REITs are Rising Again

Here's what to buy (and sell).

Biotech campus for life science R&D. By Arkelin

Editor’s Note: Thank you for reading Dividends Roundtable REITs!

Interest rates and inflation are rising again. But for the first time since the Federal Reserve started raising rates in 2022, top quality real estate investment trusts are outperforming. The Select Real Estate SPDR ETF is ahead 11.18% thus far in 2026, versus 9.64% for S&P 500 ETFs.

The First Rate REIT list is up 8.6% with an average yield of 4.7%. That compares to 3.1% for the REIT SPDR and less than 1% for the S&P 500.

Why are REITs suddenly resurgent? Give some credit to a very low bar of investor expectations after four years of underperformance, which Q1 earnings and guidance updates had no problem beating, despite numerous headwinds in come cases.

I highlight results for my 81 REIT coverage universe in this month’s edition of the REIT Rater, which is attached to this issue. I’ve launched a new feature: Quality Grades from A (most conservative) to F (riskiest). The “Commentary” column shows how each company stacks up on all five of the Quality Grade criteria.

I hope you find Quality Grades useful choosing the most suitable REITs investments. This report also highlights 5 REITs to buy and 5 to sell. And I review each of the First Rate REIT positions individually, and how they stack up following Q1 results and guidance.

Got a question or comment? Then please join the discussion at the chat I host on Substack 24-7..

To your wealth!--RC

The Federal Reserve has a new chairman, Kevin Warsh. In his contentious confirmation hearings, he promised “regime change” at the nation’s central bank, implying a bold, fresh approach from his predecessor Jerome Powell.

Investors should instead expect more of the same.

One of the biggest popular misconceptions seems to be that the Fed operates in something of a vacuum. That is, it’s the central bank’s purview to decide what borrowing costs will be. And the markets will inevitably follow.

Reality is it’s the other way around.

The voting members of the Federal Open Market Committee do directly control several things that greatly influence investment markets. That includes setting a range for the widely watched Fed Funds rate, which directly influences short-term interest rates as well as returns on “cash alternatives” like money market yields.

Under former Chairman Ben Bernanke, the Fed also built a sizeable “balance sheet” buying and selling bonds, including agency debt and mortgage-backed securities. And if executed well, buying bonds (expanding the balance sheet) and selling (contracting) can wield enormous influence on the direction and magnitude of market-based changes in interest rates.

But at the end of the day, even this enormously powerful institution must devise and follow policies that respond to what’s going on with the economy and investment markets. And right now, that’s persistently rising inflation, as cost increases from global supply chain disruption—including a Middle East war now in its 13th week—are absorbed by some combination of businesses and consumers.

The Fed could theoretically cut Fed Funds as the president has made no secret he desires. And doing so could push shorter-term interest rates lower at least in the near-term.

But anything that smacks of going soft on inflation is likely have the opposite impact on longer-term interest rates and borrowing costs. And that reality showed up last week in market expectations, with investors assigning a 50% probability the Fed will raise rather than lower Fed Funds this summer.

A Fed Funds rate boost wouldn’t immediately or directly offset inflation pressure in economy. But it would almost certainly boost investor confidence that the central bank under Chairman Warsh is still serious about fighting inflation, regardless of politicians’ wants and approaching November mid-term elections. And that could have a powerful positive impact on values of investments now deemed at most risk to inflation and even higher for longer interest rates.

That includes real estate investment trusts. One of the most important takeaways from sector Q1 results and guidance updates is at least the better run REITs are learning to live with borrowing costs that are close to twice what they paid at the beginning of the decade, as by extension most debt maturing this year and last.

My expanded Commentary—which now includes point-by-point coverage of my five criteria Quality Grade system—highlights 12-month changes in debt interest expense. And a quick scan will reveal most REITs are still seeing this cost rising at double-digit rates. The main exceptions are companies deliberately slashing their debt by some combination of asset sales and throttling back on dividends.

Rising interest expense has a direct impact on cash flow needed to pay dividends. It’s the primary reason for the dividend cuts in this sector over the past 2-3 years. And another surge in borrowing costs is the greatest risk to payouts going forward.

Higher interest rates also raise the bar for investment. Mainly, prospective returns for a new development or acquisition must rise to at least keep pace, or else the money will be better spent slashing debt, buying back stock and/or paying a higher dividend.

There are a number of REITs on the First Rate REITs list that have already raised investment targets for 2026, which in turn has enabled them to raise FFO guidance. But at least so far, these boosts are basically bringing expected investments back into line with what they did in 2025.

The abysmal conditions management was preparing for haven’t appeared, at least not yet. As a result, these REITs are handily beating a very low bar of projections baked into their guidance. And they’re topping investor expectations as well, resulting in solid returns so far this year.

Upside Drivers in Stressful Times

Outperforming tepid expectations is pretty much the theme for REITs so far this year. The sector continues to face headwinds from multiple directions.

Higher interest rates and share prices that are heavily discounted to private capital values have kept cost of capital meaningfully higher than in previous years. Past years’ overbuilding has kept supply elevated in many regions across sectors, even including traditionally recession resilient sectors like residential and self-storage. Office is still trying to find a post-2020 pandemic bottom. Hospital chains are still cash strapped and threatening leases and rents for REIT owners.

Financial REITs are now facing double trouble from a combination of volatile interest rates and commercial real estate credit concerns. And now those that have diversified into residential mortgages face a growing risk of default from floating rate mortgages.

It’s a perilous environment. And the five large REIT dividend cuts already this year is a testament that not every company is responding well.

But equally, these weak conditions are a known element—both for the REITs and investors. And investors in the companies that can stay resilient are going to continue to see strong returns.

That’s even if interest rates stay higher for longer. And if the Federal Reserve can do what’s needed to boost investor confidence that inflation will be brought under control, REITs will get a huge boost in both earnings and share prices from a return to lower rates.

A drop in borrowing costs is still the single biggest potential upside catalyst for REITs in the remainder of 2026. And the barometer to keep an eye on is still the 10-year Treasury note yield, shown in the graph.

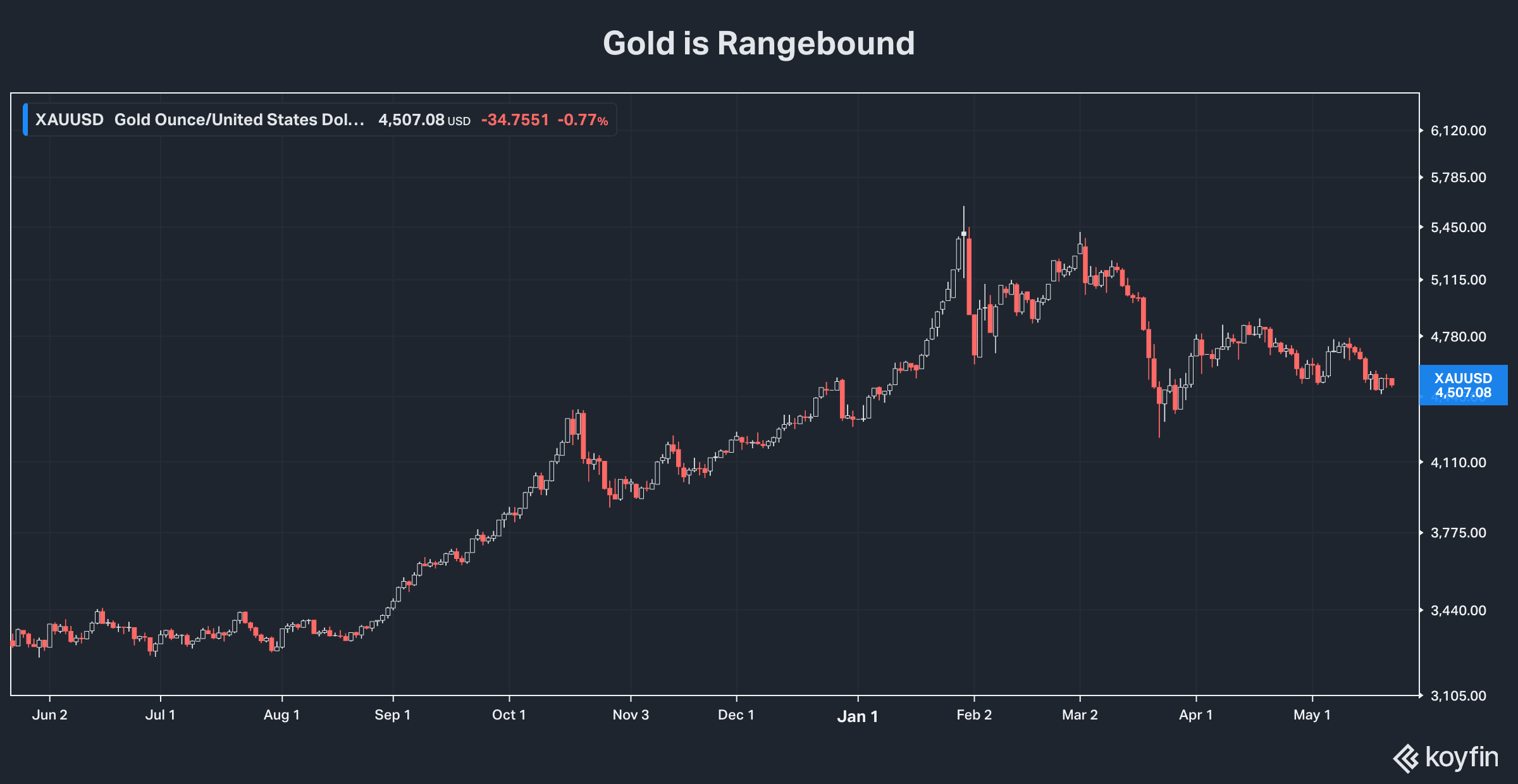

The spike in official inflation over the past month combined with concerns it could go higher pushed up the 10-year yield over 4.6% for a while last week. But it’s important to note we haven’t yet seen a breakout from the range of the past few years. And at the same time, gold prices have backed off a bit as well to around $4,500 an ounce, after spiking briefly to a point around $1,000 higher earlier this year.

To me, that still indicates an expectation from investors that inflation may remain higher for longer but that it will ultimately be brought under control. An outbreak of peace in the Middle East remains a potential catalyst for bonds to rally and yields to drop.

Even if rates go a bit higher, REITs should still benefit from the closing of the gap with private capital property values is another. The research firm Private Equity Real Estate still puts publicly traded REITs at a “median” discount north of 15% to net asset value, based on the appraised value of their properties. And some properties such as office are at especially wide ones that in the past have always closed over time.

REITs also remain historically unrepresented in S&P 500 ETFs that now dominate most Americans’ portfolios. And restoring them to a more historically normal 5-6% will bring significant buying power the next few years.

Real property remains one of the biggest long-term beneficiaries of inflation. Will Rogers once said famously, “go for the land. They ain’t making any more of it.” Generations of Americans have left real wealth to their heirs through property for decades. And like all hard assets, values will continue to rise.

Last but not least is superior yield. The average for the 81 in the REIT Rater is 5.59%. And dividends are well-covered by earnings—specifically funds from operations (FFO) and funds available for distribution (FAD). The average FFO payout ratio is just 71.8% based on most current available information. And more than half the First Rate REITs so far in 2026 have raised dividends this year,

The coverage universe has averaged a -0.26% change in dividends this year. That follows a -36% dividend cut by Chiron Real Estate (NYSE: XRN)—formerly Global Medical—which also withdrew 2026 guidance. Management’s statement is the saved cash will “facilitate growth plans.” But Q1 FFO was lower on reduced occupancy as the medical industry continues to struggle with rents.

The good news is the reduced rate should be covered with FFO even under very conservative assumptions. But Chiron’s cut is a continuing demonstration that REIT dividend growth remains restrained, even for the stronger players. And while most payouts are better protected from a downturn, especially after five years of sector-wide cost cutting, debt reduction and “high grading” of property portfolios, there’s still considerable risk.

New Feature: Quality Grades

To better manage this period of greater risk/reward in the REIT sector, I’ve added a new feature to REIT Rater coverage. That’s my five-letter “Quality Grade” system, based on these five criteria:

· Dividend policy sustainability.

· Revenue reliability.

· Regulatory/legal risks.

· Balance sheet strength.

· Operating efficiency.

I’ve used this basic five-part system for dividend stocks for several decades, utilities in particular. It doesn’t guarantee we’ll respond to every danger. And it’s only as effective as the data I feed into it. But it does provide a pretty good framework for understanding companies’ strengths and weaknesses.

One thing I’ve found is this quintet is self-reinforcing. A company with reliable revenue in all economic environments, for example, will have a strong balance sheet and a sustainable dividend. And conversely, a REIT that’s run inefficiently will have a tough time holding down debt and/or maintaining a reliable payout.

The Quality Grade system replaces the old “Conservative,” “Aggressive” and “Speculative column. But a shorthand way to convert is that “A” is Conservative, “B” and “C” are basically Aggressive and “D” or “F” are Speculative at best.

Again this is an especially important time to keep an eye on risk. Mainly, there’s no shortage of REITs with high yields and low prices relative to earnings and business value. And the long-term drivers for a sector boom are in place.

The Quality Grade system is a straightforward way to assess the risks relative to potential upside. And I’ll be using it in conjunction with my four piece overall strategy for building positions in cheap REITs and controlling risk remains the same:

· Sell any REIT where the underlying businesses is weakening. Q1 earnings releases and guidance updates have given us a golden opportunity to assess those risks, along with balance sheet health and investment/dividend policy sustainability.

· Do not chase REITs above my highest recommended entry points. And take new positions in increments of three, rather than all at once—even if stocks are at Dream Buy prices.

· Take profits in big winners when they trade above profit taking prices in the REIT Rater table included with this issue.

· Never load up on any one REIT. Always balance and diversify positions.

Top 5 Fresh Money Buys and Sells

So what am I advising now in the REIT universe—based on Q1 results, management’s guidance updates and my enhanced Quality Grades system?

My chief concern going into Q1 earnings reporting season was how higher for longer interest rates have affected investment plans and dividend sustainability. And what we saw was pretty much a mixed bag.

The good news is the First Rate REITs may not be loving inflation. But they are certainly learning to live with it. And that was my line in the sand for keeping them on that buy list as ripe for building new positions.

In all, 11 of them raised 2026 after just one quarter of results. That’s the best possible confirmation of their underlying health and ability to grow amid the challenging conditions in the property sector. And it’s why we want to continue to hold them.

IWhen a REIT does cut guidance, I need it to have a very good explanation why to give me a comfort level that it won’t do so again. This one did that and I’m going to stick with it.

The five fresh money buys below all raised their guidance following solid Q1 results. The “Commentary” column in the REIT Rater has quite a bit of information. And I recap the highlights briefly in the discussion below. They are: