What the Fed’s Pivot Means

And why I’m betting on a Great Rotation but with one big caveat.

“The time has come for policy to adjust.” That’s the money quote from the US Federal Reserve’s meeting in Jackson Hole, Wyoming last week, courtesy of Jerome Powell.

The clear implication is the Fed’s Chairman at least believes the past two-and-a-half years of “higher for longer” interest rates have made sufficient progress reining in inflation. Now it’s time for the central bank to combat emerging weakness in employment and overall growth.

To be sure, the Fed’s long-stated measure of inflation is still meaningfully higher than its long-standing target of 2 percent. But it’s hard to imagine that the other voting members of the Federal Open Market Committee would block at least a quarter point cut in the Fed Funds rate.

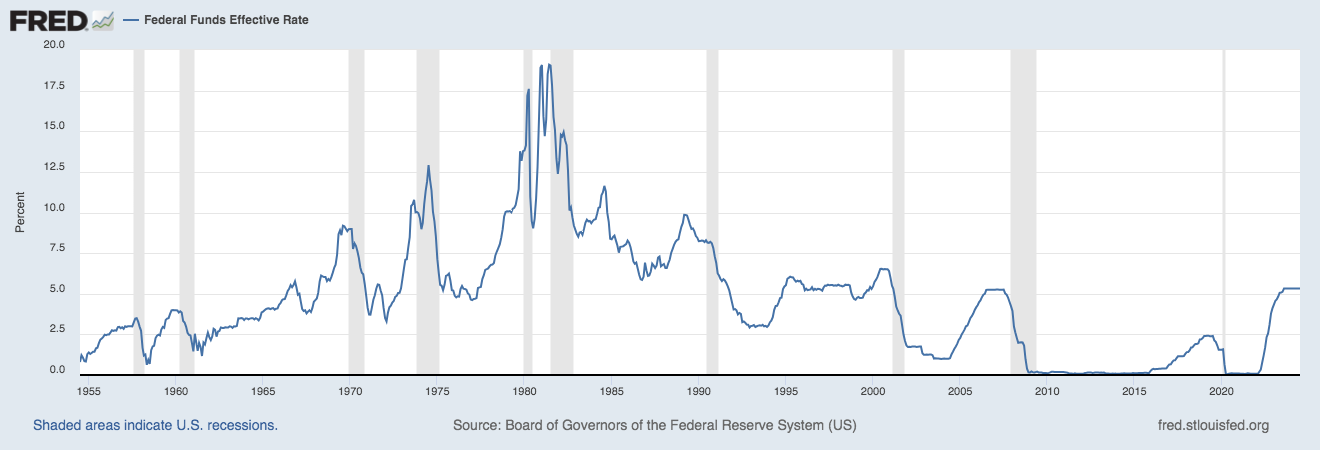

For one thing, the rate has been frozen at 5.25 to 5.5 percent for some time. And it’s been many months since a significant number of Fed governors have publicly indicated a desire to raise rates. In fact, several have repeatedly expressed a preference to cut at the “proper” time.

With the notable exception of Japan, a pivot to lower interest rates would align US monetary policy with the rest of the world. Central banks from China to the EU have shifted to a loosening mode. The UK central bank announced a quarter point cut in its official lending rate to 5 percent earlier this month, the first cut this decade.

Most importantly, this US Fed states as a point of pride that it’s “data driven.” And earlier this month, the data point it’s reacted to most historically—the health of investment markets—spoke loudly and clearly that it’s time for a pivot to lower interest rates.

The debate now has shifted to how deeply the Fed will cut rates at its September meeting. And there’s considerable difference of opinion on how aggressive they’ll be, with some still forecasting as much as 150 basis points of cuts by the end of the year or early 2025 at the latest.

My advice for investors: Don’t waste your time trying to figure out what Powell and Co will decide. And if you do hazard a guess, don’t shake up your portfolio based on that.

My best guess is Fed actions will continue to be shaped by what happens in the stock market. Mainly, if all we see is continuing gains in the S&P 500, the central bank will feel a lot less urgency to make big cuts sooner. But if there’s a selling wave, it will move swiftly. And if a real crash in stocks becomes a systemic economic event, Fed Funds near zero wouldn’t be out of the question.

If that sounds like crazy talk—and I admit it does even to me just now—then I suggest taking a look at the history of the Fed Funds rate in my graph below.

It’s a universal tendency of investors to assume current trends will stay in motion forever. That’s why so many of us always have real trouble selling high and buying low.

But investment markets always shift eventually. New trends are born and old ones die. And historically, the longer and further a trend has run, the bigger the reaction the other way.

By any measure the “Buy Big Tech” trend has run for a very long time. The S&P 500 and related ETFs are currently over 42% weighted to just four sectors, all Big Tech: Semiconductors (11.57%), Internet (11.56%), Software (10.38%) and Computers (8.51%).

The S&P 500’s six largest holdings are the Biggest of Big Tech: Apple Inc (6.9%), NVIDIA (6.72%), Microsoft (6.54%), Alphabet (3.8%), Amazon (3.4%) and Meta (2.5%). That’s almost 30 percent in just six stocks.

By contrast, the heaviest energy stock weighting is ExxonMobil (NYSE: XOM), in 14th place at just 1.1 percent of the index. Chevron Corp (NYSE: CVX) is second largest at just 0.53 percent in 28th place.

Consider that despite slumping oil and natural gas prices, ExxonMobil had roughly the same amount of sales as Apple over the last 12 months, and almost four times NVIDIA’s. Yet its S&P 500 weighting is less than one-sixth that of either company.

Big Tech is undeniably the key driver of US economic growth. But its relative overweighting is historic. And that means the S&P 500 right now has a record number of eggs in a single basket.

Combine that with the fact that for the first time in history, more money is now passively invested in the stock market with S&P 500 ETFs and the like than is actively managed. That means a crash in just 6 stocks could literally trigger a major wealth effect and accompanying economic event.

Small wonder then the Federal Reserve is focused on the stock market. In fact, I would argue all Americans should be grateful for that, regardless of how invested we are.

So how is the coming Fed pivot meaningful for investors? First, it increases the odds that the stock market’s next move will be a great rotation rather than a great correction, though just how much risk is reduced will depend on how aggressively the central bank moves.

Second, it means borrowing costs have almost certainly peaked this cycle. To the extent the economy slows in second half 2024, spreads between rates offered to AAA and junk rated borrowers will widen.

But for capital-intensive companies like investment grade rated utilities, the decline in long-term bond rates we’ve seen since April will continue. And probably sooner rather than later, shorter-term rates will drop as well.

Third, the days of cash alternatives like money market yields being north of 5 percent are almost certainly numbered. Coupled with lower bond yields, that means stocks of companies paying safe and reliably growing dividends will become increasingly attractive over the next several years.

Bottom Line: Powell’s pledge is another signal for investors to place long-term bets on a great rotation from today’s Big Tech to value and dividend stocks, with one caveat—Stick to high quality companies that can hold to plans for investment and paying dividends, even if the Fed moves too slowly and there’s a great correction in our future first.