When the Bombs Fall, Keep Your Balance

Energy stocks are making money hand over fist. That's exactly when balance matters most.

Editor’s note: Operation Epic Fury fallout roiled global investment markets again last week. And with the fog of war descended, all that’s certain about the eventual outcome is a great deal of vital energy infrastructure is at least temporarily out of commission.

Stocks of energy companies operating outside the Middle East have been big winners. But share prices have now come a long way in a hurry. And if Epic Fury brings on a global recession, they’ll also be vulnerable.

For times like these, portfolio balance is vital. And keeping yours as the bombs continue to fall is what this week’s post is all about. Dividends Premium members are cordially invited to join my Dividends Roundtable chat, which I host 24-7 on Substack. Happy Spring everyone!—RC

Super major oil companies like Chevron Corp (NYSE: CVX), ExxonMobil (NYSE: XOM) and TotalEnergies SE (Paris: TTE, NYSE: TTE) boast stronger balance sheets than most sovereign nations. And as fallout from Operation Epic Fury has shown us once again, the industry they dominate is critical as ever to a healthy global economy.

Super majors are also among the surest long-term money-makers in the stock market. The first stock I ever purchased for my own account was Texaco. I held through the Chevron merger, automatically reinvesting dividends every quarter. Today, my position is worth almost 45X the initial investment. And my annual dividends have “lapped” what I put in originally more than twice over.

But once you start harvesting instead of just saving, even super major oil companies are worth pruning back occasionally. The reason is balance.

A balanced portfolio is never at risk of being sunk by an unexpected disaster at a single stock. And paring back a position that’s become large enough to be dangerous also frees up cash to invest in cheaper, higher yielding alternatives.

What Could Take Energy Down

To be sure, I’ve rarely been this happy to own energy stocks. They continue to be that rare island of green in a sea of red.

S&P 500’s Operation Epic Fury slide is still a long way from bear market territory—defined as a decline of 20% or more from the late January high of 7,000 and change.

And so far, the roughly -7% retreat has been relatively orderly. Several leading Big Tech stocks are now well under water for the year. That includes artificial intelligence leader NVIDIA Corp (NSDQ: NVDA), which is still almost 8% of the S&P 500 index by weight. Microsoft Corp (NSDQ: MSFT) at 5% of the index is down more than -20%.

But energy is still making money hand over fist, preserving portfolio value while almost everything else is dropping. And these stocks will move a lot higher in coming years, as the long-term energy super cycle continues to unfold.

But that said, it’s fair to ask what happens to this narrow group of winners if Operation Epic Fury fallout triggers something worse. And market history isn’t particularly encouraging.

When the overall stock market goes, pretty much everything sells off with it—even sectors that hold up in the early stages of the meltdown. And there are now a multitude of potential catalysts that could turn this so-far orderly stock market retreat into a full-scale rout.

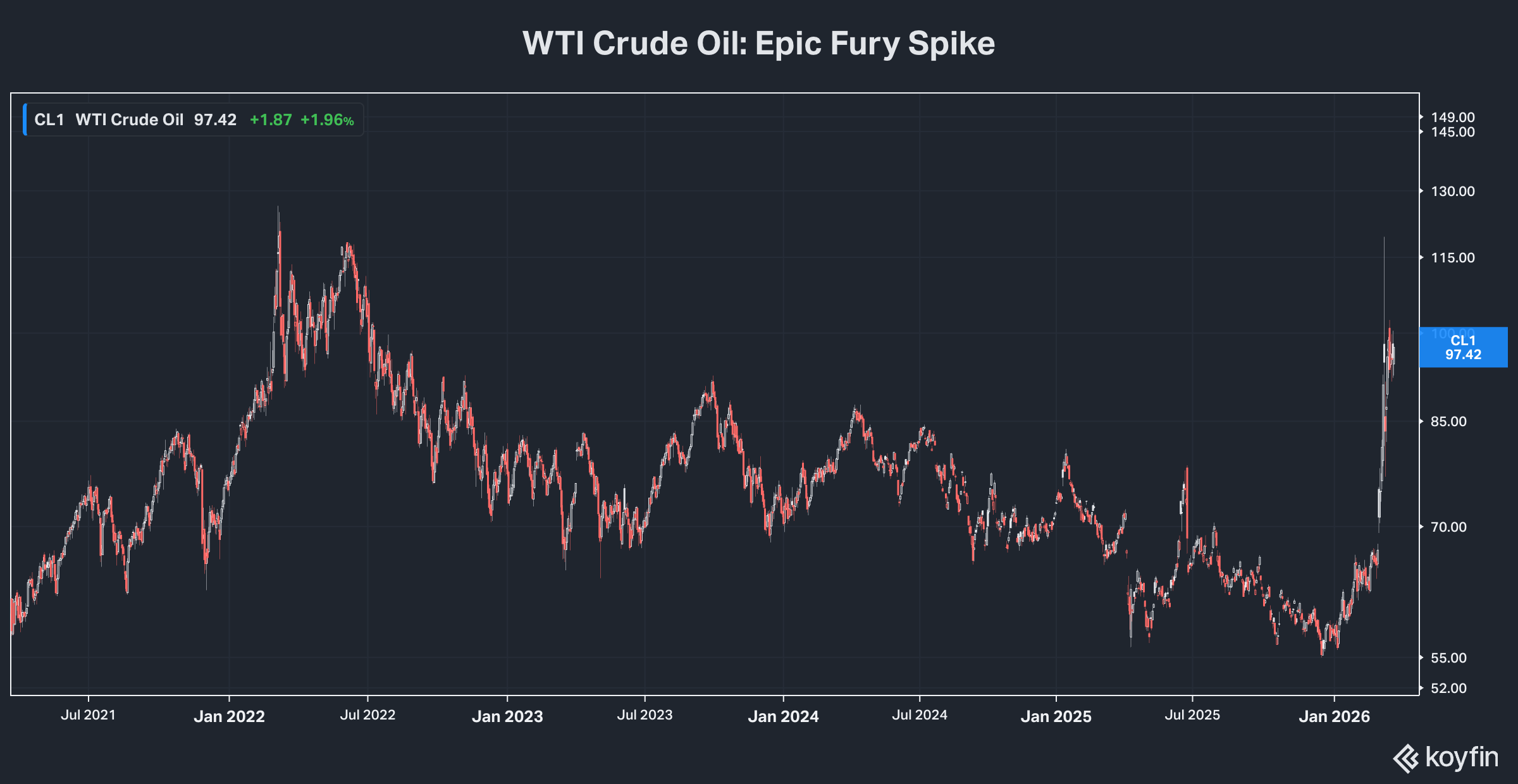

Opening the Strait of Hormuz this week would likely trigger at least some relief by reducing upward pressure on oil and gas prices. But last week, QatarEnergy reported 17% of its LNG export capacity has already been destroyed by Epic Fury fallout. And with energy infrastructure squarely on the target list of both sides, disruption in the global energy trade will likely continue for months, even in a best case.

Qatar’s force majeure on its LNG sales contracts has set off a scramble in Asia and Europe to secure sufficient supplies elsewhere. That will come at the price of higher inflation and slower growth. And we’re seeing the fallout already in global stock markets, with South Korea down -15% from all-time highs reached in late February.

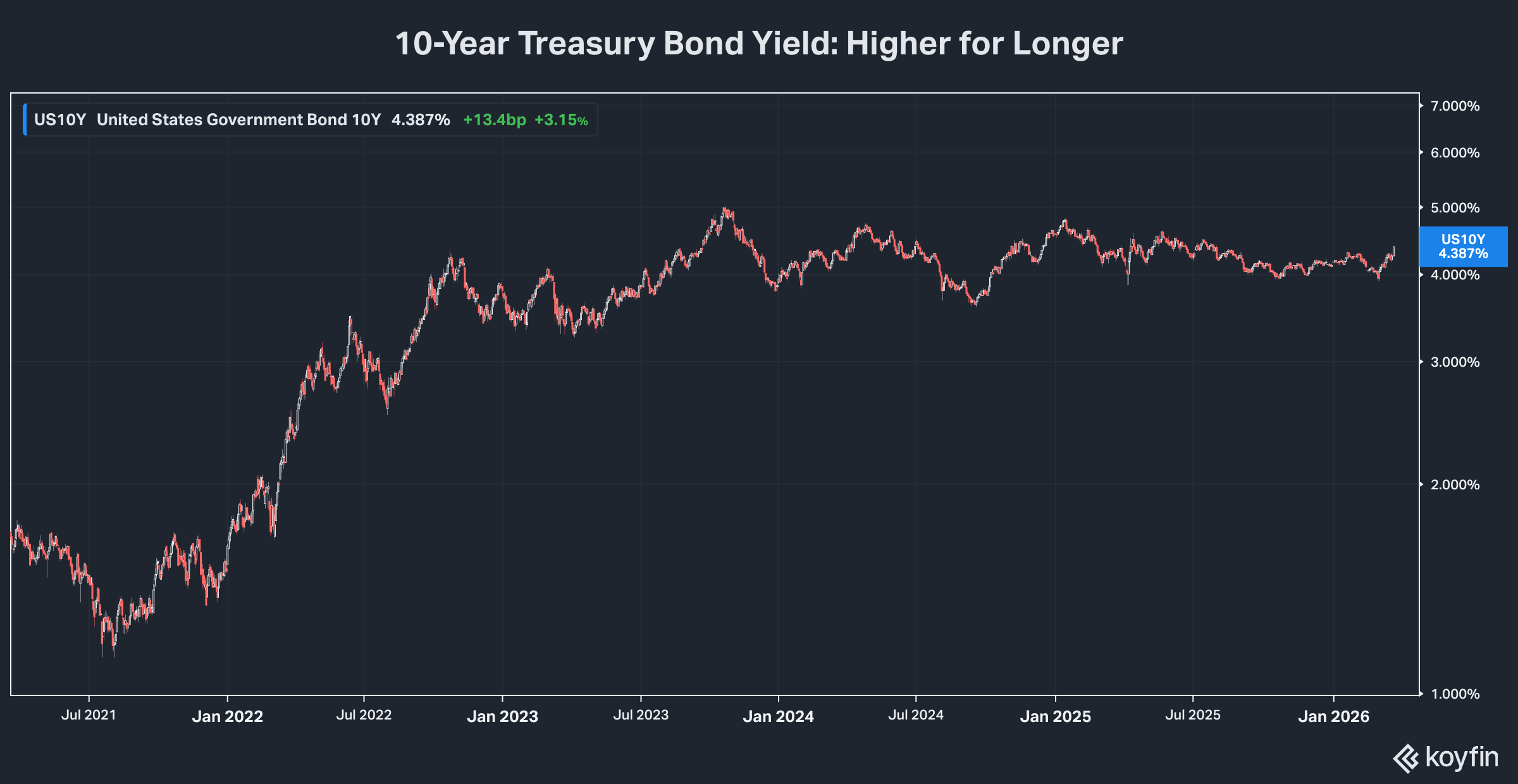

US producer prices in February rose 0.7% even before Epic Fury fallout. Resulting inflation worries prevented the Federal Reserve from cutting the Fed Funds rate again, despite White House pressure to do so. And bond yields are rising rapidly again, with the 10-year Treasury yield nearing 4.4% at last week’s close.

Higher for longer interest rates were already pressuring investment before Epic Fury. The exception has been artificial intelligence and data center-related plans, including for generating needed electricity. And while utilities’ most recently announced CAPEX plans showed no evidence of a slowdown, even these companies’ ability to absorb higher borrowing costs without making adjustments is not infinite.

Restrained investment means slower economic growth and less employment. At least one major Wall Street research firm is now forecasting odds of a US recession this year as above 50%. And the stock market will react long before actual GDP goes into reverse for two consecutive quarters.

There are also good reasons why the Epic Fury selloff could reverse suddenly and with a vengeance, including an outbreak of peace for whatever reason. And it’s important to remember we’re just a few weeks removed from the strong Q4 results and 2026 guidance updates our companies reported.

The near-term challenges from soaring energy prices, rising interest rates and a weakening economy are very real. But these companies’ strong balance sheets and pricing power are solid insurance they’ll persevere. And their long-term prospects are still bright. We’re going to want to own them on the other side of this.

What To Do Now

So what to do with our big winners in the energy sector?

First and foremost, we need to be deliberate. That means managing positions by moving incrementally, rather than precipitously.

Last week, I advised making the following four trades in the Dividends Premium model portfolio. They were to: