The S&P 500 Is Really the S&P 7

REITs paying 6% are an antidote. Here are five to buy.

Editor’s Note: Thank you for reading Dividends Roundtable REITs.

At 30X earnings, 35% concentrated in 7 AI stocks completely unmoored from business value with daily trading dominated by algorithms trained to respond to headlines: That sums up the S&P 500 and related ETFs that comprise most Americans’ stock portfolios. And market history is clear this won’t end well.

REITs are an antidote. Real property stocks’ current weighing in the S&P 500 is insignificant, effectively de-coupling them from the index. And the sector has started to outperform: Year-to-date, the Real Estate SPDR ETF (XLRE) is up 9.3% and my First Rate REITs are up 6.5%, versus the S&P 500 SPDR ETF (SPY) at 4.98%.

REITs are also still cheap relative both to other stocks and private capital property portfolios. And the average yield for the 81 REITs I track in the REIT Rater is 5.88%, almost six times the S&P 500 yield and competitive with higher quality bond funds.

There are risks, particularly to dividends as borrowing costs stay higher for longer. But best in class REITs are learning to thrive despite that headwind, as demonstrated by Prologis Inc’s (NYSE: PLD) guidance boost earlier this month.

The industrial REIT is one of my five “Best Fresh Money Buys” this month. I feature the investment case for this quintet later in this report, along with five REITs worth taking advantage of current prices to sell.

Got a question? Join the discussion at my live chat on the Substack application, which I host 24-7. Join in and start a thread!

To your wealth!--RC

What does the Strait of Hormuz have to do with real property values in the US? In the long run, not much.

But trillions of the passively invested dollars in stocks are controlled by algorithms trained to respond to headlines. And with those changing intraday on Persian Gulf developments, even REITs are getting caught up in Wall Street’s alternating risk-on/risk-off betting war.

At some point, most passive investors will realize handing off their money to an algo-managed S&P 500 fund sponsored by Mega Corp will always leave them wanting. But until then, we have a compelling investment opportunity to “fade” the algos—building positions in the high-quality stocks headline chasers are selling and taking profits on what’s been bid up.

REITs are a sector with more than its share of bargains these days. The 81 I track in my REIT Rater table cover quite a bit more territory than your grandfather’s traditional sectors like apartments, office and retail.

What “new” sectors like self-storage, data centers and the like have in common with the “old” is they generate steady income from rents. And under the REIT structure, they can distribute that income to shareholders tax-efficiently, which results in high and tax-exempt yields.

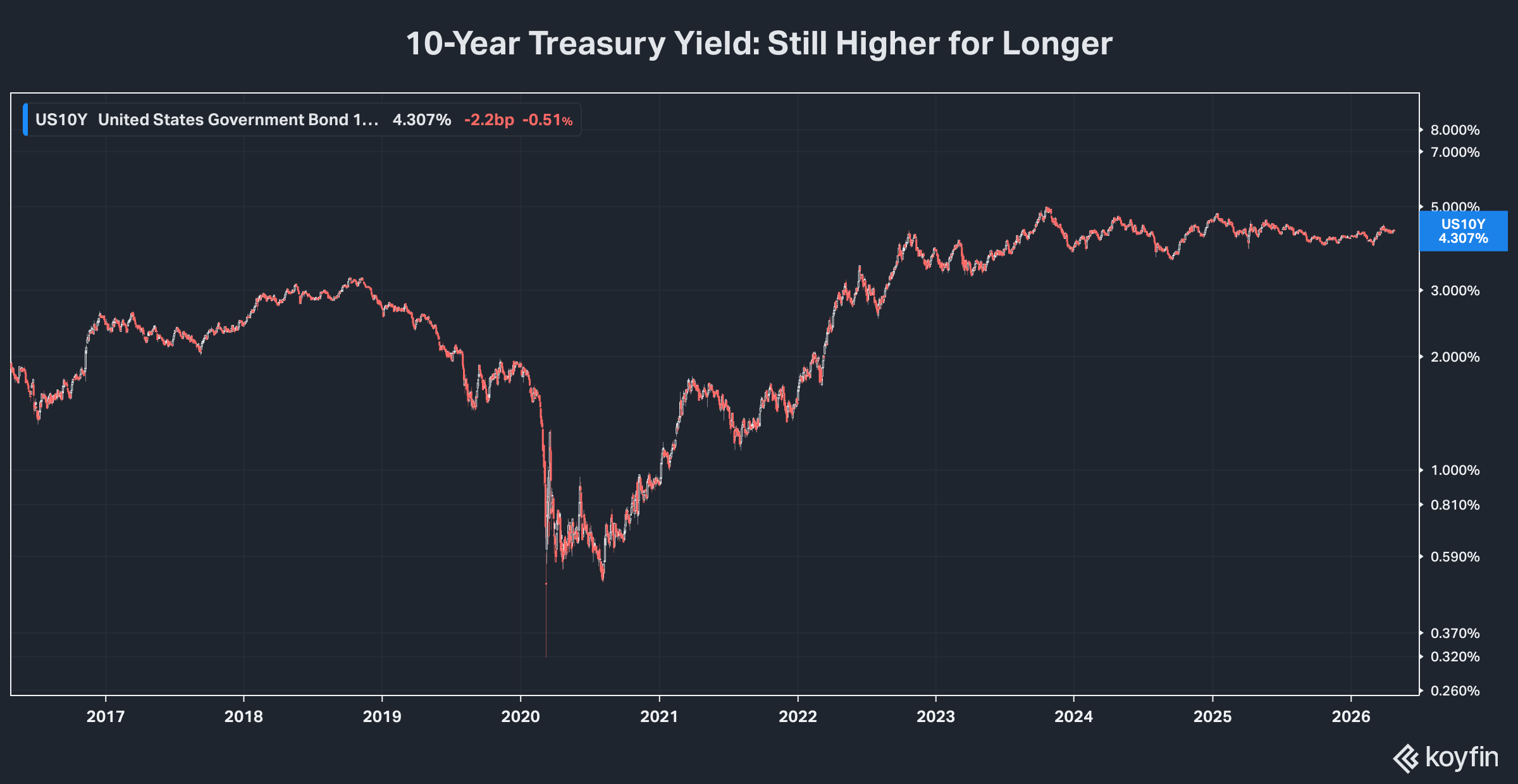

Why are REITs cheap now? For one thing, many of them have basically been left out of the stock market’s upward push since 2022, when the Federal Reserve began raising the Fed Funds rate.

The sector caught its breath a couple years after that, when the Fed pivoted to cutting rates. But it came under pressure again last year as disrupted supply chains began to push up inflation. And despite outperforming year-to-date, REIT yields are the highest and valuations the lowest in many years.

The average yield for the 81 in the REIT Rater is nearly 6%. And dividends are well-covered by earnings—specifically funds from operations (FFO) and funds available for distribution (FAD). The average FFO payout ratio is just 69.9% based on most current available information.

More than half the First Rate REITs so far in 2026 have raised dividends this year, with the coverage universe increasing 0.2%. That’s a more restrained rate of growth than in past years. But it also means companies’ payouts are better protected in case there is a downturn, especially after five years of sector-wide cost cutting, debt reduction and “high grading” of property portfolios.

As I pointed out last month, REITs are still trading at a discount to privately held property. According to Private Equity Real Estate, publicly traded REITs are trading at a “median” discount of 15% to 19.3% below net asset value, based on the appraised value of their properties.

That’s a massive discount. There is a meaningful variance between sectors, with out-of-favor sectors like office properties selling for much bigger discounts than relatively in-favor senior housing (SHOP). But in the past, such wide discounts have narrowed, providing a big boost to REITs. And in the meantime, REITs effectively provide investors the opportunity to buy properties at substantial discounts to market value. That’s solid downside protection in case property values do decline.

In my view, one of the biggest attractions of REITs now is the fact they’re historically under-represented in the S&P 500 index at less than 2%, and therefore related ETFs and close cousins. And with more money passively invested in stocks than actively managed that means REITs are historically under-owned by investors as well.

The largest by weighting—Welltower Inc (NYSE: WELL)—actually saw its weighting shrink last month to 0.24% from 0.25% of the index. That means REITs’ longer-term returns are effectively decoupled from S&P 500 performance.

That won’t prevent REITs from taking on water in a real bear market. The last one of those we had was back in 2007-09. And even regulated monopoly utilities took on water then, despite the fact they were able to increase dividends while banks were failing.

REITs that stumble have no assurance they’ll get back up. But top-quality property companies that have protected balance sheets and focused on quality expansion are among the more reliable ports in market wide storms. And they’ll also be among the first to recover at the bottom.

In any case, when REITs have traded at such low weightings and high yields in the past, they’ve rallied strongly the next several years. And there’s every reason to expect the same this time around.

What are the best REITs to buy now?

Every issue, I feature five top-quality REITs trading at attractive prices to start building positions in now. And I highlight a quintet that’s especially ripe for taking some money off the table.

The REIT Rater table is a complete databank for all 81 real estate investment trusts in the broader coverage universe. There’s a full description of what’s provided there in the section at the end of this report.

This month’s “Commentary” has earnings analysis for the 11 REITs that have reported Q1 results and updated guidance to date. I use five basic criteria to determine the “Risk Level” of every REIT:

· Dividend policy sustainability.

· Revenue reliability.

· Regulatory/legal risks.

· Balance sheet strength.

· Operating efficiency.

This quintet is self-reinforcing. A company with reliable revenue in all economic environments, for example, will have a strong balance sheet and a sustainable dividend. And conversely, a REIT that’s run inefficiently will have a tough time holding down debt and/or maintaining a reliable payout.

This is an especially important time to keep an eye on risk. Mainly, there’s no shortage of REITs with high yields and low prices relative to earnings and business value. And the long-term drivers for a sector boom are in place.

Since interest rates began rising in 2022, new builds have fallen off a cliff in multiple sectors, from office properties to residential and self-storage. New supply is still depressing rent growth and occupancy in some sectors, SunBelt apartments and life science campuses being two good examples.

Combined with elevated borrowing costs, that continues to depress new development. And that means very little new supply is set to come on stream for 2027 and later, setting the stage for eventual outright shortages of multiple property types across several regions.

Real estate is also one of a handful of asset classes that tends to perform well in times of elevated inflation. The fog of war has descended on economic data, with the Federal Reserve putting Fed Funds rate changes on hold for the time being. But inflation does appear to be on the rise, with the central bank’s preferred measure running well over 3% versus a target of 2%.

For his part, President Trump continues to pressure the Fed to cut interest rates anyway. This week, Congress held a hearing on Kevin Warsh, his nominee to replace Jerome Powell as Fed Chairman when his term ends in May. Warsh issued a call for “regime change” at the Fed, pledging again to dramatically shrink the central bank’s balance sheet with asset sales.

Warsh’s nomination has been held up in committee by Senator Thom Tillis (R-NC). That may end soon now that the Trump Administration has dropped its criminal probe of Powell over alleged mismanagement of building renovations.

But assuming he does ultimately win confirmation, Warsh’s most important challenge is going to be convincing investors of his independence from politicians. To the extent he does, the currently hot inflation expectations will diminish and borrowing costs may finally start to fall. If he doesn’t, we could see borrowing costs go even higher.

The risk inflation expectations start climbing again is a good reason to own gold stocks, despite their gains of the past year. And it’s a great reason to build positions in selected REITs, provided they can continue to fund growth and dividends at higher interest rates.

Higher Borrowing Costs = Risk to REIT Dividends

Not all of them can. Since mid-2025, we’ve seen several REITs retrench, cutting dividend to hold in more cash. So doing, they’ve shored up balance sheets by increasing their ability to self-fund investment in growth, without turning to capital markets. But their stocks have also taken hits. And arguably, they’ve suffered reputational damage with investors, which may keep their shares depressed for some time.

The REIT Rater shows year-to-date dividend changes for all 81 companies I currently track. So far in 2026, there have been four cuts: Alexandria REIT (NYSE: ARE), Allied Properties (TSX: AP-U, OTC: APYRF), Franklin BSP Realty Trust (NYSE: FBRT) and SL Green Realty (NYSE: SLG).

Alexandria, Allied and SL Green are all owners of office properties. Franklin specializes in collateralized, floating rate mortgages. Both sectors’ REITs have been under earnings pressure the past few years. And most are underwater year-to-date, with shareholders of the now bankrupt and no longer tracked Office Properties Income Trust (OTC: OPITQ) completely wiped out.

So far, SL Green is the only one of the four dividend cutters—as well as the only major office REIT—to report Q1 results. And while the New York City REIT now pays a dividend just 23% of the pre-pandemic rate, there are signs of a return to growth, the fruits of a major strategic overhaul that cut debt and expenses and boosted portfolio quality.

That’s a formula the best in class will repeat. That’s even as the less adept continue to fall by the wayside like Office Properties Income has. And a solid assessment of risks of each REIT is the key difference maker for investors.

Multifamily residential or apartment real estate is another REIT sector coming under intense selling pressure this year.

My candidate for least useful stock market indicator is still the 12-month price projections issued by major investment banks. The changes in the average target price set by the analysts covering companies invariably follow the actual share price action, rather than forecast it. So, increases basically amount to getting on the bandwagon, while decreases are simply piling onto what’s already happened.

Nonetheless, changes in target prices do still influence buying and selling. So when a sector comes under selling pressure, analysts’ target price cuts tend to beget more selling.

That’s what’s happened in the residential property sector since the second half of 2025. And the result is apartment REITs that have consistently raised dividends even during the pandemic year like AvalonBay (NYSE: AVB) are underwater this year, even as popular sector ETFs like the Real Estate SPDR are still in the black.

Residential REITs’ own guidance has played into the bearish narrative, with even the strongest companies in the sector forecasting relatively flat occupancy and rent growth. And many have fed it further by restraining dividend growth to hold in more cash.

Given the pressures on the broad economy this year including uncertain inflation, it’s likely 2026 will be another trough year for at least some residential REITs, tacking onto what was a largely lackluster 2025. And the longer there’s pressure on rents and net operating income, the greater the risk we could see a residential REIT cut its dividend.

We are also seeing some REITs leaving the residential property sector. The former Amerada Hoffler has changed its name to AH Realty Trust (NYSE: AHRT) and has now either sold or has agreements in place to divest 13 of the 14 residential properties it owned last year.

The former Washington REIT, now Elme Communities (NYSE: ELME), expects to completely divest its remaining assets by the end of Q2, all residential properties. And apartment REIT Centerspace (NYSE: CSR) has shaken up its Board during a strategic review management has said could end in the sale of the company.

Starting next week, we’ll get a better read on how leading residential REITs are stacking up in the current environment. Like the office REITs, the best in class are cheap. But neither are they regulated utilities. Some that stumble this year may not get back up. And while the sector holds great promise, we also need to navigate the risks.

My overall strategy for building positions in cheap REITs and controlling risk remains the same:

· Sell any REIT where the underlying businesses is weakening. Q1 earnings releases and guidance updates are the ideal time to assess those risks, along with balance sheet health and investment/dividend policy sustainability.

· Do not chase REITs above my highest recommended entry points. And take new positions in increments of three, rather than all at once—even if stocks are at Dream Buy prices.

· Take profits in big winners when they trade above profit taking prices in the REIT Rater table included with this issue.

· Never load up on any one REIT. Always balance and diversify positions.

In contrast to residential and office, other REIT sectors have managed to maintain upside momentum so far in 2026.

Last year, industrial and logistics property REITs were under selling pressure, as investors worried about potential oversupply at a time when global trade being affected by supply chain disruption. Now the group is back in favor, as it’s clear their major clients need the services they provide more than ever.

Seniors housing continues to enjoy a surge in occupancy and rents, powering REITs’ net operating income. The reputational damage from the pandemic has proven short-lived and demand is surging at a time when larger players with scale are ramping up market share.

Data center REIT shares have spiked up since Operation Epic Fury scrambled global energy markets. US-based facilities especially have gained an advantage over global competitors thanks to access to cheap local natural gas for generating electricity. And the group seems to be getting more traction from the fact that major US tech companies are pushing their AI energy advantage.

Finally, retail REITs are getting some recognition from investors that their sector is far stronger than it was in 2019-20, the last time the US economy weakened. Much greater scale and rapid debt reduction are two reasons. But still-climbing occupancy rates—despite some notable retail failures—are an unmistakable sign that top quality sites are currently in high demand.

There are bargains in each of these sectors. But investors do face a growing challenge in that many of the leaders now pay yields that resemble technology stocks with far different business and growth profiles. They’re now effectively momentum stocks, rather than income investments.

That doesn’t mean they can’t go higher in coming months. But it doesn’t make any sense for long-term investors to build positions, even if dividends aren’t your first priority. And unless you’re prepared to wake up tomorrow seeing them down -20% or more, it makes sense to take some money off the table by selling at least some of your shares.

Top 5 Fresh Money Buys and Sells

So what am I advising now?