Solar Rises While SunPower Falls

Betting right on even the most powerful trends doesn’t guarantee investment success.

For America’s solar energy business, it’s both the best and worst of times.

Last week, leading US renewable energy producer NextEra Energy (NYSE: NEE) announced its second largest quarterly intake ever of orders for new generating capacity.

CEO John Ketchum forecast renewable energy generation will triple by 2030, fueled by both replacement of other power sources and “gross cycle demand.” Artificial intelligence-enabled data centers are one key catalyst. NextEra has 7 gigawatts of renewable energy capacity operating or in development serving the industry. And the company signed contracts with Google for another 860 megawatts his spring.

NextEra’s backlog of projects currently under development is 22.6 GW—with a largely transmission-enabled total pipeline of 300 GW. That makes it the only US renewable energy developer on the scale of China’s majors. And it’s by far the most profitable, routinely beating its target of 6 to 8 percent annual earnings growth.

Over the next few weeks, the rest of US utilities and renewable energy generators will report Q2 results. And though none have the scale of NextEra, solar will power earnings growth. In fact, Enel SpA (Italy: ENEL, OTC: ENLAY) and Iberdrola SA (Spain: IBE, OTC: IBDRY)—European utilities with substantial US renewable energy investments—both increased full-year 2024 earnings guidance last week.

Remarkably, utilities are accelerating solar deployment despite notable headwinds. Spooked by inflation, the Federal Reserve is holding borrowing costs at their highest levels in decades. And the Biden Administration has doubled down on Trump Administration tariffs, shutting off Americans’ access to increasingly cheap and efficient Chinese solar panels.

Utilities’ solar investment has proved resilient for three main reasons.

First, regulators are increasingly supportive, including in states governed by climate skeptics like Florida.

It boils down to cost. Utility-scale solar projects can be sited, permitted, financed, built and grid connected within 12 to 18 months. That’s a far shorter time frame than anything else including new natural gas, limiting risk of expense over-runs. And once built, maintenance costs are far lower and fuel expense is zero.

NextEra claims it’s cut $16 billion in fuel costs from customers’ bills since 2001. And the utility’s ongoing solar buildout has dispersed generation, hardening south Florida’s grid against the ever-present storm cycle. That’s pretty easy for any regulator or politician to support.

Second, despite challenging capital markets, utilities have found alternative sources of finance.

One is selling Inflation Reduction Act tax credits to third parties. Some Republicans have targeted that on the campaign trail. But even in the unlikely event of repeal, Blackrock’s recent investment in a $1.9 billion portfolio of NextEra projects suggests private capital sees value and will likely pick up any funding slack.

The third reason utilities’ solar investment is proving so resilient: US competition for customers, contractors, components and funding are evaporating right before our eyes.

Roughly one week after Joe Biden’s inauguration in January 2021, shares of then-US leading residential solar company SunPower (NSDQ: SPWR) hit a 12-year high of nearly $60 a share. That capped a one-year gain of over 850 percent, as investors bet heavily (and rightly) that the new administration would push renewable energy.

Since then, however, SunPower shares have dropped by almost -99%. And odds of a complete wipeout are growing, with the company largely suspending operations and its financials under investigation by the US Securities and Exchange Commission. Earlier this month, auditor Ernst & Young announced it was “unwilling to be associated with the financial statements prepared by management.”

SunPower’s hardly the only residential solar company in dire straits. On June 28, the sixth largest US resi solar company announced its “permanent closure,” joining 15 other failures since the beginning of 2023.

Some Wall Street analysts postulate this pain will be remaining players’ gain—notably SunRun (NSDQ: RUN), Sunnova Energy International (NSDQ: NOVA), Complete Solaria Inc (NSDQ: CSLR) and Tesla Inc (NSDQ: TSLA).

Tesla has made headway with sales of electric vehicle charging systems. The company reported a 99.7% lift in “Energy Generation and Storage” revenue, with a 256% boost in gross profit excluding selling and interest expense.

All four stocks, however, are well underwater this year, with Sunnova losing nearly half its value. And except for Tesla, none are anywhere close to being free cash flow positive. They’ll depend on outside capital to keep the doors open for the foreseeable future.

What went wrong with residential solar? Rapidly rising interest rates since early 2022 made it impossible for installers to offer cheap financing for consumers. Regulator-ordered changes in “net metering” rules reduced the appeal of selling power back to the grid. So will California’s decision to charge a fixed utility fee of $24.

But even before these setbacks, residential solar companies failed to demonstrate anything resembling a sustainable business model. In fact, explosive sales growth actually undermined margins in a perverse, reverse economics of scale.

Earlier this year, Nathaniel Conrad published a series of articles on residential solar’s demise in his “New Energy Future” column on Substack, based on personal experience in the sector. Front and center: A deeply flawed “installation based” rather than customer centric business model.

SunPower’s demise is the latest sign that model is dead. The question is will remaining companies adapt to survive?

My bet is some survivors will find a way, but not all. Tesla seems to have. SunRun may eventually by tying energy storage to solar, and linking its customers in “virtual power plants” integrated with the power grid in California. But the company is still nowhere close to being profitable, with -$3.3 billion in negative free cash flow expected this year.

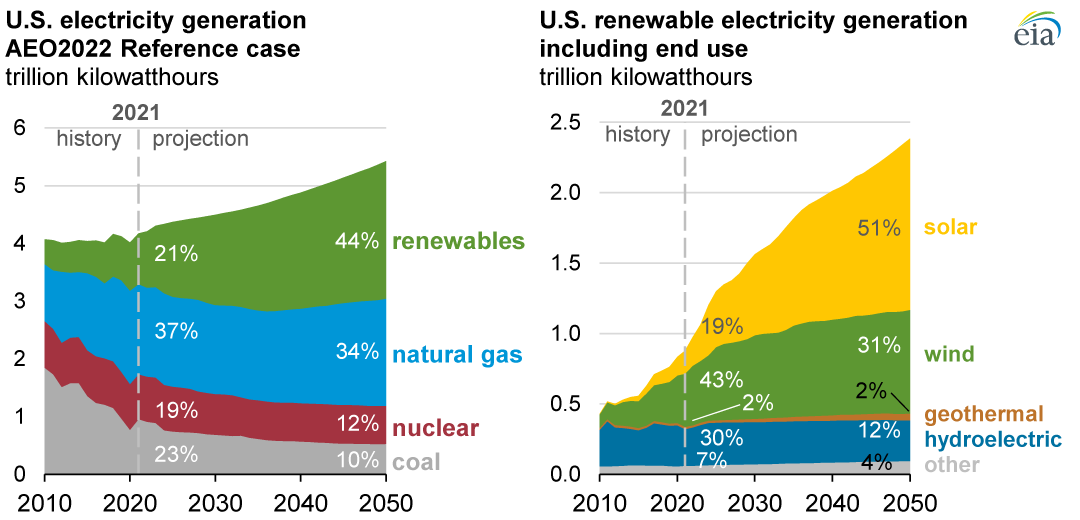

Solar energy’s share of US electricity generation has grown from just 0.1% to over 6% since 2010. That’s a phenomenal success story. And deployment is accelerating, with solar accounting for more than 75% capacity additions this year.

But the best bets on solar are still what’s surest: Regulated utilities and other major generation companies. Until the SunPowers figure it out, they literally have the field to themselves.