Spotting the Next Market Crash

The most likely catalysts for future catastrophe are almost always homegrown on Wall Street.

Thank you for reading Dividends with Roger Conrad! I hope everyone is having a great July 4th weekend with friends and family.

If you like what you’re seeing here, you might want to consider checking out the paid version of this service, Dividends Premium. This coming week, I’ll once again highlight my actively managed income and growth portfolio, which continues to stay ahead of the market and features a low risk 5% plus yield.

Later in the month, I’ll be posting Dividends Premium REITs, with advice and analysis for more than 80 real estate investment trusts. And throughout the month, you can talk to me at my Dividends Roundtable investment discussion forum, which I host 24-7 on Discord.

To find out more, follow the link attached to this email, or on the Substack application. Here’s to a rewarding second half 2025!—RC

The past few Wednesdays this summer, I’ve taught a class on investing and investment markets to a pair of college students—one of them my younger son.

We’ve explored what makes investment markets tick. I’ve shown them the basics for reading primary financial documents like income statements and balance sheets for companies in a range of industries. And we’ve examined the pros and cons of multiple investment strategies.

Throughout, I’ve tried to make it about the practical—what I’ve actually experienced in my 40 years investing and advising others. And as should be the case with inquisitive young people, the conversation has frequently come around to the less savory side of the money business: Greed, fear, fraud, outright deception and everything else on the dark side.

One thing they’ve discovered is there’s certainly plenty to talk about from 40 years of experience. So last week as an assignment, I told them to check out the 2015 film “The Big Short.”

For those of you who haven’t seen it, the movie is the story of a handful of big money investors who bet on the collapse of the market for mortgage backed securities in 2007-09. And though enduring wrenching indignities for daring to bet against the crowd, they became fabulously wealthy in the end.

The Big Short features some pretty good acting. But with all due respect to Brad Pitt, Christian Bale and Steve Carell and the other A-listers, the real reason to watch or revisit this film is for the lessons about investment markets it teaches.

For the record, I couldn’t disagree more with the takeaway many people have—that investment markets are too hopelessly corrupt and weighted towards the big boys for anyone else to bother with. That’s an argument used by trillion dollar investment firms like Blackrock and Vanguard to herd small investors into “passive” investment products—more on that in a minute.

The biggest lesson of the film is investors who use their own judgment and educate themselves will not just weather the worst disasters in investment markets. But they can actually turn the downside to their advantage to build real wealth.

This is contrary investing 101—by the way if you can still get a copy of Richard E. Band’s “Contrary Investing,” it’s still essential reading despite being written in the 1980s.

The name of the game in investing is to buy low and sell high. And you won’t do that with any consistency by not being willing to make bets that go against prevailing popular opinion in the market place.

The real people who the characters of The Big Short were based on knew this in their bones. So did the people who bet against Enron and Worldcom when the Wall Street consensus was their stocks would rise forever, or at least the foreseeable future. So did the people who bet against Big Tech in 2000 for the same reason.

So what happened to make them right? Simply realizing a simple truth: Multi-trillion dollar investment companies talk a good game about serving investors. But what keeps the lights on in those posh offices and pays those bonuses is selling product. Sure, these firms employ many creative, intelligent and highly energetic people. But no one gets paid unless investors are buying products.

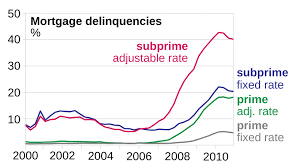

The hot product in the mid-00s was mortgage-backed securities (MBS). In previous decades when Americans bought houses, they usually wrote a check for principal and interest to the same bank that underwrote their mortgage until it was paid off.

But by the mid-1990s, financial deregulation has loosened the rules for banks. So it became increasingly common for banks to sell those same mortgages to big investment firms, who packaged a bunch of them into a single security—called an MBS or mortgage-backed security.

Early MBS issuers stuck to mortgages perceived to be low risk, based on credit of borrowers. And they became incredibly popular as interest rates remained well behaved and investors increasingly craved safe, high yields.

The problems began when—as MBS sales soared—demand began to dwarf supply. And MBS issuers began to tap into riskier and riskier mortgages, of which there was growing supply because deregulation stripped away many of the Great Depression era rules for mortgage lending.

Even that was OK at first as the economy remained generally strong. But when growth began to soften and interest rates rose, mortgage delinquencies started to soar. The mortgages inside the MBS stopped paying. And the whole house of cards came crashing down, nearly taking the banking system with it.

The fact the credit rating agencies like S&P, Moody’s and Fitch were rating rotting MBS as super safe into the great crash is particularly disturbing. And it should be a wake up call for anyone tempted to just take someone else’s word for it when it comes to investing, rather than thinking for themselves.

And there’s another lesson here I think is even more important. That is the financial system—with the investment giants at the center—basically kept selling as much product as they possibly could, even after they realized what they were unloading was basically worthless.

Unfortunately, despite how bad 2007-09 was, big investment firms still operate with the same basic motivation: That’s to sell, sell, sell until you can’t anymore—if you want to even keep your job in the era where firms can and will replace human beings with artificial intelligence and algorithms wherever they can.

A bit of dark humor that’s been around as long as I’ve been in this business—and no doubt well before—is that America’s biggest financial companies go through a crisis of their own making about once a decade. And in my experience, that’s been pretty much spot on, with the industry serving up such catastrophes of its own making as the S&L wipeout, the Latin America debt crisis of the 1990s and so on.

The experience of 2007-09 may still be restraining behavior in the banking system. But there are still some pretty good candidates to base a future movie on, mainly products the Blackrocks and Vanguards are pushing most aggressively now.

Right now, that’s passive investing products—marketed as a way to grow your portfolio at low risk and no real effort.

I was always taught you get out of something what you put into it. Passive investing says that for the first time in the history of the world, you can get superior results with no effort—other than cutting a check to the investment industry’s largest companies.

I don’t confess to know the inner workings of all the passive products the Street is peddling now on steroids. But I can see one huge vulnerability: The extreme dependence on weighted S&P 500 ETFs—which right now are 35% invested in just 8 stocks trading at valuations pretty much unmoored from actual business value, and none of which pay a decent dividend.

That’s a lot of eggs in one basket—which again has never been a good idea in the history of the world. And if these passive funds are where your wealth is tied up, time may be running out to get control of your financial health.