US Renewable Energy Comes of Age

Achieving critical scale is every energy resource’s secret to success.

Welcome to Dividends with Roger Conrad, and Happy Star Wars Day for we many fans of that franchise.

See the link in this email and the Substack app for more on the paid version of my advisory Dividends Premium—including my diversified income portfolio, Dividends Premium REITs and 24-7 access to the Dividends Roundtable I host on the Discord app. Thanks for reading!—RC

What caused Spain’s April 28 electricity outage? Power grids are complex animals. So an actionable explanation will take time.

There was, however, one undeniable and massive development in the energy sector last week. Four US renewable power leaders demonstrated they have the scale for sustainable success.

In my Substack a week ago—“Your Antidote to Trading Trump Tweets”—I highlighted Q1 earnings and guidance at NextEra Energy (NYSE: NEE). Those results were proof positive that investment-led growth is on track at the Florida-based utility and leading US wind and solar power generator, despite numerous headwinds.

Since then, three more leading US renewable energy companies have affirmed their expansion plans are on track—despite facing the same challenges of higher for longer interest rates, an unprecedented US-versus-the world trade war, a softening economy and increasingly unpredictable federal government tax policies and regulation.

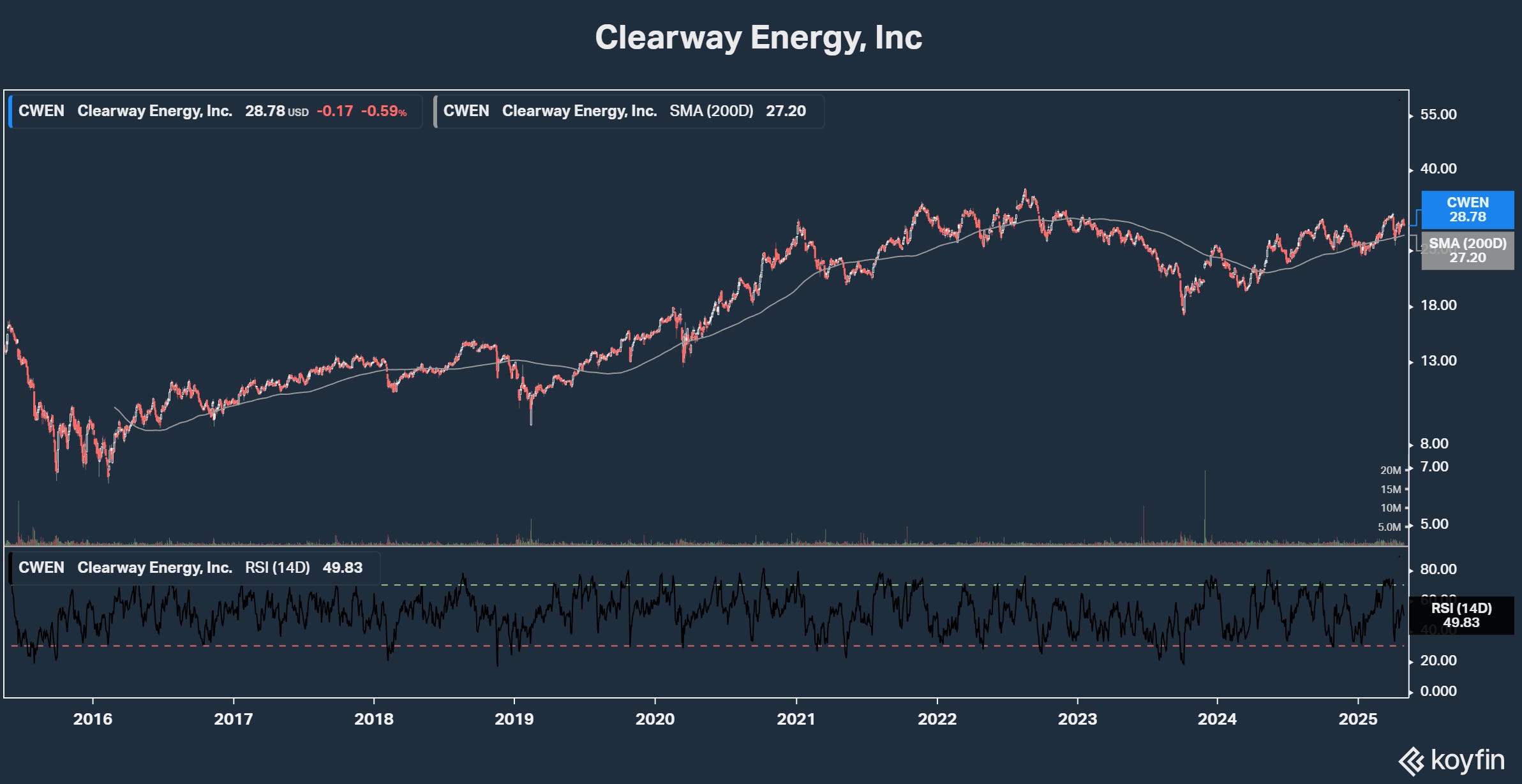

Backed by super oil major TotalEnergies (Paris: TTE, NYSE: TTE) and private capital firm Blackrock, Clearway Energy (NYSE: CWEN) recorded record output and cash flow while advancing a 9 gigawatt pipeline of projects. Those included repowering the Mt Storm wind facility in Appalachia selling energy to Microsoft (NSDQ: MSFT).

AES Corp (NYSE: AES) is on track to bring 3 GW of new renewable energy into service this year, including an already completed 250 megawatts also serving Microsoft. Total backlog is 11.7 GW, with 7 GW slated in the US through 2027. The company has total agreements for 9.5 GW of power sales to data centers, “more than anyone else in the sector” according to management.

Brookfield Renewable (TSX: BEP-U/BEPC, NYSE: BEP/BEPC) continues to execute a 10.5 GW “initial” supply agreement with Microsoft. The company expects to bring 8 GW into service this year, more than twice its “run rate of commissioning capacity just 3 years ago.”

The trio’s growth numbers are right in line with the 3 GW of new contracts NextEra Energy reported signed in Q1. And they clearly back the assertion of that company’s CEO John Ketchum that corporate America’s demand for wind, solar and paired energy storage is robust as ever.

All four companies have faced immense skepticism over the past year. But their numbers show demand growth from artificial intelligence-enabled data centers is not up for debate. It’s happening in real time, and US electricity companies are meeting it mainly with renewable energy.

What’s really impressive in these companies’ results is they’re executing on growth even as others are leaving the business to them.

National Grid (London: NG, NYSE: NGG), for example, was making money with its 3.9 GW operating renewable energy portfolio and 30 GW US development pipeline. But management realized it’s better off selling these operations to much larger Brookfield. So did Duke Energy (NYSE: DUK) two years earlier, when it also sold wind and solar assets to Brookfield.

In the energy business, scale is critical, regardless of resource. US nuclear power plants today, for example, run between 90-100% of their operating capacity. But they ran at just 60-65% in the 1990s, before a great consolidation of ownership.

Now the owner of nearly two dozen reactors, Constellation Energy (NYSE: CEG) can apply lessons learned from one reactor’s refueling outage throughout its entire fleet. The result is fewer unscheduled outages and shorter times having plants offline, adding up far greater profitability.

At the previous oil and gas cycle peak in 2024-15, there were hundreds of US shale producers, and dozens of midstream and pipeline operators serving them. All but a handful lacked critical scale to weather a real downturn. And they perished when boom inevitably turned to bust.

But the leaders gained critical scale. And as a result, the US shale oil and gas industry is the best prepared it’s ever been to handle a recession and much lower oil and gas prices.

US renewable energy leaders have achieved roughly the same milestone in their rapidly maturing space.

Except for perhaps NextEra, they’ve got a long way to grow before they come close to the financial power of super major oil companies like TotalEnergies and Chevron (NYSE: CVX)—which literally have stronger balance sheets than most sovereign nations.

But unlike the “green power” industry that sprang up in the previous decade to breathless hype, these four companies have demonstrated staying power.

That starts with being able to consistently raise low cost capital. AES and Clearway are actually self-funding development plans. Brookfield accesses private capital markets through parent Brookfield Asset Management (TSX: BAM, NYSE: BAM) and various third parties. And NextEra Energy is anchored by perhaps the strongest regulated utility in America, Florida Power & Light.

During last week’s earnings calls, all four companies addressed the possibility Congress will scale back wind and solar tax credits and/or eliminate “transferability”—which enables developers to sell tax credits to third parties.

My view is tax credits have enough support among Republicans to make repeal problematic. But all four companies have “safe harbored” credits for the projects currently in development: Once 5% of the cost of materials has been incurred, projects have four years to enter service to be entitled to receive tax credits.

The 25% tariff on imported steel—and accompanying price increases by US producers—have already increased the cost of infrastructure projects. That may have a chilling effect on re-shoring of manufacturing, which has been a driver of electricity demand growth in many regions.

But these four companies’ direct exposure to tariffs is very low. They’ve been adjusting supply chains for several years in anticipation of higher import costs, as well as to prevent the kind of disruption we saw in pandemic year 2020. And as they’ve grown larger, they’ve gained pricing power with vendors, enabling them to lock in prices with contracts.

NextEra estimates just 0.2% of its CAPEX through 2028 is exposed to tariffs. Globally operating AES and Brookfield have largely matched input sources to where projects are located. Clearway still buys batteries from China. But all four companies report the ability to push cost increases onto ultimate customers. Also, their projects are on private land, skirting erratic US permitting policy.

Bottom line: Corporate America still favors the renewable energy these four companies sell.

And small wonder: New wind, solar and battery storage production capacity can be built in one-fifth the time of new natural gas and one-tenth or less what’s needed for new nuclear. And tariffs on steel alone have further widened the already substantial cost gap between cheap renewables and new natural gas and nuclear projects.