Week One: Trends to Bet On

Portents from the stock market's first 6 trading days in 2026.

Editor’s note: Greetings from Hong Kong! Here are my thoughts on big picture trends that emerged from the investment markets first full week in 2026.—RC

It’s dangerous to draw too many conclusions from just one week of stock market trading in January. The S&P 500 has come out of the gate at full speed, only to falter by spring. And conversely, first week selloffs have led to surges by the end of the month.

But I see a handful of trends that at this point look set to gain strength in 2026. And if they do hold, they’ll be difference makers for investment returns this year.

Let’s start with interest rates. It’s no secret the Trump Administration is anxious to bring Americans’ borrowing costs lower in advance of November elections.

A newly appointed Federal Reserve chairman this year will be under immense pressure from day one to cut the Fed Funds rate sharply. And last week, the president opened a new front, declaring on social media that he would “order” Fannie Mae and Freddie Mac to use their entire cash reserve of $200 billion to buy mortgage bonds—for the purpose of bidding up prices and thereby lowering mortgage rates.

Actual borrowing costs, however, remain higher for longer. The 10-year Treasury bond yield is stuck well above 4%, basically where it was in mid-2023. Lofty mortgage rates have kept homes unaffordable in much of the US. And corporations are still refinancing maturing debt by issuing bonds at meaningfully higher rates.

The reason is inflation expectations. But pushing Fed Fund lower, the Fed has decreased banks’ cost of capital, both at its discount window and by pushing down savings and money market rates. But lenders are concerned the voting members of the Federal Open Market Committee will bow to political pressure and stop fighting inflation. And they continue to require a premium for longer term debt.

As a result, corporations are increasingly locking in their cost of debt where they can, paying down credit lines even with longer-term rates still higher for longer.

Earlier this month, for example, T-Mobile US (NSDQ: TMUS) issued $1.15 billion of 5% notes due in 2036 and $850 million of 5.85% due 2056. The purpose: Pay off shorter-term debt with variable interest rates.

Clearway Energy (NYSE: CWEN) was able to upsize it offering of 5.75% notes due 2034 from $500 to $600 million. Those proceeds too will go primarily to pay down credit lines with variable interest rates. And deep junk-rated, small communications until Uniti Group (NSDQ: UNIT) is locking in debt costs by issuing new bonds securitized by its fiber assets.

That only scratches the surface of companies that will issue debt in 2026. But it continues the trend of 2025, with corporate America seemingly becoming resigned to the fact that borrowing costs are going to stay higher for longer—and possibly go up even more if inflation expectations rise further.

That means more companies are likely to allocate cash flow to keep debt lower, either by internally funding more capital spending or paying it off outright. That means reduced dividend increases, and cuts for some.

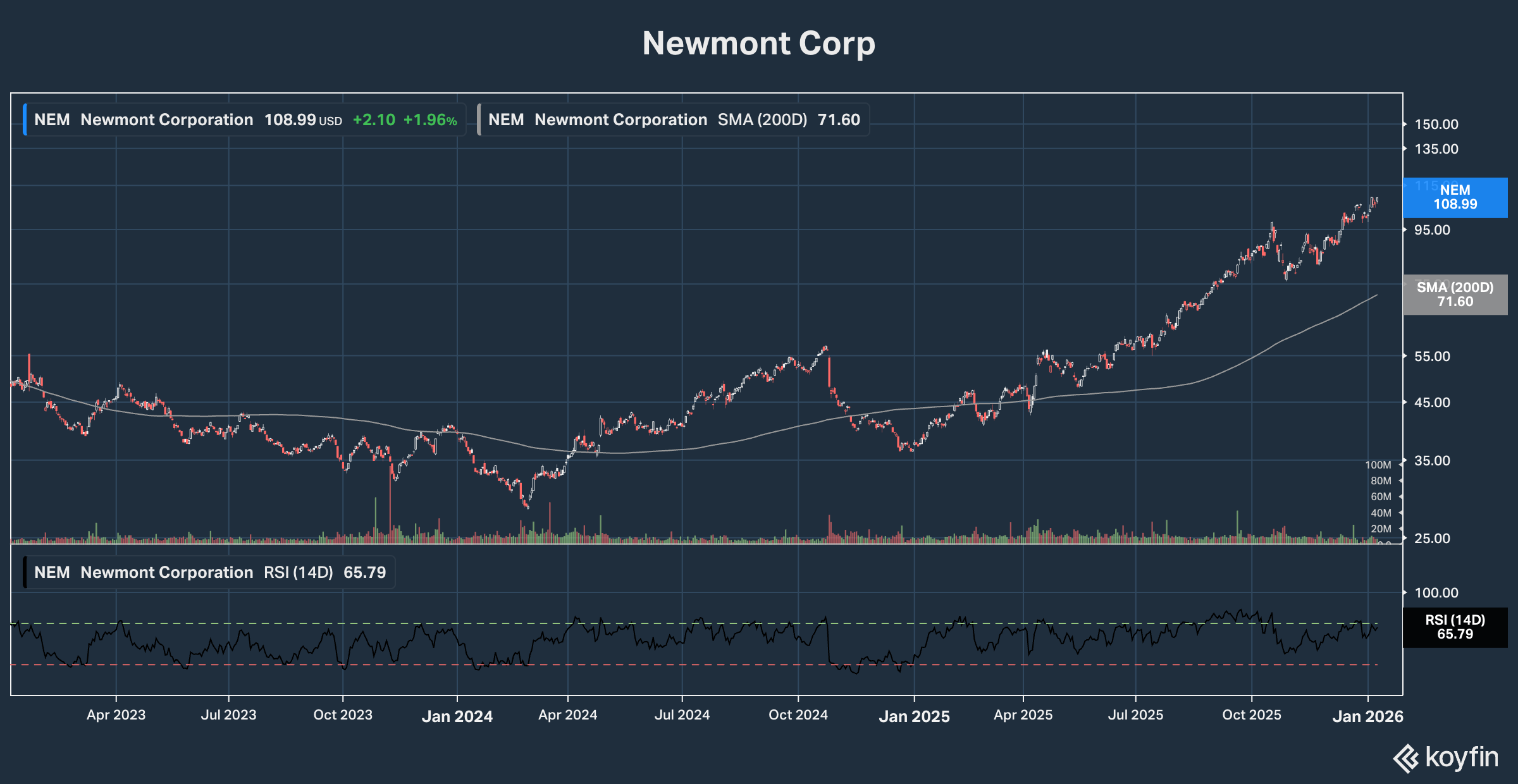

The flipside of increased expectations for inflation is stronger performance of commodities and materials stocks. NYSE-listed shares of BHP Group (ASX: BHP, NYSE: BHP) have gained strength since second half 2025. Gold miner Newmont Corp (NYSE: NEM) was a huge winner last year and it’s up another 10% so far in 2026.

MDU Resources’ (NYSE: MDU) construction materials spinoff company Knife River (NYSE: KNF) was red hot in 2024 before cooling off last year. But in a little over a week’s trading this year, the stock is up almost 14%.

Will metals and materials stocks stay strong this year? The answer depends on if the global economy stays strong, particularly China—which is by far the most important market. And that currently looks like a great bet.

Our Dividends Premium play on Hong Kong is already up big in the year’s opening days. And while US investors can’t own numerous Chinese companies directly, iShares China ETF is also well in the black this year, after a big gain in 2025.

China and Hong Kong are arguably the only stock markets in the world that could be resilient in the face of a meaningful US correction. That in my opinion is a real possibility this year, with roughly 38% of the S&P 500 ETFs that increasingly dominate investor portfolios in just 7 Big Tech stocks—all historically high priced and leveraged to a single investment theme: AI.

So far in 2026, however, investors are still willing to keep buying Big Tech. The SPDR S&P 500 ETF, for example, is up around 2%. The SPDR Tech Index is up a like amount. That’s despite Apple Inc (NSDQ: AAPL) being down a little less than -5% year to date.

Dividends and value stocks are thus far doing slightly better than the S&P 500. But so far with very few exceptions, the better performers are the companies that led the way last year. Many underperforming real estate investment trusts, for example, have so far added to their losses. Momentum is still a primary driver of returns, if not the most powerful one.

It’s easy to envision much of what the second Trump Administration has done so far being reversed after the next election. But for this year at least, its actions will be a major wildcard for investor returns, with results that will surprise many.

One of those is the fierce production discipline of the US shale oil and gas industry, focusing on reducing costs and debt at a time of soft commodity prices.

Shale discipline prevented a crash in energy company earnings last year. And producers will continue to control output until oil and gas prices move to a higher level. That’s no matter what happens in Venezuela, Iran, Russia or anywhere else.