export revenue. That comes at a time when private capital markets are showing some signs of strain, and most publicly traded companies’ share prices get punished when they announce meaningful equity issuance.

Sufficient turbulence would slow the pace of mergers and acquisitions globally, as private capital and sovereign wealth funds have been major players the past couple years. The consortium currently offering $15 a share in cash for AES Corp (NYSE: AES), for example, includes the Qatar Investment Authority—a country hit hard by Epic Fury fallout.

There’s an argument to be made that the Trump Administration will do a Middle East policy U-Turn, if the economic fallout in the US gets too severe in the next few weeks. November brings Mid-Term elections for Congress, 39 governors’ mansions and 88 of the nation’s 99 state legislative chambers.

Republicans are clearly on the defensive, having lost 28 state offices since November 2024 versus zero gains. That tally now includes one race following the launch of Epic Fury: A New Hampshire legislative vote that saw a 17-percentage point swing in favor of the same Democrat who ran in 2024.

Some kind of declaration of victory by the Trump Administration before moving on—regardless of whether Epic Fury succeeds or fails—still seems likely to me. But it’s a pretty flimsy rationale to base an investment strategy on in the fog of war.

What I’m Doing Now

A month ago, the average year-to-date return for this portfolio was about 14%. The return since inception in September 2018 was 98.05%, just below a high-water mark of roughly 100% reached earlier in February.

Returns continued to rise in late February and into early March. But have given back some ground since Epic Fury began. We’re now up 9% year to date and 92.52% since inception, assuming harvesting of dividends rather than reinvesting. The average weighted yield of the positions is 4.4%.

Performance this month is basically in line with what we’ve seen for the S&P 500 SPDR ETF (SPY), which is down -2.9% year to date with a dividend yield of 1.1%. And it’s in line with the iShares Dividend ETF (DVY), which is still up 6.7% so far in 2026 with a yield of 3.4%.

At this point, I’m not seeing a lot of conviction in the stock market in any direction. Big moves by a particular stock or sector on one day—up or down—are frequently reversed with a vengeance the next. And so long as so much is unknown, that’s what we can expect to continue, as some investors will continue to react to every news flash.

In times like these when so much is unknown, it helps to reflect on what our core objectives are. In this portfolio, that’s building a reliable and rising stream of income, growing principal by investing in growing businesses and minimizing overall portfolio volatility where possible. And we do it by following a simple four step strategy:

· We build and hold onto positions in companies with underlying businesses that are positioned for long-term growth and have healthy balance sheets. We sell when the business numbers tell us that’s no longer true, even if it means taking a big loss.

· We maintain a cash reserve against the possibility of a broad correction. My favorite parking place for cash is still the Vanguard Federal Money Market (VMFXX), which currently has a 7-day SEC yield of 3.58%. If you choose something else, make sure principal is protected and that you can access funds in a timely manner.

· We never overload on any one stock. That’s no matter how attractive a particular company looks or even if it trades below its “Dream Buy” price (see attached table). Spreading your bets is the surest way to limit risk you’ll be taken down by an unexpected setback with a single company.

· We make fresh investments in increments of two to three, rather than all in one purchase. And we’re willing to pare back positions when upside targets are reached, or when it makes sense from a tax perspective.

Are your primary investment objectives still to generate reliable and rising income, build portfolio value over time and limit near-term volatility? If yes, Epic Fury has changed nothing for you. And your best course is to stick with this approach.

But that doesn’t mean doing nothing in the current market.

Last month, only a handful of portfolio stocks were trading at or below my highest recommended entry points. The rest were effectively holds until further notice. Now almost everything we hold is at a price where those without positions should start building them.

That’s partly because stock prices have moved down a bit. But it’s also because more than a few companies have earned a higher entry point on the merits of positive developments, which showed up in calendar Q4 results and bullish guidance updates.

So, here’s what I’m advising this month.