Cheap REITs, Dangerous Markets

Epic Fury wiped out the sector's 2026 gains. Here's how to buy without getting trapped.

money (3204689360).jpg")

Editor’s Note: Thank you for reading Dividends Roundtable REITs.

Fallout from Operation Epic Fury continues to scramble investment markets. And top-quality real estate investment trusts—despite being historically undervalued and under-owned—have taken meaningful hits this month.

Lower prices mean better bargains. But if what’s happening now does lead to further stock market downside, it’s likely what’s cheap now will get cheaper still. And REITs are not regulated utilities: There can never be a guarantee what goes down will ultimately rise again.

How to scoop up bargains without getting burned? That’s what this month’s report is all about. And I’m introducing a new feature—“Five Best Fresh Money Buys and Sells”—which you’ll find following my market analysis and strategy.

Got a question? Join the discussion at my Dividends Roundtable Substack webchat. I host it 24-7 on the Substack application.

To your wealth!--RC

It’s been only five weeks since my last report on real estate investment trusts. But that’s been plenty of time for the ground to shift under investors’ feet.

The primary catalyst is continuing fallout from Operation Epic Fury. And as is always the case when war breaks out in the Middle East, energy prices are ground zero.

The Brent price of a barrel of oil is now nearly twice where it began the year. At Friday’s close, North American natural gas prices had dropped with seasonal weakness to around $3 per million BTU. But with Qatar declaring force majeure on LNG contracts, global gas prices are tracking oil higher as buyers in Asia and Europe scramble for alternative supplies.

Even in the energy self-sufficient US, gasoline prices have surged. And with at least 17% of Qatari LNG production facilities destroyed, it’s likely global oil and gas supply disruption will continue even when the bombs stop falling and the Strait of Hormuz opens again to shipping.

Energy prices along with food are not included in measures of so-called “core” inflation. But they do affect real estate.

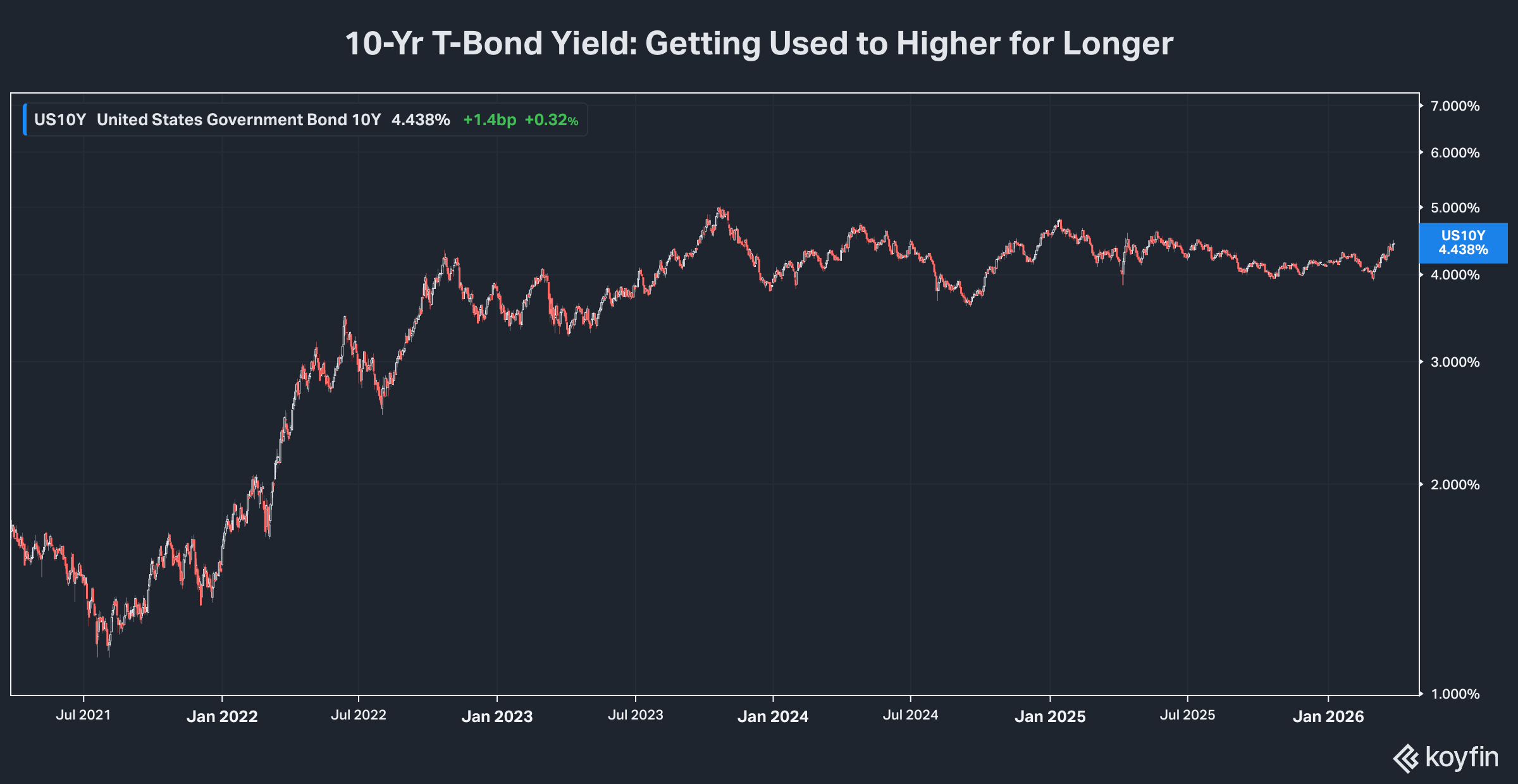

That starts with interest rates. Before Epic Fury, the 10-year Treasury note yield appeared to at last be breaking below 4%. Friday, it spiked up to close around 4.5%. Mortgage rates have followed the benchmark rate higher, with their fastest three-week climb since second half 2024 according to Freddie Mac data.

REITs in general have been pulling back on debt issuance the past several years, adjusting to higher for longer rates. And what bond sales we’ve seen have been primarily on the shorter end of the maturity spectrum, where borrowing rates have generally remained lower.

Just after Epic Fury began, for example, data center REIT Equinix Inc (NSDQ: EQIX) sold $1.5 billion of bonds. That included $700 million due 2031 with a coupon interest rate of 4.4% and $800 million maturing in 2033 at a rate of 4.7%.

Equinix is among the highest rated REITs. Both Fitch and S&P rate the REIT BBB+ with a stable rating. And earlier this month, Moody’s lifted it to Baa1 with a stable outlook, citing the company’s “established position in the global digital infrastructure market.”

Rates that low aren’t available to most. Just before Epic Fury, BBB- rated Gaming and Leisure Properties (NYSE: GLPI) issued $800 million of bonds due 2036 at a coupon interest rate of 5.625%. A week after Equinix’ bond sale, BB-rated Ryman Hospitality Properties (NYSE: RHP) sold $700 mil notes due 2034 at coupon interest rate of 5.75%.

Lower Debt Equals Less Risk

Both REITs would have paid considerably more had they waited longer to sell. Going forward, some companies won’t have any choice but to take what the market will give them. But those with the flexibility to pull back on investment, offset the cost with asset sale proceeds and/or partner with private capital will do that instead of issuing bonds.

That’s clearly the direction most are taking. All 80 REITs in the REIT Rater databank have now at last reported Q4 results and updated 2026 guidance. My analysis of the results is in the attached table, along with updates for REITs reporting earlier.

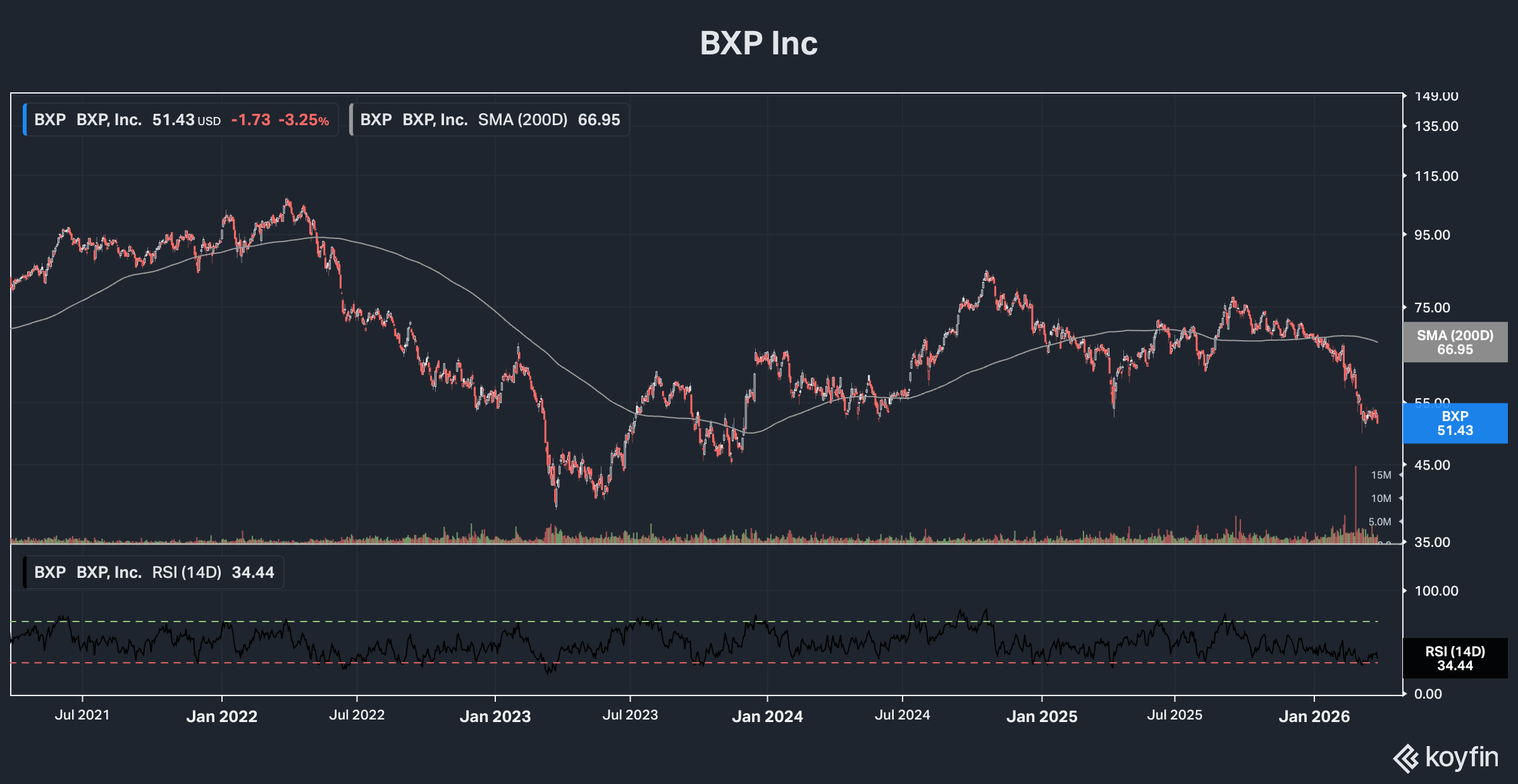

BXP Inc (NYSE: BXP), for example, reported on the progress of its multi-year strategic plan earlier this month at its annual “Investor Day.” Highlights included an update of its target of $1.9 billion in proceeds from “strategic sales of raw land, residential and “non-strategic office assets.” The REIT now forecasts it will have completed $1.25 billion of that in 2026. That compares to one acquisition announced so far this year of $55 million.

Focus on cost containment and debt reduction are a huge plus for BXP’s ability to meet its 2026 FFO guidance of $6.88 to $7.04 per share. That’s even if its target of being 91% leased by end-year falls short. Management’s leased target by the end of 2027 is 93%.

Realty Income (NYSE: O) is leaning on its strategic partnership with private capital firm Apollo to help fund its $8 billion investment program for 2026. Apollo’s initial $1 billion investment will buy it a 49% ownership interest in the partnership, with the REIT contributing 500 retail assets.

Realty Income will own the other 51% and continue to operate the assets under a long-term management contract. The REIT also retains the right to buy out Apollo’s interest “after year 7 and through year 15 of the joint venture” at “a future call price calculated to ensure a capped internal rate of return (IRR) of 6.875%.” But the expectation now is this will be an entity both partners will continue to invest in, pooling resources to accelerate growth at a time of higher for longer interest rates.

Will it succeed? In the past few weeks, there have been reports that over $100 billion in private capital firm assets are experiencing some form of financial stress. And at least one fund investing in real estate has suspended making redemptions.

That’s hardly surprising when you consider this more lightly regulated financial sector has up to now been enjoying a much lower cost of capital than rivals. That includes REITs, which have been challenged to issue new debt and equity at economic rates since the Fed began raising interest rates in early 2022.

Most recent National REIT Association (NaREIT) data reveal a “valuation gap” between public (REITs) and privately owned real estate since the Federal Reserve of around 130 basis points, based on capitalization or “cap rates.”

Cap rates are a shorthand measure of the rate of return on commercial investment property. The simple calculation is to divide net operating income—basically rents and other revenue after subtracting out operating costs—by the current market value of the property.

As I pointed out last month, elevated spreads have usually been followed by several years of REIT outperformance in the stock market. But what if the spread narrows by a private capital implosion, also triggered by a sudden rise in the cost of capital at a time of over confidence and over-leveraging?

New at REIT Rater

Last month, I highlighted the fact that REIT sector stocks were still cheap on a relative and absolute basis, even after a solid start to the year. That’s even more the case now, with Epic Fury fallout wiping out the sector’s year-to-date gains and then some.

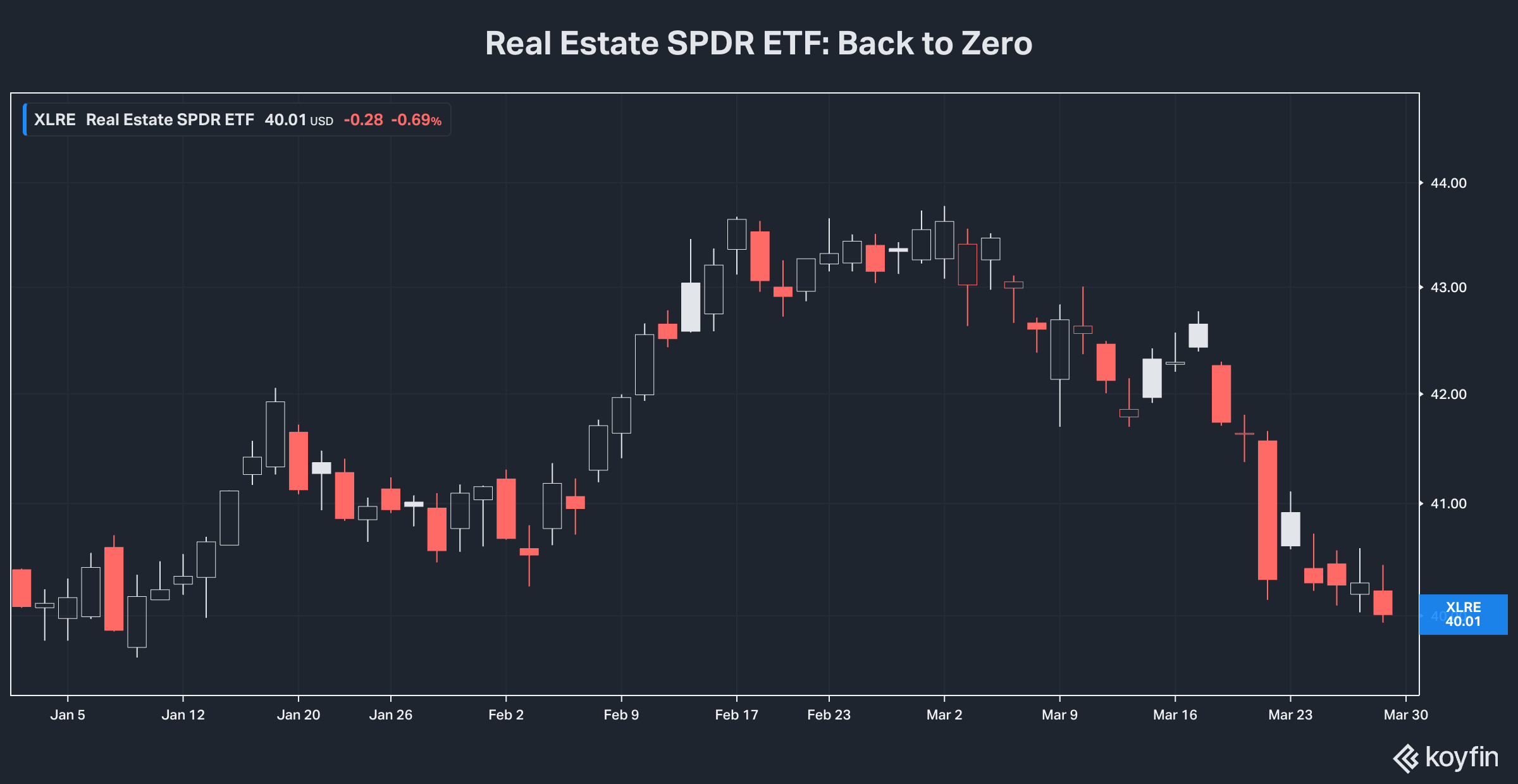

The REIT SPDR ETF (XLRE) is now underwater for 2026 including dividends paid. The First Rate REITs have gone from a 7.6% gain to a barely breakeven 0.1%. And the full REIT Rater coverage universe of 80 REITs is down -2.2%.

I’ve initiated two new columns in the REIT Rater table: Year-To-Date Total Return and Year-To-Date Dividend Growth.

The link to the table follows my newly launched “Top 5 Fresh Money Buys and Sells” feature.

Looking down the list, there are still a handful of meaningful winners this year. The biggest is National Storage Affiliates (NYSE: NSA), which received a high premium takeover offer from larger rival Public Storage (NYSE: PSA) in mid-March.

Most REITs, however, have given up the bulk of this year’s gains. And many are now in the red, some substantially.

As for dividend growth, there’s one notable standout: Farmland Partners (NYSE: FPI) boosted its payout by 50% for shareholders of record April 1. Five others raised payouts by at least 10%. And nine more managed a mid-to-upper single digit percentage boost.

Most REITs, however, throttled back on increases, including almost every residential property owner. And we’ve already seen some sizeable cuts, especially in the office sector. The latest of these was at prime New York City building operator SL Green (NYSE: SLG), which has gone to a quarterly rate that’s about -20% below the previous level.

Headwinds and Tailwinds

During the most recent round of REIT guidance calls, more than one executive commented that properties were healthy but that higher for longer interest rates were squeezing margins and ability to grow. That was the primary reason for quite conservative guidance for 2026. And Epic Fury fallout seems likely to trigger even more retrenchment when Q1 reporting season begins in mid-April.

So what’s the big picture here for REIT investors, five weeks into Epic Fury fallout?

First, there are still some substantial positives. Following the selloff and the latest round of dividend increases, REIT yields are generous. The REIT SPDR ETF pays just 3.5%. But the average for my First Rate REITs is 5%. And the REIT Rater coverage universe as a whole is 6.3%, a high point for this decade so far. First Rate REITs so far have raised dividends 1.76% on average, with the coverage universe increasing 0.14% despite several big cuts.

REITs are still trading at a discount to privately held property. And as a sector, they’re still less than 2% of the S&P 500.

The largest by weighting—Welltower Inc (NYSE: WELL)—is still just 0.25% of the index. The second largest is Prologis Inc (NYSE: PLD) at 0.22%, followed by Equinix (NSDQ: EQIX) at 0.17%, American Tower (NYSE: AMT) at 0.14%, Simon Properties (NYSE: SPG) at 0.11% and nothing else over 0.1%.

Historically, when REITs have traded at such low weightings and high yields, they’ve rallied strongly the next several years. And there’s no reason to expect that won’t happen this time around.

Real estate is among the handful of “hard” assets that tends to perform well in times of elevated inflation. And the gains could be larger than usual the next few years.

That’s because new development in multiple sectors—especially residential and self-storage—has been curtailed for several years by a combination of higher for longer interest rates and previous overbuilding. And other sectors including data centers, senior living/housing and industrial/logistics are seeing historic booms due to generational demographic and economic changes.

Also bullish is the fact the REIT sector in general is learning to live with a higher cost of capital. And the lessons of the historic pandemic year collapse (2020) are still fresh in mind for management. That’s especially true in the retail sector, which took the biggest hit then.

Those are the positives. The chief negative is higher for longer interest rates that have slowed growth and are forcing even stronger REITs to hold in cash. And the longer Epic Fury fallout continues, the more likely rates will go higher and companies will retrench further.

Again, it’s worth pointing out that just a month ago, it looked like interest rates were little by little becoming a tailwind for the sector. But at this point, it’s hard to envision the Federal Reserve cutting interest rates with energy prices soaring and supply chain disruption still elevated from an uncertain Trump Administration tariff policy. And inflation could well go higher the next few months, pushing up borrowing costs even more.

But if recent weeks have shown us anything, it’s that geopolitical events can shift the picture in a hurry. And if the US economy starts to show signs of slowing this spring, the Fed may indeed change course to prevent something worse than an inflation spike.

Lower interest rates/borrowing costs are still the single most bullish potential development for REITs this year. So long as rates remain elevated, the sector isn’t likely to make much headway—other than the occasional takeover beneficiary and possibly the sectors that have been hot like industrial properties, seniors housing and data centers.

But when it becomes clear the worst is over, a safe, growing 5-6% plus yield paid reliably by a best-in-class REIT is going to be quite attractive. And from current prices, it’s easy to envision gains of 30%, 40% even 50% in a relatively short period of time.

Here’s What I’m Advising Now

The most important thing is to stick to the strategy. Remember, the goal here is to continue building positions in high quality, dividend-paying REITs when they trade at low prices.

As of Friday’s close, the S&P 500 was down about -10% from the all-time high set earlier this year. The Nasdaq is off by a like amount, which stands to reason as it’s dominated by the same Big 7 Tech stocks.

That magnitude of losses is usually called a “correction” rather than a real “bear market.” Unfortunately, the global fallout from Operation Epic Fury still appears to be spreading. So, we could see stocks slide a lot further, as more investors move to the safety of cash.

The history of big stock market declines is that they hit pretty much everything.

REITs are arguably historically cheap and under-owned. But the sector-wide selloff this month makes it clear that even stronger performers will take a big hit if the broad market continues to fall. In fact, private capital’s emerging vulnerabilities could worsen the situation for commercial real estate in the near-term—even as the demise of rival bidders for properties eventually boosts opportunity for REIT buyers.

Bottom line: High quality REITs are cheap after a multi-year under-performance, capped off by the past month’s declines. But they could still get a good bit cheaper. And the worse Epic Fury fallout becomes, the more likely some will fall and not get back up.

So my strong advice is to ignore the temptation for heroics, such as “backing up the truck” on bargains. Instead, continue to follow our four-part REIT investment strategy: